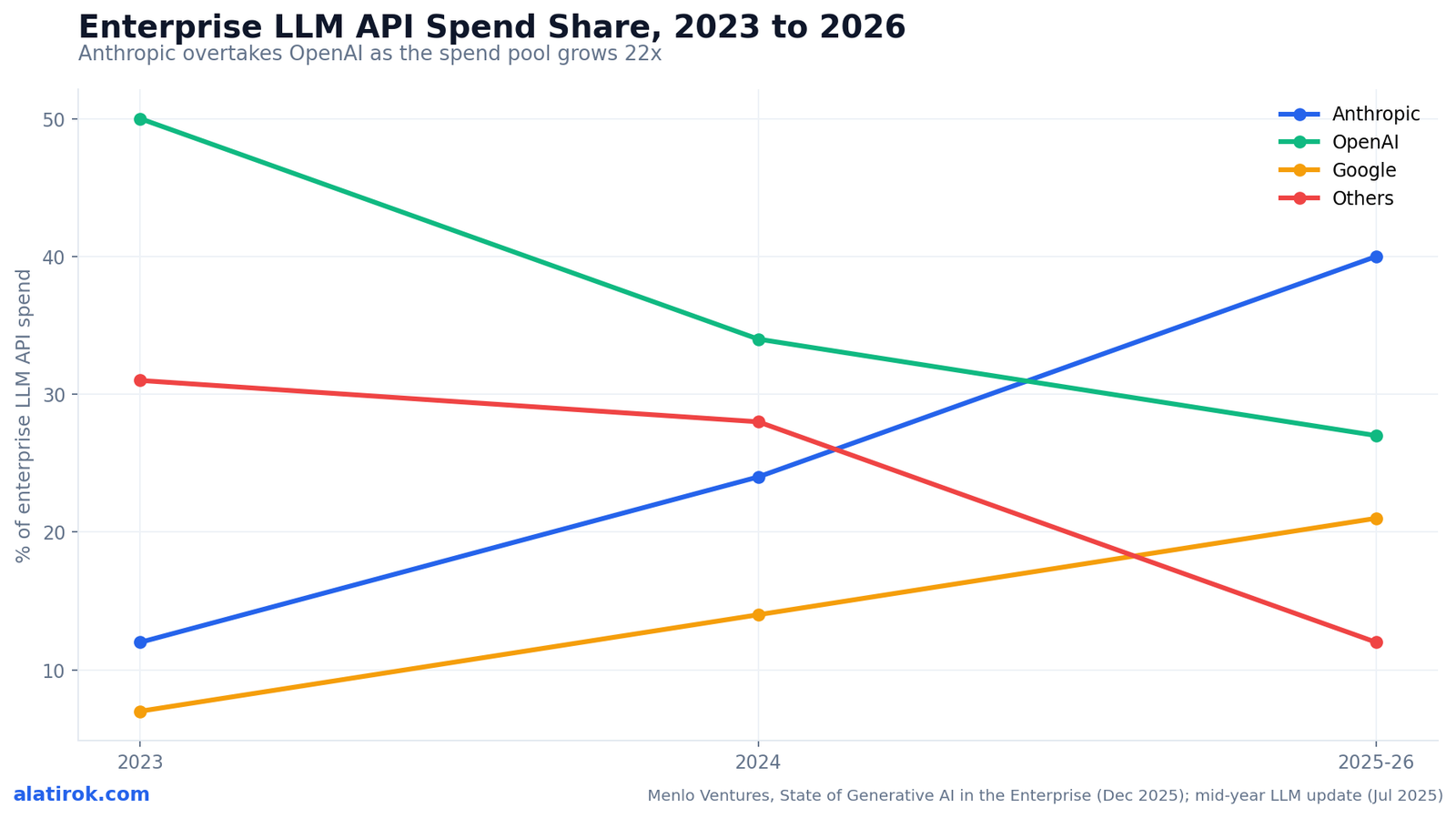

Anthropic now earns 40 cents of every enterprise LLM API dollar, OpenAI has fallen to 27%, and Google tripled to 21% – all while the spend pool itself exploded from $1.7B to $37B in two years.

The enterprise LLM market share 2026 picture, in one number

Anthropic now captures 40% of enterprise LLM API spend, OpenAI has fallen to 27%, and Google has tripled to 21% – a complete inversion of the 2023 ranking, according to Menlo Ventures’ December 2025 “State of Generative AI in the Enterprise” report. Three years ago, OpenAI owned half the market and Anthropic was a 12% afterthought. The leaderboard has since flipped end to end. That makes the enterprise LLM market share 2026 picture almost unrecognizable next to the 2023 ranking.

The headline is not just that Anthropic passed OpenAI. It is the speed and completeness of the reversal. Anthropic’s share climbed 12% to 24% to 40% across three annual reads. OpenAI’s collapsed from roughly 50% to 27% – it lost nearly half of its enterprise position in twenty-four months. Google, written off as a slow mover in 2023 at 7%, is now a credible number three at 21%.

