Cytora, CoverGo, Zywave, Travelers/OpenAI and SUPERAGENT compared on the before/after numbers from real carrier rollouts.

The short answer: which AI underwriting agents carriers actually deploy

In 2026 the AI underwriting agents carriers actually deploy fall into two camps: carrier-side risk-processing platforms led by Cytora and CoverGo that automate intake, triage and document parsing inside the underwriting workflow, and distribution-side agents from Zywave and SUPERAGENT that automate prospecting and quoting for brokers. Travelers sits in its own lane with an OpenAI-built claims voice agent. If you are a commercial carrier looking for proven before/after numbers, Cytora is the safest bet today; if you are a retail agency drowning in quoting, SUPERAGENT and Zywave are aimed squarely at you. This guide compares the AI underwriting agents 2026 carriers are actually evaluating, camp by camp.

The distinction matters because almost every vendor now calls its product an ‘AI agent,’ but they are solving very different problems on opposite ends of the same value chain. A carrier cares about throughput per underwriter and straight-through processing. A broker cares about how many quotes a producer can generate before lunch. The platforms below are not interchangeable, and buying the wrong camp is the most common mistake we see.

This comparison anchors every claim to a real, named rollout with a verifiable number. Where a vendor only offers a projection or a glossy case study without a baseline, we flag it. The market is moving fast enough that hype outruns evidence, so the evidence is what we lead with.

Why AI underwriting agents 2026 became unavoidable

$154.39B

AI-in-insurance market by 2034

Up from $13.45B in 2026 at 35.7% CAGR (Fortune Business Insights)

78%

Q4 2025 insurtech funding to AI firms

Per Gallagher Re Global InsurTech Report

75%

Faster claims resolution with AI

Alongside 30-40% cost reductions (Vantage Point)

58%

GenAI use cases in core workflows

Claims, underwriting, pricing, quoting in Q4 2025

AI underwriting agents 2026 went from optional to unavoidable because the money, the use cases and the performance data all converged in a single 12-month window. The AI-in-insurance market is projected to grow from $13.45 billion in 2026 to $154.39 billion by 2034, a 35.7% compound annual growth rate, according to Fortune Business Insights. That is not a niche; that is a core infrastructure shift.

The funding signal is even sharper. Gallagher Re reported that AI-centred insurtechs captured roughly 78% of all insurtech funding in Q4 2025, and claims, underwriting, pricing and quoting together accounted for 58% of disclosed generative-AI insurance use cases that quarter. Capital and engineering attention are pointing at exactly the workflows these agent platforms automate.

And the performance gap is the kind that forces a board to act. Across the industry, AI-driven claims automation is resolving claims around 75% faster with 30-40% cost reductions, while underwriting straight-through processing rates have jumped from 10-15% to 70-90% and cycle times have collapsed from roughly three days to three minutes on automatable submissions. When a competitor quotes in minutes and you quote in days, the choice makes itself.

