Humanoid robots 2026 is no longer a speculative category pitch. Tesla says more than 1,000 Optimus Gen 3 robots are deployed across its factories, while Figure points to 11 months on BMW’s Spartanburg line and work tied to more than 30,000 vehicles. Together with 1X opening preorders for NEO ahead of first customer deliveries in 2026, the market has shifted from stage demos to early commercial deployment.

The market crossed from demo theater into factory operations

$20B

Tesla 2026 capex allocation

A significant portion is described as going to Optimus

1,000+

Optimus Gen 3 robots deployed

Reported across Tesla factories in January 2026

~$20K

Tesla target price per robot

Target pricing, not current public list price

1M/yr

Tesla late-2026 production target

Annualized target for Optimus output

The category changed in 2026

The clearest signal in humanoid robots 2026 is not a new render or keynote clip. It is time on task. Tesla’s Optimus program is being framed around internal factory deployment, with more than 1,000 Optimus Gen 3 robots reportedly deployed across Gigafactory Texas and Fremont as of January 2026, while Figure says its robot spent 11 months on BMW’s Spartanburg production line and contributed to work associated with more than 30,000 vehicles. Those are still early numbers by industrial automation standards, but they are materially different from the proof-of-concept era.

That shift matters because buyers now have three things they largely lacked a year ago: visible deployment references, early pricing anchors, and competing commercialization models. Tesla is talking about a roughly $20,000 target price and external sales in late 2026 or early 2027. Unitree has pushed a lower-cost reference point around its G1. Figure and 1X are leaning into platform narratives that tie robotics progress to AI software and model improvement. The result is that humanoid robots 2026 has become a capital formation story as much as a robotics story.

Enterprises can now evaluate humanoids against actual factory hours, not just conference demos.

“Tesla is building humanoid robots that can perform unsafe, repetitive or boring tasks.”

Tesla AI

| Company | Robot | 2026 signal | Commercial posture |

|---|---|---|---|

| Tesla | Optimus Gen 3 | 1,000+ deployed across Tesla factories | Internal deployment first, external sales targeted late 2026 or early 2027 |

| Figure | Figure 02 | 11 months at BMW Spartanburg; work tied to 30,000+ vehicles | Commercial pilots targeted in 2026 |

| 1X | NEO | Preorders open; first customer deliveries in 2026 | Early customer rollout |

| Unitree | G1 | Low-cost positioning | Commodity-style ecosystem play |

Tesla is trying to brute-force scale before the rest of the field

Tesla’s case in humanoid robots 2026 is straightforward: deploy internally, learn fast, then industrialize at automotive scale. The reported numbers are aggressive. Tesla is described as allocating $20 billion in 2026 capex, with a significant portion tied to Optimus, and targeting annual production of 1 million units by late 2026. A dedicated factory is reportedly under construction at Giga Texas with a target of 10 million units per year by 2027. If even part of that roadmap lands, Tesla will be attempting something no other humanoid company has publicly matched: mass manufacturing as the core product strategy.

The commercial logic is equally clear. Tesla’s target price of roughly $20,000 per robot puts Optimus in a range that large manufacturers and logistics operators can model against labor shortages, repetitive-task automation, and safety improvements. Tesla says initial external customers would be in manufacturing and logistics, with external sales expected in late 2026 or early 2027. That keeps the near-term story grounded in enterprise use cases rather than the consumer-home narrative that still dominates public imagination.

There is still a credibility gap between target and reality. Tesla has a long history of setting ambitious timelines, and the humanoid stack remains constrained by dexterity, safety, and autonomy. Yet the internal-factory-first approach gives Tesla a practical advantage: it can iterate on real workflows inside facilities it already controls. In humanoid robots 2026, that may be the single most important operational edge.

Tesla Optimus Gen 3 ⭐ Editor’s Pick

Best for: Large manufacturers and logistics operators watching for high-volume supply and lower target pricing

What works

Watch out for

Use internal factories as both customer and training ground, then sell into manufacturing and logistics.

How much of today’s factory work is truly autonomous?

Public humanoid demos still blur the line between autonomy, scripted behavior, and tele-operation assist. The safest reading for enterprise buyers is that many systems remain supervised, constrained to narrow tasks, or supported by remote intervention. That does not erase their value in controlled environments, but it does mean deployment claims should be read as workflow-specific rather than proof of general human-level autonomy.

Why does dexterity still limit broader deployment?

Walking, lifting, and basic pick-and-place have improved faster than fine manipulation. Industrial buyers care less about a robot dancing and more about whether it can handle irregular objects, recover from slips, and complete repetitive tasks without frequent resets. Human-skill dexterity remains out of reach for most commercial systems.