What makes this more than a vendor squabble is the backdrop. The enterprise generative-AI spend pool grew from $1.7 billion in 2023 to $11.5 billion in 2024 to $37 billion in 2025 – a 22x expansion in two years. So Anthropic is taking a larger slice of a dramatically larger pie. A 40% share of $37B is a different universe than 40% of $1.7B would have been. This is the rare market where you can lose share and still grow revenue, and gain share and grow it explosively.

How the enterprise LLM market share 2026 split was built, year by year

The shift happened in two distinct phases: a mid-2025 crossover where Anthropic first passed OpenAI on API usage, and a year-end consolidation where Anthropic pulled clear to 40% of spend. Menlo’s July 2025 mid-year update already showed Anthropic at 32% of enterprise usage versus OpenAI’s 25% and Google’s 20%, on an LLM spend base that had doubled in six months from $3.5B (late 2024) to $8.4B. In short, enterprise LLM market share 2026 is now a three-horse race, not a one-model default.

By the December 2025 full report, the spend-weighted picture had hardened: Anthropic 40%, OpenAI 27%, Google 21%, and everyone else – Meta’s Llama, Mistral, Cohere, DeepSeek and the rest – sharing the remaining 12%. The chart below tracks the full three-year arc as a share-of-spend race, with the total pool plotted as the inset reference so you can see both the share shift and the pool expansion at once.

Two mechanics drove the curve. First, Anthropic held the top of the coding and agentic benchmarks for roughly 18 months after Claude 3.5 Sonnet shipped in mid-2024, and coding is the single largest enterprise workload. Second, Google’s tripling came less from benchmark wins than from distribution: Gemini rides into accounts that already pay Google Cloud, turning model selection into a procurement default rather than a bake-off.

The 40% enterprise share with 2% consumer mindshare paradox

Anthropic commands roughly 40% of enterprise LLM spend while drawing only about 2% of consumer chatbot website traffic – the clearest sign yet that enterprise revenue and consumer fame have fully decoupled. ChatGPT still dominates the public imagination and the app-store charts. But when technical leaders spend production budgets, they are buying Claude.

This divergence is the most strategically important fact in the entire report, and most coverage misses it. The consumer chatbot race – measured in monthly active users and viral moments – and the enterprise API race – measured in production token spend – are now two different markets with two different winners. A company can lose the dinner-party conversation and win the procurement cycle.

For buyers, the lesson is to ignore brand gravity. The model your engineers reach for on a personal account is a weak predictor of which model survives a rigorous internal eval. For investors, it means consumer DAU charts are a poor proxy for enterprise durability. The money and the mindshare have parted ways.

If you are benchmarking your own provider choice, weight production eval results over public popularity. The market’s biggest enterprise winner is roughly the 5th-most-famous consumer brand. Fame is not a buying signal.

Where the $37B actually goes: spend by category

$37B

Enterprise gen-AI spend, 2025

Up from $11.5B in 2024 and $1.7B in 2023

$12.5B

Foundation model API spend

The pool Anthropic, OpenAI and Google fight over

$8.4B

General-purpose copilots

Largest single application category

6%

Of the global software market

Reached in three years – fastest in software history

Applications captured more than half of all enterprise AI investment in 2025 at $19 billion, with general-purpose copilots ($8.4B), coding and developer tools ($7.3B), and industry-specific vertical AI ($3.5B) as the three largest application buckets. Infrastructure – foundation-model APIs, training, and tooling – took the other roughly $18 billion, of which foundation-model APIs alone were $12.5 billion.

Inside vertical AI, healthcare is the clear leader at $1.5 billion – about 43% of the vertical category – ahead of legal at $650 million. The coding line is what underwrites Anthropic’s position: when more than half of departmental AI spend flows to developer tools, and one vendor has owned the coding benchmarks for a year and a half, share follows the workload.

The stat highlights below frame the scale of the pool and its concentration. Note that AI applications now represent about 6% of the entire software market after just three years – which Menlo calls the fastest growth rate in software history.

| Category | 2025 spend | Notable detail |

|---|---|---|

| Infrastructure (incl. model APIs) | ~$18B | Foundation-model APIs alone: $12.5B |

| General-purpose copilots | $8.4B | Largest application bucket |

| Coding and developer tools | $7.3B | Underwrites Anthropic’s lead |

| Vertical / industry-specific AI | $3.5B | Healthcare leads at $1.5B |

| Total enterprise gen-AI | $37B | 3.2x year-over-year growth |

Why OpenAI fell and Google climbed

OpenAI’s decline to 27% reflects share erosion, not revenue collapse – it lost ground on a fast-growing pool because brand-led adoption gave way to workload-led evaluation, while its lead narrowed on reasoning and disappeared on code. In 2023, picking OpenAI was the safe default. By 2025, defaults stopped winning once teams ran real production tests.