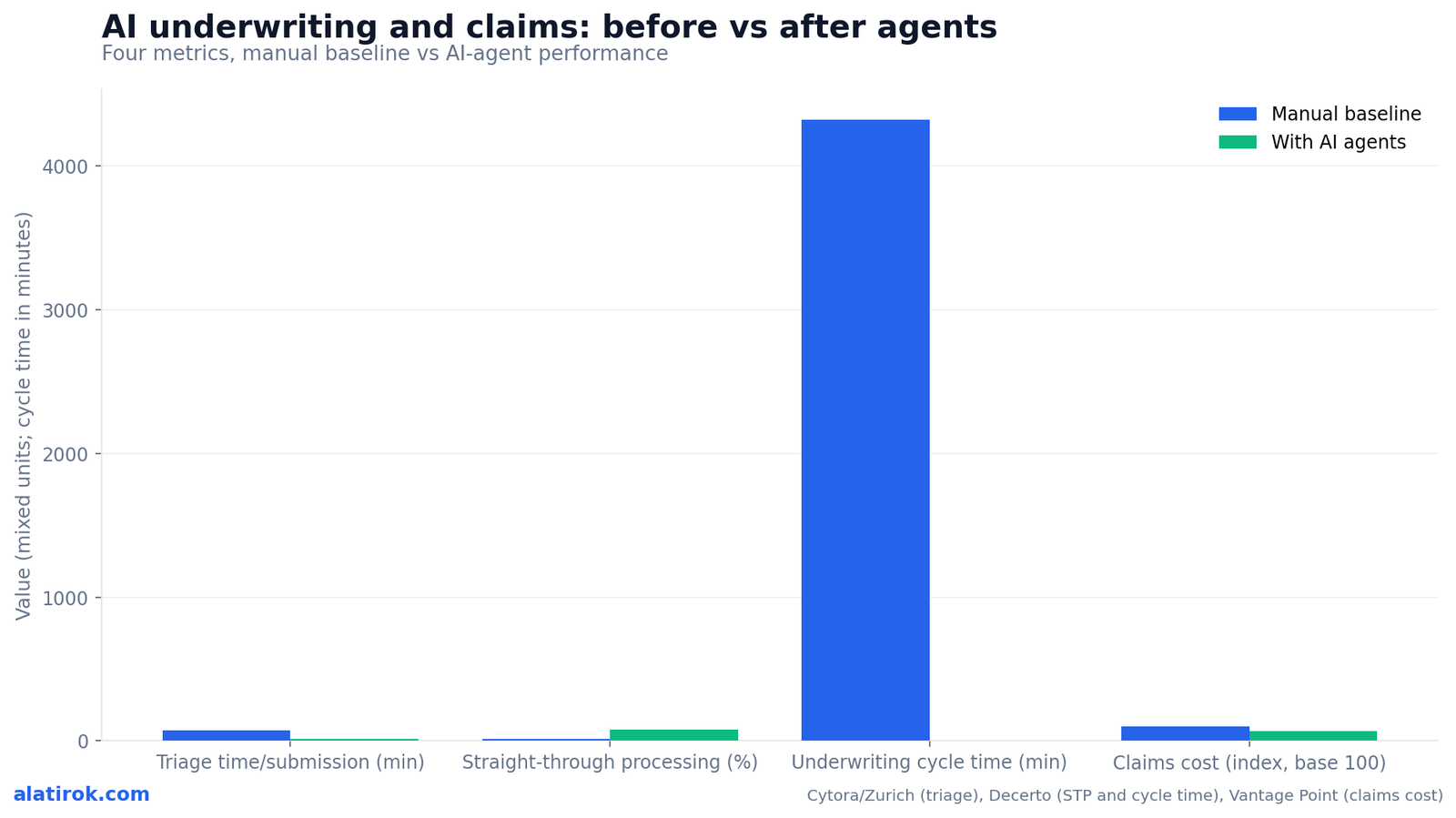

Before vs after: the numbers from real carrier rollouts

The single most credible before/after dataset comes from Zurich’s Cytora rollout, where manual triage time fell from 75 minutes to 15 minutes per submission, an 80% reduction, while digitisation accuracy rose from 70-80% to 98% and intake straight-through processing climbed from 10% to 95%. Zurich scaled this across five countries in 90 days and is on track for more than 20 markets over 16 months, making it the largest agentic-AI underwriting deployment with published baselines.

Markel’s number is the productivity headline: a 113% increase in underwriting productivity, measured as gross written premium per full-time employee, after deploying Cytora. Markel had estimated its underwriters previously spent 30% of their time on low-value tasks; automating that pre-underwriting work cut strategic-partner quote turnaround from roughly one day to two hours.

The chart below pairs the four metrics that recur across every credible rollout. Read it as the shape of the opportunity, not a guarantee: the Zurich and Markel figures are the realised end of a spectrum, and the industry-wide STP, cycle-time and claims-cost numbers from Decerto and Vantage Point describe what automatable submissions look like, not the full book. Complex, judgment-heavy risks still route to a human, by design.