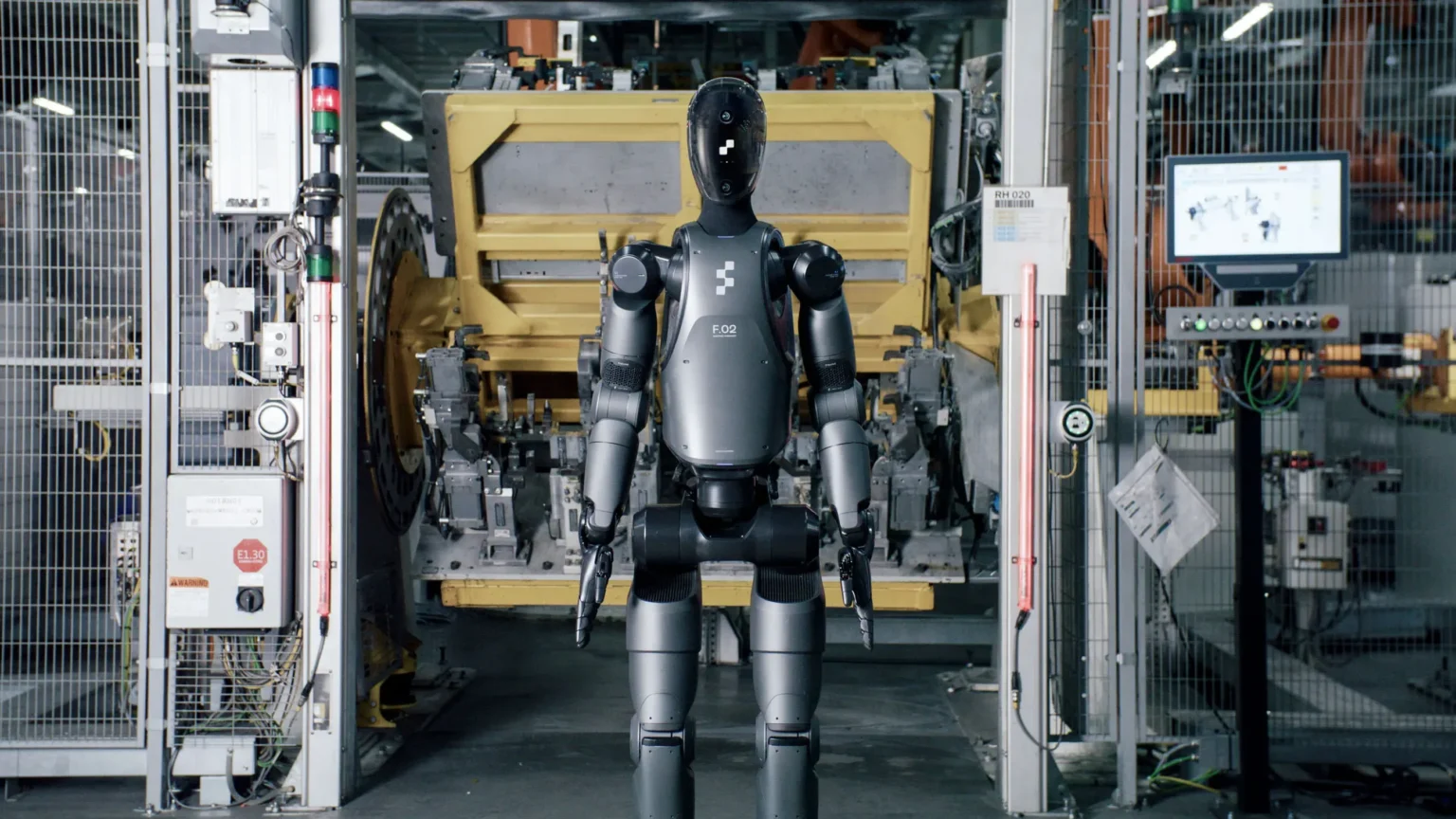

Figure has the strongest public manufacturing reference point outside Tesla

Figure’s position is different. It is not trying to out-manufacture Tesla overnight. It is trying to prove that an AI-first humanoid platform can earn its place on real production lines, then expand through partnerships and pilots. The company says it is backed by OpenAI, NVIDIA, Amazon, and Microsoft, and it has raised hundreds of millions. That cap table matters because Figure is selling more than a machine. It is selling the idea that software, model improvement, and integration velocity will define the winners in humanoid robots 2026.

The BMW deployment is the key data point. Figure says its robot spent 11 months on BMW’s Spartanburg production line and contributed to work associated with more than 30,000 vehicles. That does not mean Figure has solved general-purpose labor. It does mean the company can point to sustained time in a major automotive environment, which is more meaningful than a one-day pilot or a trade-show loop. Figure says Figure 02 is being designed as a general-purpose humanoid for warehouse and manufacturing work, with commercial pilots targeted in 2026.

For investors and buyers, Figure represents the strongest version of the AI-first platform thesis: use foundation-model progress, multimodal perception, and software iteration to improve robot usefulness faster than hardware cycles alone would allow. If Tesla is the vertically integrated benchmark, Figure is the best-known argument that partnerships and software leverage can still win share.

Figure 02

Best for: Manufacturers and warehouses evaluating pilot deployments with a software-led roadmap

What works

Watch out for

“Figure is building the first commercially viable autonomous humanoid robot.”