Google’s path is different and, in some ways, more durable. Its jump from 7% to 21% leaned on distribution: Gemini is bundled into the Google Cloud relationships that enterprises already have, so adoption is a contract addendum rather than a new vendor onboarding. That is a slower-burning but stickier advantage than any single benchmark win.

The cautionary note for Anthropic: leadership built on a benchmark lead is rentable, not owned. OpenAI’s GPT-5 line and Google’s Gemini cadence are explicitly aimed at the coding workloads that anchor Anthropic’s 40%. Share this concentrated in one use case is share that can move quickly if the benchmark gap closes.

“This is the rare market where one vendor can lose half its share and still grow revenue – because the pool itself grew 22x in two years.”

On the $1.7B to $37B expansion

What buyers should actually do with these numbers

Share is a snapshot; the pool is the story

Treat the 40/27/21 split as evidence that single-vendor lock-in is a real risk and multi-model routing is cheap insurance – not as a mandate to standardize on the current leader. The market reordered itself completely in 24 months. Whatever is #1 today is a snapshot, not a destiny.

The pros and cons below weigh consolidating on Anthropic today against staying provider-flexible. The honest answer for most teams is hybrid: route coding and agentic work to whichever model wins your internal eval this quarter, keep a fallback wired in, and re-run the eval every model release. Switching cost – tuned prompts, evals, and agent scaffolding – is the real moat, and it accrues to whichever vendor you let it accrue to.

Pros

Cons

Builder’s take

I buy model tokens for two products – Cyntr and Loomfeed – so this report is not abstract to me. The 40/27/21 split matches what I see in my own invoices and in the way I route work.

- The number that actually moved buyers was not a benchmark – it was reliability under real workloads. I switched coding-heavy paths to Claude because the diff quality held up across a full agent loop, not because of a leaderboard screenshot.

- Anthropic’s 40% enterprise share against ~2% consumer mindshare is the single most important strategic fact here: enterprise revenue and consumer fame have fully decoupled, and most coverage still conflates them.

- Google tripling to 21% is the quiet story. When you already pay Google for cloud, Gemini becomes the path of least resistance, and procurement loves one bill. I expect that number to keep climbing on distribution alone.

- The pool grew 22x in two years to $37B. Share percentages are a fun horse race, but the real lesson for builders is that the prize itself is compounding faster than any single vendor’s slice.

- Switching cost is now the moat. Once your agents, evals, and prompt libraries are tuned to one model family, moving is a project, not a config change. Multi-model routing from day one is cheap insurance.

Frequently asked questions

Per Menlo Ventures’ December 2025 report, Anthropic leads enterprise LLM API spend at 40%, OpenAI is second at 27%, and Google is third at 21%, with all other providers (Llama, Mistral, Cohere, DeepSeek, etc.) sharing the remaining 12%. This reverses the 2023 ranking, when OpenAI held about 50% and Anthropic just 12%.

Anthropic’s share rose 12% to 24% to 40% across three annual reads, largely by leading coding and agentic benchmarks for roughly 18 months after Claude 3.5 Sonnet shipped in mid-2024. Coding is the largest enterprise workload, so as buyers shifted from brand-led defaults to production evals, spend followed the model that won those evals.

Total enterprise generative-AI spend reached $37 billion in 2025, up from $11.5 billion in 2024 and $1.7 billion in 2023 – a 22x increase in two years. Of that, foundation-model APIs accounted for $12.5 billion, and AI applications now represent about 6% of the entire global software market.

Anthropic earns roughly 40% of enterprise LLM spend while drawing only about 2% of consumer chatbot website traffic. The consumer market (where ChatGPT dominates app-store charts) and the enterprise API market (measured in production token spend) have decoupled into two different races with two different winners. Consumer popularity is a weak predictor of enterprise durability.

Google roughly tripled its enterprise LLM API spend share from 7% in 2023 to 21% in 2025. Much of that gain came from distribution rather than benchmark wins – Gemini is bundled into existing Google Cloud relationships, making model selection a procurement default for accounts already on the platform.

In 2025, applications took more than half of enterprise AI investment at $19 billion: general-purpose copilots ($8.4B), coding and developer tools ($7.3B), and vertical industry-specific AI ($3.5B, led by healthcare at $1.5B). Infrastructure – including foundation-model APIs ($12.5B), training, and tooling – accounted for roughly $18 billion.

Primary sources

- 2025: The State of Generative AI in the Enterprise — Menlo Ventures

- Enterprise Investment Hit $37B in 2025, Tripling in One Year — GlobeNewswire

- Menlo Ventures Report: Enterprise LLM Spend Reaches $8.4B as Anthropic Overtakes OpenAI — BigDATAwire (HPCwire)

- Menlo Ventures’ 2025 State of Generative AI Report (Yahoo Finance) — Yahoo Finance

- Anthropic Hits 40% of Enterprise AI Spend: What SMBs Gain — Appalach.AI

Last updated: June 1, 2026. Related: Capital.