Cytora vs CoverGo: the carrier-side platforms

For carrier-side underwriting and claims automation, Cytora leads on published before/after evidence and commercial-lines depth, while CoverGo wins on breadth across health, life and P&C plus a no-code core and tier-1 client roster. Both moved from point tools to full agentic platforms in early 2026, but they are aimed at different buyers.

Cytora’s March 2026 launch of Autopilot is the most ambitious of the two: an agentic capability that runs underwriting and claims workflows end-to-end from submission to decision, maintaining persistent context across emails, documents and calls, with what Cytora describes as explainable reasoning and fully auditable workflow steps. The pitch targets the 50% of underwriter and claims-handler time currently lost to reviewing submissions, chasing missing data and writing broker follow-ups. The Zurich and Markel deployments give it the strongest evidence base in this comparison.

CoverGo launched its insurance-specialised AI agents in late February 2026 and already has three running in production with tier-1 insurers and brokers: an Intelligent Document Processing agent, a Customer Support agent and a Quotation agent. Its IDP agent is live at Generali Hong Kong automating health-claims document handling. CoverGo’s clients include AXA, Bupa, Sun Life, Prudential and Marsh, and the platform is ISO 27001 and SOC 2 certified, which matters for regulated, multi-jurisdiction rollouts.

“Underwriters and claims handlers spend up to half their time reviewing submissions and chasing missing data. The whole agentic thesis is to give that half back.”

Cytora Autopilot launch positioning, March 2026

| Platform | Primary buyer | Flagship 2026 launch | Proven before/after metric | Lines covered |

|---|---|---|---|---|

| Cytora | Commercial carriers | Autopilot (end-to-end agentic, Mar 2026) | Zurich: triage 75 to 15 min; Markel: +113% productivity | Commercial P&C, specialty |

| CoverGo | Health/life/P&C carriers and brokers | IDP, Support and Quotation agents (Feb 2026) | Generali HK health-claims document automation (live) | Health, life, P&C |

| Travelers + OpenAI | Own policyholders (auto claims) | AI Claim Assistant voice agent (Feb 2026) | First-line auto-damage claim calls handled end to end | Personal auto claims |

| Zywave | Brokers and agencies | Four AI agents, Winter 2026 release | Rolling to 35+ early adopters; quoting agents to follow | Distribution and prospecting |

| SUPERAGENT AI | Retail agencies | Quoting AI Agent (Feb 2026) | Multi-carrier autonomous quoting (early access) | Personal and commercial quoting |

Travelers and the claims-side agent built with OpenAI

Travelers’ AI Claim Assistant, launched in February 2026 and built with OpenAI’s models and APIs, is the most consumer-facing agent in this comparison: a fully agentic voice service that takes auto-damage claim calls end to end and guides customers from consultation through submission. It is the clearest signal yet that a tier-1 US carrier will put a frontier-model agent on the phone with policyholders at the first point of contact.

The assistant uses speech recognition and language models to deliver what Travelers describes as the natural, comprehensive service customers expect from a live agent. It can surface relevant policy information, answer coverage questions, help a customer decide whether to file, then hand off to a digital flow for photo upload, appraisal, repair scheduling and rental reservation. Travelers says it selected OpenAI after benchmarking on reliability, enterprise security and scale.

What makes Travelers distinct is that it is not a horizontal platform you can buy; it is an in-house deployment of a foundation-model partnership. That is the build-versus-buy fork every large carrier now faces. Travelers chose to build on OpenAI’s stack rather than license Cytora or CoverGo for claims intake, which tells you that at sufficient scale, carriers will treat the model vendor as the platform and own the orchestration themselves.

Travelers building directly on OpenAI signals the fork ahead: large carriers with scale will license a frontier model and own orchestration; mid-market carriers will buy a vertical platform like Cytora or CoverGo that ships the insurance domain logic, audit trail and integrations out of the box.

