Inside the reported 65B Series H that pushed Anthropic to a 965B post-money mark, the revenue math behind the trillion-dollar framing, and why it now sits above OpenAI.

What is the Anthropic valuation after the Series H round?

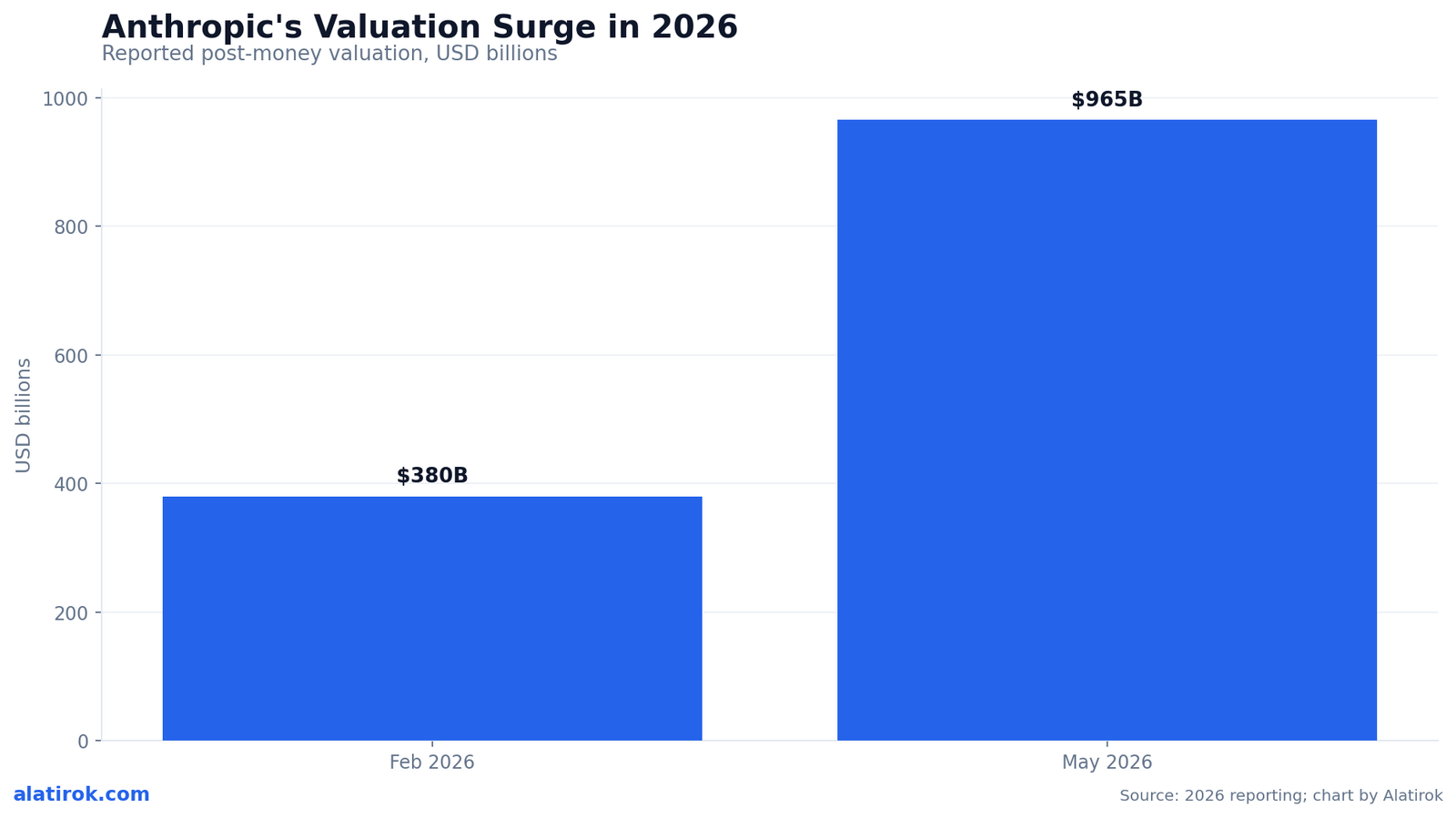

The Anthropic valuation reached a reported 965 billion dollars post-money on May 28, 2026, after a 65 billion dollar Series H financing, narrowly missing the trillion-dollar mark and overtaking OpenAI as the most valuable pure-play AI startup. The figures here are as reported by Anthropic and major outlets; private valuations are negotiated marks, not audited prices, so treat every number as directional.

The round is enormous on two axes at once. The 65 billion in fresh capital is itself one of the largest private financings ever assembled, and the 965 billion post-money valuation is roughly 2.5x the 380 billion mark set at the Series G just over three months earlier, per TechCrunch. Anthropic’s own announcement frames the raise as fuel for research and compute expansion rather than runway.

Several reports characterized this as likely Anthropic‘s last private round before a public listing. The presence of crossover and public-markets investors on the cap table is the tell that the next financing event could be an IPO at a valuation floor set here.

How does the funding round and its valuation history break down?

