Who’s raising, who’s consolidating, where the compute money went, and whether the bubble is real — the AI industry 2026, mapped, with every funding, M&A, and market-analysis deep dive.

The AI industry in 2026, mapped

The AI industry 2026 is moving faster than any single headline can capture: nine-figure rounds, sudden acquisitions, a compute build-out measured in hundreds of billions, and a running argument about whether any of it is sustainable. This hub is the map.

We group every funding analysis, M&A story, company timeline, and market thesis below so you can trace the money rather than chase the news. Follow the section that matters — who’s raising, who’s buying, where compute is going, or whether the whole thing is a bubble.

Funding, valuations & unicorns

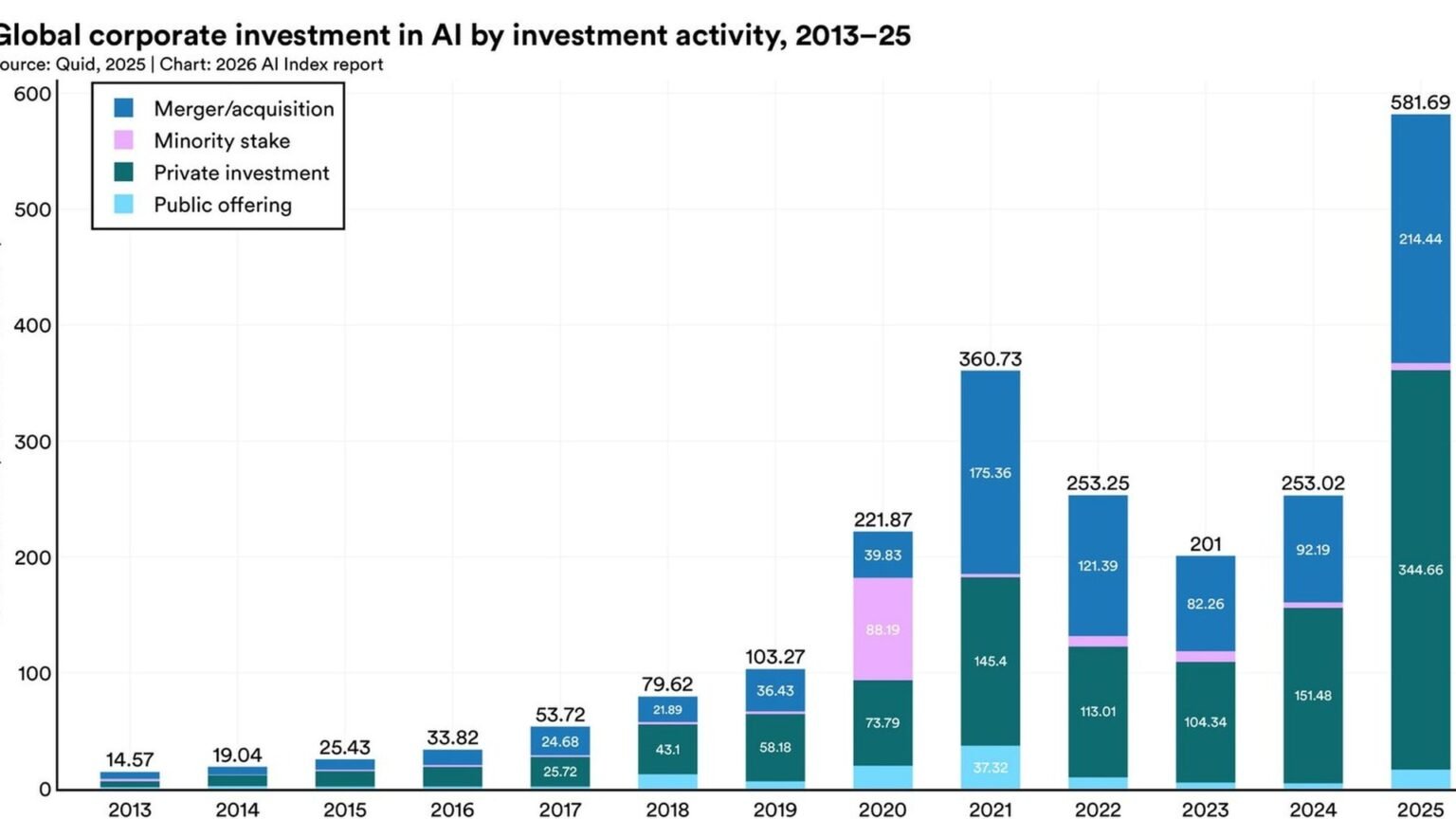

Where the money is going and at what price. The funding and valuation picture for the AI industry 2026.

M&A & consolidation

The wave of deals and the case that consolidation is inevitable.

Company timelines

How the key players got here, traced year by year.

Compute, infrastructure spend & hardware

The physical build-out underneath the AI industry 2026 — chips, data centers, and where the capex went.

| Guide | Format |

|---|---|

| Humanoid robots 2026 — Tesla, Figure, 1X enter real deployment | Guide |

| Stargate Compute Project: What’s Actually Being Built | Guide |

| Where $100B in AI Compute Went, 2024-2026 | Data |

Talent, salaries & layoffs

The labor market: who’s getting paid, who’s getting cut.

| Guide | Format |

|---|---|

| AI engineer salary 2026 — real frontier lab pay | Data |

| AI 2026 layoff split: 92K cut, labs hire | Guide |

Market analysis & theses

The bull and bear cases, regional landscapes, and the structural arguments shaping the AI industry 2026.

Builder’s take

As a founder building in this market (Cyntr, Loomfeed), I read the AI industry 2026 money flows less for the gossip and more for the signal: where capital concentrates is where the defensible moats and the brutal competition both end up.

- Follow compute spend, not press releases — capex commitments reveal real conviction better than valuations.

- Most of the nine-figure rounds are buying distribution and compute, not technology — read the funding analyses with that lens.

- Consolidation is the base case; build assuming your favorite tool may be acquired.

Frequently asked questions

Record funding concentrated in a few large labs, rapid M&A and consolidation, a hundreds-of-billions compute build-out, and an active debate over whether valuations are a bubble. The sections above map each thread to a deep dive.

It’s contested. The market-analysis section above lays out both the bull case (real revenue and compute demand) and the bear case (circular financing and stretched valuations).

Into data centers, chips, and multi-year capacity deals — see the compute and infrastructure-spend section for the breakdowns.

Primary sources

- Stanford HAI AI Index — economy chapter — Stanford HAI

- Crunchbase AI funding data — Crunchbase News

Last updated: May 30, 2026. Related: Capital.