SK Hynix, Samsung, and Micron split the most contested component in AI. Here is the HBM market share 2026 picture, the pricing, and the HBM3E-to-HBM4 handoff.

What is the HBM market share 2026 split?

In 2026 SK Hynix holds roughly 58% of the HBM market, Samsung about 25%, and Micron near 17% — a three-way split where one vendor still controls more than half of supply. Those are midpoints of the ranges analysts are publishing: Counterpoint and Astute Group bracket SK Hynix at 50-62%, Samsung at 25-40%, and Micron at 5-20% for the year, reflecting how fast share is moving as HBM4 ramps. That is the HBM market share 2026 story in one line: highly concentrated, and increasingly spoken for in advance.

High-bandwidth memory is the stacked DRAM that sits next to the logic die on every modern AI accelerator. An NVIDIA Blackwell or Rubin GPU is useless without it — the compute starves waiting for data. That makes HBM the single most supply-constrained component in the AI buildout, and the reason a handful of Korean and American fabs effectively gate how fast the industry can scale.

The story of the HBM market share 2026 is less about marketing and more about manufacturing yield. SK Hynix earned its lead by being first to ship working 12-high stacks at volume with the yields NVIDIA needs. Samsung spent most of 2025 climbing back from a qualification stumble, and Micron went from a rounding error to a credible third source faster than anyone expected.

How the three vendors got here: the Q2 2025 inflection

62%

SK Hynix HBM share, Q2 2025

Counterpoint baseline quarter

2% to ~17%

Micron HBM share, 2023 to 2026

Fastest climb in the field

~58%

SK Hynix HBM share, 2026

Midpoint of 50-62% range

The pivotal moment was Q2 2025, when Micron overtook Samsung to become the world’s number-two HBM supplier for the first time. Counterpoint pegged that quarter at SK Hynix 62%, Micron 21%, and Samsung 17% — a humiliating result for Samsung, historically a memory titan, and a breakout for Micron, which held just 2% of HBM as recently as 2023.

By Q3 2025 the picture shifted again. SK Hynix slipped to roughly 53-57% as Samsung clawed back, with reports putting Samsung’s HBM revenue share back above Micron’s at 22% and higher as fresh HBM3E qualifications landed at major customers. Micron held roughly flat near 11% on a revenue basis. The volatility is the point: in a normal memory market, share moves a point or two a year, not ten points a quarter.

Three forces drove the churn. First, qualification — getting a stack certified by NVIDIA or a hyperscaler is a binary event that can swing share overnight. Second, yield on tall stacks, where SK Hynix’s lead is widest. Third, customer concentration: with NVIDIA, Google, Amazon, and a handful of others buying nearly everything, winning or losing one socket reshuffles the table.

Producing 1GB of HBM consumes roughly 4x the wafer capacity of standard DRAM, per TrendForce. That multiplier is why a relatively small revenue category can swallow about 20% of the world’s entire DRAM wafer output in 2026 — and why HBM, not logic, is often the first thing to run short.