Zywave vs SUPERAGENT: the distribution-side quoting agents

On the distribution side, Zywave is the broader, broker-workflow incumbent rolling out four AI agents across prospecting and outreach, while SUPERAGENT AI is the focused challenger attacking the single hardest task in retail insurance: autonomous multi-carrier quoting. Neither is a carrier underwriting engine; both aim to feed the underwriting funnel with more, better-prepared submissions.

Zywave’s Winter 2026 release shipped four agents to 35-plus early adopters: a Prospect Identification agent, a Lead Sourcing and Scoring agent, a Research and Enrichment agent, and an Outreach and Optimization agent. The strategy is to unify prospecting, content and engagement so producers spend time on customers rather than systems, with new-business and renewal quoting agents promised later in 2026. Zywave’s edge is its existing data assets and broker footprint.

SUPERAGENT AI went narrow and deep. Its Quoting AI Agent, launched in February 2026, autonomously gathers customer data, navigates multiple carrier rating engines simultaneously, optimises rates and generates quotes, with multi-channel contact over voice, SMS and email. The company frames it as solving the quoting bottleneck that has capped agency growth for decades. The risk is execution: navigating live carrier portals autonomously is brittle, and early-access claims need real-world durability data before they rank with Cytora’s deployed numbers.

Pros

Cons

How to choose, and where the limits are

Choose by your seat in the value chain: commercial carriers should shortlist Cytora for proven underwriting triage and Autopilot’s auditability; multi-line carriers in health and life should evaluate CoverGo; large carriers with engineering depth should weigh a Travelers-style direct foundation-model build; and agencies should pilot SUPERAGENT or Zywave against their actual quoting volume. Match the buyer to the platform’s center of gravity and most of the noise disappears.

The hard limit to internalise: every realised win in this comparison is in intake, triage, document parsing and quoting preparation, not in autonomous risk judgment. Straight-through processing rates of 70-90% describe the automatable slice of the book; the rest still routes to a human, and the better platforms are explicit about that boundary. Cytora leading Autopilot’s pitch with auditable, explainable steps is not incidental, it is what survives a regulator and an errors-and-omissions claim.

Two practical cautions. First, the before/after numbers are ceilings achieved after substantial data plumbing; budget for integration that runs longer than the demo implies. Second, governance is now table stakes: certifications like CoverGo’s ISO 27001 and SOC 2, and explainability like Cytora’s auditable workflow steps, should be hard requirements, not nice-to-haves, because an agent that cannot explain why it triaged a risk a certain way is a liability you cannot defend.

Treat every vendor before/after figure as a realised ceiling, not a starting point. Zurich’s 80% triage cut and Markel’s 113% productivity gain are real, but they followed months of data integration.The verdict

Cytora leads on proof; pick your platform by your seat in the chain

For 2026, Cytora is the category leader on evidence and commercial depth, CoverGo is the strongest multi-line and most certification-ready alternative, Travelers proves the direct-foundation-model build at scale, and Zywave and SUPERAGENT are the distribution-side bets to watch with the caveat that their hardest numbers are still unpublished. There is no single winner because there is no single buyer; the right answer is dictated by where you sit between the broker and the bind.

If you force a ranking on deployed, verifiable carrier outcomes today, Cytora is first, CoverGo second, and Travelers a category of one for in-house claims voice. The distribution agents are genuinely promising but earlier in their proof cycle, and a serious procurement process should demand the same kind of baseline-anchored numbers from them that the carrier-side platforms can already show.

Builder’s take

I build agent orchestration for a living at Cyntr, and insurance is the cleanest case study I know for where agentic AI is actually paying its way in 2026. The wins are real, but they cluster in a narrow band.

- Every carrier win in this comparison comes from intake, triage and document parsing, not from letting an agent make the bind/deny call. The economic value is in clearing the queue so a human decides faster.