Figure

What should buyers ask about safety standards first?

Start with the operating envelope. Is the robot working in a caged, semi-structured, or shared human environment? Ask how emergency stops, speed limits, remote intervention, and incident logging are handled. Humanoid form factors create new expectations, but procurement still comes down to familiar industrial safety questions.

1X is the quiet contender pushing NEO toward first customer deliveries

1X does not yet have Tesla’s scale narrative or Figure’s public manufacturing reference, but it has something investors watch closely in emerging hardware markets: a concrete delivery story. The Norwegian company says preorders are open for NEO and that first customer deliveries are planned for 2026. In a market where many timelines still live in slides, that matters.

The broader significance for humanoid robots 2026 is competitive shape. 1X fits the AI-first platform pattern more than the vertically integrated one. The company is part of a cohort betting that software differentiation, embodied AI progress, and iterative deployment can create defensible value even if hardware supply chains become more standardized over time. That makes 1X strategically important beyond its current scale.

For now, the company remains earlier in commercialization than Tesla’s internal deployment push and Figure’s BMW case study. Still, preorders plus a 2026 delivery target put 1X in the conversation as the field moves from prototype fascination to customer qualification.

1X NEO

Best for: Early adopters tracking AI-first humanoid platforms and pilot opportunities

What works

Watch out for

The rest of the field shows how fragmented the market still is

The next tier of companies makes it clear that humanoid robots 2026 is not a winner-take-all market yet. Boston Dynamics remains a major reference point in robotics, though Atlas is still more research-focused while Spot has the clearer commercial footprint. Apptronik’s Apollo is in a pilot with Mercedes-Benz. Agility Robotics has pushed Digit into Amazon warehouse deployment. Sanctuary AI’s Phoenix keeps Canada in the conversation. Unitree’s G1 stands out for low-cost positioning, with pricing around $16,000 often cited as the clearest sign that a commodity-style humanoid market could emerge faster than many expected.

That diversity of approaches is healthy for buyers. It means the category is being tested across automotive, warehouse, logistics, and general industrial settings rather than converging too early on one architecture or one go-to-market model. It also means comparisons remain difficult. A robot designed for tightly scoped warehouse movement is not directly interchangeable with one marketed as a general-purpose factory worker.

Unitree G1

Best for: Developers and buyers watching low-cost humanoid economics

What works

Watch out for

Do not compare humanoids as if they are already standardized products. Most are still workflow-specific systems.

| Pattern | Companies | Core bet |

|---|---|---|

| Vertically integrated | Tesla, Boston Dynamics | Own hardware, software, and control stack |

| AI-first platform | Figure, Sanctuary AI, 1X | Differentiate through software, models, and partnerships |

| Low-cost commodity | Unitree and peers | Hit a price point and let the ecosystem build applications |

What 2026 unlocked, and what it still has not

Commercial deployment is real; general autonomy is not

The strongest conclusion from humanoid robots 2026 is that this is the first year of commercial-scale deployment, not the year of general robot labor. The unlocked pieces are concrete: real factory hours, named customers, visible target pricing, and enough competition for enterprise procurement teams to begin serious evaluation. Figure’s 11 months at BMW and Tesla’s internal factory deployment are the clearest proof that the category has crossed into operational use.

What remains unresolved is just as important. Consumer and home deployment are still out of reach because price remains high and safety is not solved for unstructured environments. Dexterous manipulation is still well below human skill in many practical settings. Outdoor and highly variable environments remain difficult. True autonomy is also not here in the broad sense implied by marketing; many systems still rely on tele-operated assist, supervision, or narrow-task constraints.

That leaves the market with a more sober but more investable thesis. Humanoids do not need to replace people everywhere to become a real category. They need to work reliably in enough repetitive, labor-constrained, and safety-sensitive workflows that buyers can justify deployment. On that narrower test, 2026 looks like a genuine turning point.

Pros

Cons

Why are home humanoids still not a 2026 market?

Homes are harder than factories. Layouts vary, objects are irregular, safety expectations are higher, and the economics are far less forgiving. A robot that can justify itself in a logistics workflow may still be far too expensive and unreliable for household use.

Frequently asked questions

Because the category now has visible deployment evidence rather than only demos. Tesla’s Optimus page, Figure’s official site, and 1X’s company site all point to active commercialization efforts, while the reported Tesla and BMW-related milestones give buyers concrete reference points.

No broad consumer rollout is established in the cited material. Tesla’s AI page frames Optimus around industrial work, and the reported external customer focus is manufacturing and logistics. Figure and 1X are also centered on commercial deployment and early customer programs rather than mass home use.

Primary sources

- Tesla AI — Tesla

- Figure official site — Figure

- 1X Technologies official site — 1X Technologies

- Tesla Optimus Gen 3 production and deployment report — Programming Helper

- Top tech news on Tesla Optimus factory deployment — Top Tech News

- GrabaRobot on humanoid workforce deployment — GrabaRobot

- Top 8 humanoid robot companies 2026 — EVSINT

Last updated: May 26, 2026. Related: Capital.