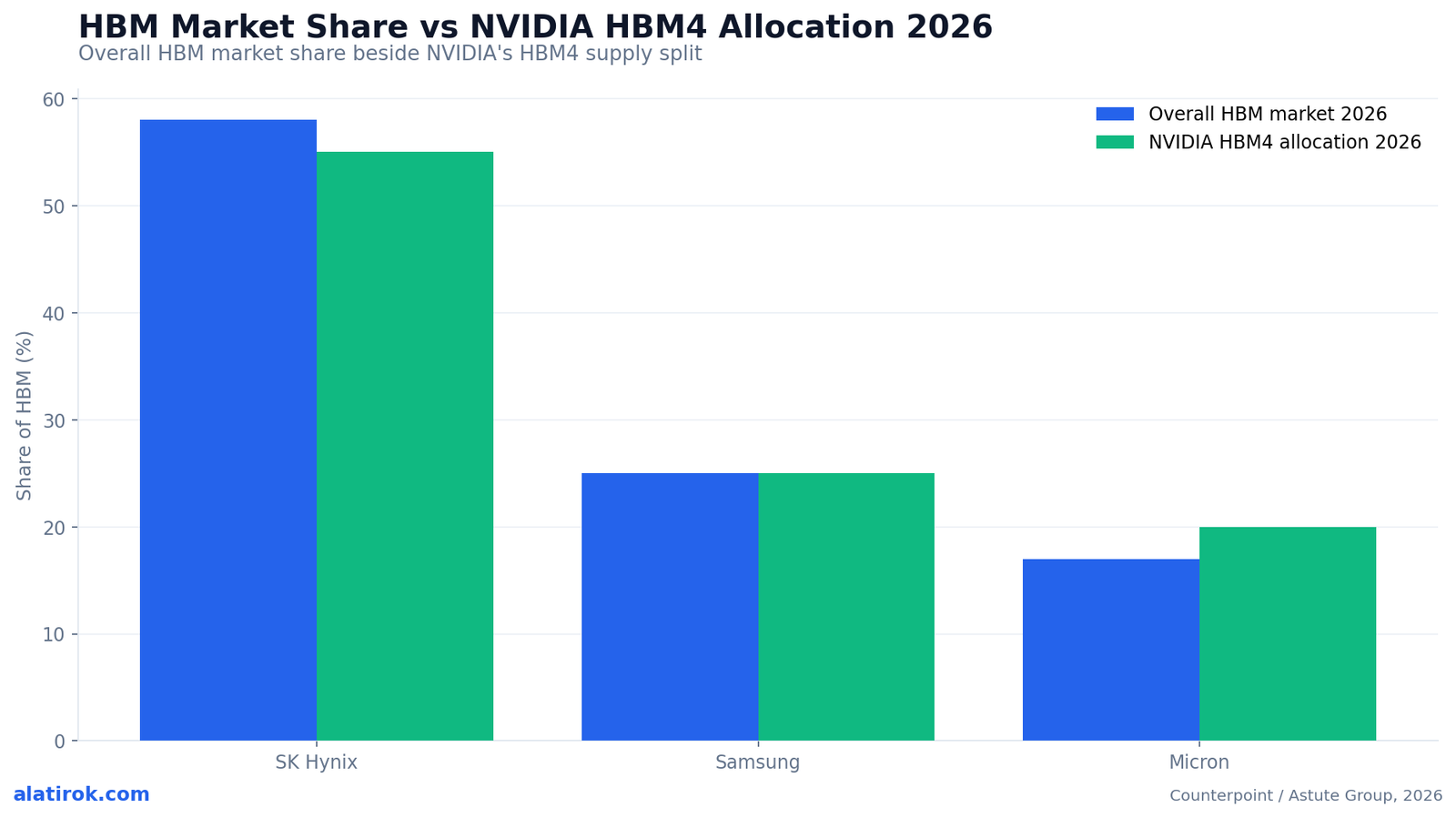

The HBM market share 2026 chart: market vs. NVIDIA allocation

The overall HBM market share 2026 and NVIDIA’s specific HBM4 allocation look similar but not identical — and the difference is where Micron and Samsung are fighting hardest. Across the whole market, SK Hynix sits near 58%, Samsung near 25%, and Micron near 17%. On NVIDIA’s HBM4 orders specifically, Astute Group’s read is SK Hynix in the mid-50s, Samsung in the mid-20s, and Micron near 20%.

Read the two bars side by side and a pattern emerges. Micron punches slightly above its overall weight on NVIDIA’s HBM4 because it qualified early and NVIDIA wants a genuine third source for leverage and resilience. Samsung’s HBM4 slice is roughly in line with its market share — a recovery from where it sat a year ago, but still short of the 30%-plus some forecasts say it can reach if its HBM4 parts clear qualification cleanly in the back half of 2026.

The per-stack price line tells the commercial story underneath the share fight. Silicon Analysts estimates run near $200 for an HBM3 stack, about $300 for HBM3E, and roughly $500 for HBM4. Each generation packs more dies, more bandwidth, and a fatter margin — which is exactly why all three vendors are racing to shift their mix toward the newest, most expensive product.

“In a normal memory market, share moves a point or two a year. In HBM right now, it moves ten points a quarter.”

On the volatility of HBM market share 2026

The unusual 20% HBM3E price hike

Heading into 2026, Samsung and SK Hynix raised HBM3E supply prices by roughly 20% — a move TrendForce flagged as unusual because prices normally fall, not rise, as a newer generation arrives. Conventional wisdom said HBM3E should soften once HBM4 shipped. Instead, demand for HBM3E kept climbing and vendors hiked into the transition.

The driver is a wave of HBM3E-hungry accelerators all shipping at once. NVIDIA’s H200 carries six HBM3E stacks each, and approval to export H200 to China pulled demand forward. Google’s seventh-generation TPU reportedly integrates eight HBM3E stacks per chip, and Amazon’s Trainium3 uses four. Every one of those sockets competes for the same finite stack output, and custom ASICs from the hyperscalers are now a structural buyer, not a side bet.