The Series H was co-led by Altimeter Capital, Dragoneer, Greenoaks, and Sequoia Capital, with the Anthropic valuation climbing from 183 billion in September 2025 to 380 billion in February 2026 to 965 billion in May 2026, a roughly 5.3x rise in eight months. That cadence is, as one analysis put it, unprecedented for a company at this scale.

Beyond the leads, the syndicate spans Capital Group, Coatue, D1 Capital Partners, GIC, ICONIQ, and XN, alongside institutional names including Baillie Gifford, Blackstone, Brookfield, Fidelity, and T. Rowe Price, per Anthropic. Strategic infrastructure partners Samsung, SK hynix, and Micron also joined, and roughly 15 billion of the total came from hyperscalers, including Amazon’s previously announced 5 billion commitment.

The table below tracks the reported valuation ladder. Each step should be read as a negotiated post-money mark at the time of the round, not a continuous market price.

Private valuations are post-money negotiated figures, not audited market prices. A 965 billion dollar mark means new investors bought a slice at an implied total value, not that the whole company could be sold for that today.

| Round | Date | Raised | Post-money valuation | Lead investors |

|---|---|---|---|---|

| Series F | Sep 2025 | Not specified | ~$183B | Not specified |

| Series G | Feb 2026 | ~$30B | ~$380B | GIC, Coatue |

| Series H | May 2026 | ~$65B | ~$965B | Altimeter, Dragoneer, Greenoaks, Sequoia |

What does Anthropic’s revenue run-rate actually show?

~$965B

Series H post-money valuation

As reported, May 28, 2026

~$47B

Reported revenue run-rate

Crossed earlier in May 2026

~$10B

Full-year 2025 revenue

Up ~10x year over year, per Anthropic

~20x

Implied revenue multiple

Valuation / run-rate, as reported

Anthropic‘s run-rate revenue reportedly crossed 47 billion dollars earlier in May 2026, up from a roughly 14 billion dollar run-rate cited at the February Series G and against roughly 10 billion in full-year 2025 revenue. The company has said revenue grew about 10x annually for three consecutive years, with the large majority coming from enterprise customers.

Run-rate is the load-bearing word. A run-rate annualizes a recent period, often the strongest recent month, so a 47 billion dollar run-rate does not mean 47 billion has been collected over the trailing year. Some analysts cited by CNBC have questioned whether the surge reflects double-counting or extrapolation from outlier months. I am not endorsing that skepticism, but I am flagging it: this is exactly the line item public-market diligence will stress-test first.

The growth story underneath is genuinely strong if it holds. Reported adoption includes eight of the Fortune 10 as Claude customers, and Claude Code’s run-rate was cited above 2.5 billion at the Series G. The open question is durability, not direction.

How does the Anthropic valuation compare to OpenAI?

The Anthropic valuation of 965 billion now sits above OpenAI’s reported 852 billion post-money mark from its 122 billion dollar March 2026 round, making Anthropic the most valuable AI-pure-play private company in absolute terms. Yet on revenue multiple, Anthropic is reportedly the cheaper of the two.

At roughly 965 billion against a 47 billion run-rate, Anthropic trades near 20x sales. OpenAI, at about 852 billion against roughly 20 billion in trailing revenue, trades closer to 42x, per reporting summarized by INDmoney. So the company with the higher headline value carries the lower multiple, which is the crux of the bull case.

The comparison has caveats stacked on caveats. OpenAI’s revenue base and Anthropic’s run-rate are measured differently, the rounds closed two months apart, and both numbers are reported rather than audited. The clean takeaway is narrow: Anthropic leapfrogged OpenAI on price while claiming a less stretched multiple.

“The company with the higher headline value carries the lower multiple. That single inversion is the entire bull case for the Series H.”

Alatirok analysis

Does the trillion-dollar Anthropic valuation framing hold up?

The trillion-dollar framing is a rounding-up of the reported 965 billion mark, and whether it holds depends entirely on whether the 47 billion run-rate proves to be repeatable recurring revenue rather than an annualized peak. At 20x sales the multiple is defensible by 2026 AI-lab standards; the risk lives in the denominator, not the multiple itself.

Two structural factors complicate the math. First is the circular capital loop: a meaningful share of round dollars flows back out as multi-year compute commitments to Amazon, Google, and Broadcom, so some capital is effectively prepaid infrastructure rather than free cash. Second is the run-rate measurement problem above. Public-market analysts, as the INDmoney piece notes, price repeatability, not momentum.

If revenue keeps compounding at even a fraction of its recent pace, a 20x multiple compresses quickly and 965 billion looks conservative in hindsight. If the run-rate normalizes after a strong stretch, the same number looks aggressive. Both outcomes are live, and the IPO is where the disagreement gets settled in public.

Why “run-rate” deserves scrutiny

Run-rate annualizes a short recent window. A 47 billion dollar run-rate from a strong month is not the same as 47 billion in trailing-twelve-month revenue. Enterprise usage can also spike around launches, and partner credits or committed-spend deals can inflate recognized figures. None of this proves the number is wrong; it means the multiple sits on a denominator that public diligence will test line by line.What the circular capital loop means

Reports describe Anthropic committing to large multi-year infrastructure spend with the same hyperscalers and chipmakers investing in the round. That recycles capital between investment and cost of goods sold, which inflates gross dollar flows on both sides and makes clean unit-economics harder to read from the outside. It is common in capital-intensive AI, but it is a reason to discount headline figures.What should builders and investors take away?