- Treat vendor before/after numbers as ceilings, not floors. Zurich’s 75-to-15-minute triage cut is real, but it followed months of data plumbing most carriers underestimate by a factor of two.

- The defensible moat here is the same one I obsess over in my own stack: auditable, explainable reasoning on every step. Cytora’s Autopilot leading with ‘fully auditable workflow steps’ is not marketing fluff, it is what gets you past a regulator.

- Watch the wedge between broker-side tools (Zywave, SUPERAGENT) and carrier-side platforms (Cytora, CoverGo). They are converging on the same quote-and-bind workflow from opposite ends, and the carriers that win will own the data spine in the middle.

Frequently asked questions

AI underwriting agents are software systems that autonomously handle parts of the underwriting workflow, such as intake, triage, document parsing and pre-underwriting risk evaluation, then route decision-ready submissions to human underwriters. In 2026 the leading carrier-side examples are Cytora and CoverGo, which automate these steps inside core insurance operations rather than replacing the underwriter’s final risk judgment.

The most credible published figure comes from Zurich’s Cytora deployment, where manual triage time per submission dropped from 75 minutes to 15 minutes, an 80% reduction, while intake straight-through processing rose from 10% to 95%. Industry-wide, underwriting straight-through processing rates have moved from roughly 10-15% to 70-90%, and cycle times on automatable submissions have collapsed from about three days to three minutes.

It depends on your lines of business. Cytora has the deepest published before/after evidence in commercial P&C, including Zurich’s triage cut and Markel’s 113% productivity gain, and its Autopilot platform emphasizes auditable, end-to-end workflows. CoverGo covers health, life and P&C with a no-code core, has three agents in production with tier-1 insurers, and is ISO 27001 and SOC 2 certified, making it strong for multi-line, multi-jurisdiction carriers.

Travelers’ AI Claim Assistant, launched in February 2026 and built with OpenAI’s models and APIs, is a fully agentic voice service that handles incoming auto-damage claim calls end to end. It surfaces policy information, answers coverage questions, helps the customer decide whether to file, and then hands off to a digital flow for photo upload, appraisal, repair scheduling and rental reservation. It is an in-house deployment rather than a platform other carriers can license.

Zywave and SUPERAGENT AI are distribution-side tools for brokers and agencies, not carrier underwriting engines. Zywave’s Winter 2026 release added four agents covering prospecting, lead scoring, research and outreach, with quoting agents promised later in 2026. SUPERAGENT AI focuses on autonomous multi-carrier quoting. Both feed better-prepared submissions into the underwriting funnel rather than making underwriting decisions themselves.

Not in the deployments documented so far. Every realised 2026 win is in intake, triage, document parsing and quoting preparation, with complex or judgment-heavy risks still routed to a human. Straight-through processing rates of 70-90% describe the automatable slice of the book, not the entire portfolio. Leading platforms are explicit about this boundary and emphasize explainable, auditable reasoning so decisions can be defended to regulators and in errors-and-omissions disputes.

Primary sources

- Zurich scales Cytora AI across global underwriting (triage 75 to 15 min, 20+ markets) — Reinsurance News

- Markel records 113% underwriting productivity increase with Cytora — FF News

- Cytora launches Autopilot to deliver insurance workflows that run themselves — Applied Systems

- Travelers launches agentic AI Claim Assistant developed with OpenAI — Travelers Investor Relations

- CoverGo launches AI agents for insurance operations across the policy lifecycle — CoverGo

- Zywave unveils Winter 2026 release with four new AI agents — Business Wire

- SUPERAGENT AI announces world’s first insurance Quoting AI Agent — Business Wire

- Insurtech Trends 2026: AI claims and underwriting (STP, claims cost, cycle time) — Vantage Point

- AI in Insurance Market size to reach $154.39B by 2034 at 35.7% CAGR — Fortune Business Insights

- Global InsurTech Report Q4 2025 (AI share of funding) — Gallagher Re

Last updated: June 1, 2026. Related: Products.