For anyone running large-scale inference, the math is brutal and worth doing explicitly. At roughly $300 per HBM3E stack and six to eight stacks per accelerator, memory alone is $1,800 to $2,400 of bill-of-materials before the logic die, packaging, or board. A 20% hike on that line flows straight into cloud GPU pricing — and then into the per-token cost of every model you serve.

Analysts suggest budgeting roughly a 20% premium for HBM4 over HBM3E at launch, with some moderation possible as three-way competition heats up in the second half of 2026. If your 2026-2027 capacity plan assumes flat memory cost, it is already wrong.

| Generation | Est. price per stack | Typical bandwidth | Where it ships in 2026 |

|---|---|---|---|

| HBM3 | ~$200 | Up to ~819 GB/s | Legacy H100-class accelerators |

| HBM3E | ~$300 | ~896-1,280 GB/s | H200, TPU v7, Trainium3, mid-2026 mainstream |

| HBM4 | ~$500 | ~1.5-2 TB/s | Vera Rubin and next-gen ASICs, ramps from Q3 |

The HBM3E-to-HBM4 handoff and why it dictates 2026

TrendForce projects 2026 HBM revenue will split roughly 55% HBM4 and 45% HBM3E, with HBM4 ramping from the third quarter to rapidly absorb demand once served by HBM3E. That single mix shift is the most important operational fact of the year: the industry is pivoting its highest-value product line mid-stride, under maximum demand, with no slack.

HBM4 is not a routine upgrade. It widens the memory interface to 2,048 bits, pushes bandwidth past 1.5 TB/s per stack, and demands tighter integration with the logic die. NVIDIA has reportedly explored relaxing some HBM4 specs as suppliers wrestle with capacity and yield limits — a sign of how tight the engineering margins are. Whoever ships 12-high and then 16-high HBM4 at acceptable yield first captures the richest sockets of the cycle.

This is why the handoff, not the headline share number, decides 2026. SK Hynix is reported to be supplying close to two-thirds of NVIDIA’s HBM4 in some accounts, while Samsung targets early delivery to prove it belongs in the top tier. Micron’s job is to stay qualified and reliable enough that NVIDIA keeps it near 20%. The share table you see in December 2026 will be written almost entirely by who executes this transition between now and Q4.

What does HBM4’s 2,048-bit interface actually change?

HBM3E uses a 1,024-bit interface per stack. HBM4 doubles that to 2,048 bits, which is the main lever behind the jump past 1.5 TB/s per stack. The wider bus also tightens the coupling between memory and the logic die, which is part of why HBM4 is harder to manufacture and yield than a simple die-count increase would suggest.Why does HBM4 ramp specifically from Q3 2026?

Volume HBM4 lines up with the launch window for NVIDIA’s Vera Rubin platform and the next wave of hyperscaler ASICs. 12-high HBM4 enters mass supply early in 2026, with 16-high parts pushed for the second half — so the revenue crossover to a majority-HBM4 mix lands in the back half of the year.Capital and capacity: the bottleneck behind the bottleneck

HBM revenue is forecast to rise from about $3.17 billion in 2025 to roughly $3.98 billion in 2026, per Mordor Intelligence, with a ~25.58% CAGR pushing toward $12.44 billion by 2031. But the dollar figure understates HBM’s gravity. Because HBM eats roughly 4x the wafer area of standard DRAM per gigabyte, this comparatively modest revenue line distorts the entire memory industry around it.

TrendForce estimates AI will consume close to 20% of global DRAM wafer capacity in 2026, with HBM and GDDR7 leading that draw against an estimated 40-exabyte global DRAM pool. When a fifth of the world’s DRAM wafers are diverted to AI memory, conventional server and PC DRAM tightens too — which is why server DRAM contract prices were reported rising 60-70% in some quarters. The HBM bottleneck radiates outward into every memory category.

For investors and operators, the takeaway is that HBM is a capacity-allocation problem dressed as a market-share story. The constraint is not demand — demand is effectively unlimited at current prices — but how many wafer-starts each vendor can convert into yielding, qualified stacks. That is the real moat, and it is why a third entrant like Micron reaching ~17% matters: it is the only thing keeping a structural shortage from becoming a single-vendor monopoly.

HBM is a capacity-allocation problem wearing a market-share costume. The scarce resource is not demand — it is yielding, qualified wafer-starts, and only three companies on Earth can supply them at scWho wins the HBM market share 2026 fight?