A real lead, on a multiple that still needs auditing

For builders, the practical signal from the Anthropic valuation is supply security and pricing stability, not the headline number; for investors, the decision reduces to whether the 47 billion run-rate is durable enough to justify a 20x multiple at IPO. Use the checklist below to separate the financing noise from operating reality.

The presence of Samsung, SK hynix, and Micron on the cap table is the detail I weight most as an operator. Memory and fab capacity are the real ceiling on inference throughput, and locking those relationships matters more to my latency budget than any valuation milestone. The round buys Anthropic time and compute; whether it buys durable margin is the IPO’s question to answer.

Every dollar amount here, round size, valuation, run-rate, and multiple, is as reported by Anthropic and the press. Private marks are negotiated, run-rates are annualized estimates, and OpenAI comparisons mix differently-measured numbers. Verify against primary filings before making any decision.

Decision checklist before you anchor on the 965B number

1) Is the metric run-rate or trailing revenue? Default to skepticism on run-rate. 2) How much of the raise is prepaid compute via the circular loop versus deployable capital? 3) Does the revenue multiple (~20x) hold if growth halves? 4) For contracts: are you pricing on token cost and rate-limit headroom, or on valuation hype? 5) For IPO exposure: would you underwrite repeatability, since public markets price that, not momentum?Builder’s take

I build on these models for a living. Cyntr, my agent orchestration runtime, routes production workloads across frontier APIs, so a number like 965 billion is not abstract trivia to me. It is the discount rate baked into every vendor I depend on. Here is how I read this round as an operator rather than a spectator.

- A 20x revenue multiple is the cheapest of the megacap labs right now, but “cheapest” only matters if the $47B run-rate is real recurring revenue and not annualized peaks plus partner credits. Treat the multiple as a hypothesis, not a fact.

- The circular capital loop, where round dollars flow back out to Amazon, Google, and Broadcom as multi-year compute commitments, means a chunk of this raise is effectively prepaid infrastructure. I read it as capacity insurance, not pure war chest.

- For builders, the strategic signal is supply security. Samsung, SK hynix, and Micron joining the cap table tells me Anthropic is locking memory and fab access, which is the actual bottleneck for the inference I am paying for.

- If you are pricing a multi-year contract against Claude, anchor on capability and rate-limit headroom, not the valuation headline. The 965B number is a financing event; your unit economics are decided by token prices and uptime.

Frequently asked questions

Anthropic was reportedly valued at about 965 billion dollars post-money after its 65 billion dollar Series H round announced on May 28, 2026. That is roughly 2.5x its 380 billion dollar Series G valuation from February 2026. As with all private rounds, this is a negotiated post-money mark rather than an audited market price.

Yes, on a reported basis. Anthropic’s 965 billion dollar Series H mark sits above OpenAI’s reported 852 billion dollar post-money valuation from its 122 billion dollar March 2026 round, making Anthropic the most valuable AI-pure-play private company in absolute terms. The two figures were set roughly two months apart and are measured differently, so the lead is real but the comparison has caveats.

The Series H was co-led by Altimeter Capital, Dragoneer, Greenoaks, and Sequoia Capital. The broader syndicate included Capital Group, Coatue, D1 Capital Partners, GIC, ICONIQ, and XN, plus institutional investors like Baillie Gifford, Blackstone, Fidelity, and T. Rowe Price, and strategic partners Samsung, SK hynix, and Micron.

Anthropic reportedly crossed a 47 billion dollar annualized run-rate earlier in May 2026, up from roughly 14 billion at the February Series G, against about 10 billion in full-year 2025 revenue. Run-rate annualizes a recent period and is not the same as trailing-twelve-month revenue, so the figure should be treated as a reported estimate.

It depends on the revenue denominator. At about 965 billion against a 47 billion run-rate, Anthropic trades near 20x sales, the lowest multiple among the AI megacaps despite the highest absolute value. That multiple is defensible if the run-rate is durable recurring revenue, but some analysts have questioned whether the surge reflects annualized peaks or double-counting. Public markets will settle it at IPO.

No specific IPO date has been confirmed. Multiple reports describe the Series H as likely Anthropic’s final private round, and the presence of public-markets investors such as T. Rowe Price, Fidelity, and Baillie Gifford suggests positioning for a listing. The 965 billion dollar valuation effectively sets a reference floor for any future public debut.

Primary sources

- Anthropic raises $65B in Series H funding at $965B post-money valuation — Anthropic

- Anthropic raises $65 billion, nears $1T valuation ahead of IPO — TechCrunch

- Anthropic tops OpenAI as most valuable AI startup, nears $1 trillion valuation — CNBC

- Anthropic raises another $30 billion in Series G with a new value of $380 billion — TechCrunch

- Anthropic $965B Valuation: Series H Funding and IPO Outlook — INDmoney

Last updated: May 31, 2026. Related: Capital.