A three-horse race the whole AI industry is betting on

SK Hynix wins 2026 on volume and yield, Samsung wins the recovery narrative, and Micron wins as the indispensable third source — but no single vendor wins outright, and that is the healthiest outcome for AI buyers. The structural shortage means all three sell everything they can make; the contest is over mix, margin, and the HBM4 sockets that define the next cycle.

If you are building on top of this stack rather than inside it, the strategic move is to treat HBM cost as a planning input, not a footnote. Model the HBM4 premium, assume memory pricing rises through a node transition rather than falls, and remember that your inference economics are downstream of three fabs you will never visit. The HBM market share 2026 table is, in the end, a forecast of how expensive intelligence will be to serve.

Pros

Cons

Builder’s take

I build orchestration software, not silicon, but every cost curve I plan against bends back to one part I cannot buy more of. HBM is the choke point nobody on the application side sees until the cloud invoice arrives.

- The HBM market share 2026 numbers are really a yield story. SK Hynix keeps ~58% not because the market loves a monopoly but because it ships working 12-high stacks at volume while rivals are still qualifying.

- A ~20% HBM3E price hike heading into a node transition is the tell. Vendors raise prices on the OLD generation when demand outruns supply that badly. That is a seller’s market, full stop.

- If you run inference at scale, model the HBM4 premium now. A jump from roughly $300 to $500 per stack, times 6-8 stacks per accelerator, is real money baked into every token you serve.

- Three suppliers is fragile but better than one. Micron clawing from 2% to ~17% is the single best thing that happened to AI buyers in two years, even if you never order a chip directly.

Frequently asked questions

For 2026, analysts at Counterpoint and Astute Group place SK Hynix at roughly 50-62% of the HBM market (about 58% at the midpoint), Samsung at 25-40% (around 25%), and Micron at 5-20% (around 17%). SK Hynix retains a clear lead, but it is now a genuine three-way market rather than a near-monopoly.

Astute Group’s 2026 read puts NVIDIA’s HBM4 allocation at SK Hynix in the mid-50% range, Samsung in the mid-20s, and Micron near 20%. Some later reports suggest SK Hynix could supply closer to two-thirds of NVIDIA’s HBM4 for the Vera Rubin platform, depending on how Samsung’s and Micron’s qualifications progress through 2026.

TrendForce reported that Samsung and SK Hynix raised HBM3E prices by roughly 20% for 2026, calling it unusual because prices normally fall as a newer generation arrives. The hike was driven by stronger-than-expected demand from NVIDIA’s H200 (six HBM3E stacks each), Google’s TPU v7 (eight stacks), and Amazon’s Trainium3 (four stacks), all competing for the same finite supply.

Silicon Analysts estimates run near $200 for an HBM3 stack, about $300 for HBM3E, and roughly $500 for HBM4. With six to eight stacks per accelerator, HBM alone can represent $1,800 to $4,000 of an AI chip’s bill of materials before logic, packaging, or board costs.

TrendForce projects 2026 HBM revenue will split roughly 55% HBM4 and 45% HBM3E, with HBM4 ramping from the third quarter of 2026. 12-high HBM4 enters mass supply early in the year, with 16-high parts targeted for the second half, so the crossover to a majority-HBM4 revenue mix lands in the back half of 2026.

HBM is the stacked memory that feeds an AI accelerator’s compute, and it is severely supply-constrained. Producing 1GB of HBM consumes roughly 4x the wafer capacity of standard DRAM, so AI memory is expected to absorb close to 20% of global DRAM wafer capacity in 2026. With only three suppliers capable of high-yield production, HBM gates how fast the whole industry can scale.

Primary sources

- SK hynix holds 62% of HBM, Micron overtakes Samsung, 2026 battle pivots to HBM4 — Astute Group

- Samsung, SK hynix Reportedly Plan ~20% HBM3E Price Hike for 2026 — TrendForce

- AI Reportedly to Consume 20% of Global DRAM Wafer Capacity in 2026 — TrendForce

- High Bandwidth Memory Market Size, Growth, Forecast and Industry Share — Mordor Intelligence

- HBM Memory Pricing and Specifications (2026) — Cost per Stack and per GB — Silicon Analysts

- SK hynix, Samsung, and Micron fighting for NVIDIA supply contracts for 16-Hi HBM4 orders — TweakTown

- SK Hynix, Micron Gain Share In HBM But Samsung Loses Ground — Semiecosystem

Last updated: June 1, 2026. Related: Capital.