I think the AI bubble thesis is both too cynical and not cynical enough. Too cynical because it often ignores the fact that this market already has real revenue, real enterprise buyers, and real developer usage. Not cynical enough because it sometimes underestimates how much capital has been committed before the long-term unit economics are settled. The honest read, in my view, is that AI can be a bubble in capital formation and a genuine platform shift in software at the same time. That is the frame I use here, with an eye on what is actually verifiable today and where the analogy to 2000 still holds. For related market maps, see our AI agent unicorn tracker and our Anthropic vs. OpenAI analysis.

My view: this is a real boom, and parts of it will still break

$20.0B

Microsoft FY25 Q1 capex incl. finance leases

Source: Microsoft earnings

$13.1B

Alphabet Q3 2024 capex

Source: Alphabet earnings

$64B–$72B

Meta 2025 capex outlook

Source: Meta Q1 2025 results

Verdict: bubble in financing, not necessarily in usage

I do not buy the lazy version of the AI bubble argument. I do buy the harder version. The lazy version says AI is mostly hype, with little underlying demand, and that today’s spending resembles a pure speculative mania detached from business reality. I think that is already contradicted by the evidence. The harder version says demand is real but capital deployment may still be ahead of durable returns. That is much more plausible.

Start with the scale of the buildout. Microsoft said in its fiscal 2025 first-quarter earnings materials that capital expenditures, including finance leases, were $20.0 billion for the quarter, up 5% sequentially and 50% year over year, with cloud and AI-related spending a major driver. Alphabet said in its Q3 2024 earnings release that capital expenditures were $13.1 billion in the quarter, reflecting investment in technical infrastructure, especially servers and data centers. Meta said in its Q1 2025 results that it increased its 2025 capital expenditure outlook to $64 billion to $72 billion, citing support for AI efforts and data center investments. Amazon said in its Q1 2025 earnings release that capital investments were focused on supporting demand for generative AI and technology infrastructure. Oracle has also repeatedly tied data center expansion to AI demand in its earnings communications, including its fiscal 2025 third-quarter results.

Add those signals together and the bear case writes itself: hundreds of billions of dollars are being committed across 2024 and 2025 before anyone can say with confidence what steady-state margins look like for foundation models, inference-heavy applications, or agentic workflows. If utilization disappoints, if open-weight models compress pricing faster than expected, or if enterprises settle into narrower use cases than the market is underwriting, some of this infrastructure will be remembered the way excess fiber was remembered after the dot-com era.

That is the part the bubble camp gets right. Capacity can outrun demand. Capital cycles can overshoot. Infrastructure investors can confuse strategic necessity with economic discipline.

Pros

Cons

⚠️ The bear case in one line. Even if AI is transformative, too much infrastructure can still be built too early and at the wrong expected margin.

“The strongest AI bubble argument is not that demand is fake. It is that capital has moved faster than proven long-term economics.”

alatirok analysis

| Company | What it disclosed | Why bears care |

|---|---|---|

| Microsoft | $20.0B capex incl. finance leases in FY25 Q1 | Large AI/cloud buildout raises the bar for utilization and returns |

| Alphabet | $13.1B capex in Q3 2024 | Server and data center spending assumes sustained AI demand |

| Meta | $64B–$72B 2025 capex outlook | Aggressive AI investment increases execution risk if monetization lags |

| Amazon | Capex tied to generative AI and infrastructure demand | AWS AI demand must remain strong to justify pace of expansion |

Where I think the AI bubble argument goes wrong

$10B+

OpenAI ARR run rate

Source: OpenAI, June 2025

$3B

Anthropic annualized revenue

Source: Anthropic, May 2025

The mistake is collapsing every layer of the stack into one trade. Data centers, GPUs, foundation models, copilots, vertical AI apps, and agent tooling do not share the same economics or the same risk profile. Saying “AI is a bubble” is analytically weak in the same way saying “the internet was a bubble” was weak. Some internet companies were nonsense. The internet itself was not. Some AI companies will be nonsense. The software shift is still real.

The cleanest rebuttal to the broad-brush bubble claim is revenue. OpenAI said in June 2025 that it had surpassed $10 billion in annual recurring revenue run rate. Anthropic said in May 2025 that its annualized revenue reached $3 billion. Those are not tiny experimental numbers. They do not prove these businesses are efficiently profitable, and they do not settle valuation debates. They do prove that the market is not built on demos alone.

There is also a distribution point that many bubble arguments miss. This cycle is not waiting for entirely new consumer behavior to emerge from scratch. Microsoft has integrated Copilot across Microsoft 365, GitHub, Azure, and security products. Google has embedded Gemini across Workspace, Cloud, Search, and Android-facing surfaces. Amazon has pushed generative AI through AWS, including Amazon Bedrock and Amazon Q. That matters because enterprise adoption often follows procurement gravity, identity systems, and existing contracts more than raw model quality.

The other thing that is different from 2000 is that AI can be sold as an efficiency layer inside existing budgets. A company does not need to invent a new category of online commerce to justify an AI coding assistant, support automation workflow, or document analysis pipeline. It can reallocate spend from contractors, BPO, search, analytics, or internal tooling. That does not make every ROI claim true. It does make the path to monetization shorter than many critics admit.

📌 What is actually new. This cycle has real recurring software revenue and enterprise distribution through incumbent platforms, not just speculative future traffic.

“The right comparison is not ‘bubble or no bubble.’ It is ‘which layers have durable cash flow, and which layers are being financed on hope?'”

alatirok analysis

| Signal | What it suggests | Why it matters |

|---|---|---|

| OpenAI >$10B ARR run rate | Large-scale paid demand already exists | Weakens the claim that AI revenue is mostly hypothetical |

| Anthropic $3B annualized revenue | A second major model vendor has material revenue | Suggests demand is not concentrated in a single outlier |

| Microsoft/Google/Amazon distribution | AI is being sold through existing enterprise channels | Reduces go-to-market friction versus prior platform shifts |

The dot-com and fiber analogy is useful, but only if you use it carefully

Runner-up framing: AI may rhyme with fiber, not Pets.com

I think the fiber analogy is the best version of the bear case. In the late 1990s and early 2000s, too much telecom infrastructure was financed ahead of realized demand. That overbuild destroyed capital even though long-run internet demand turned out to be enormous. The lesson was not that bandwidth was fake. The lesson was that timing, financing structure, and competitive intensity mattered.

That is why I am skeptical whenever someone uses the dot-com comparison as a total dismissal of AI. The historical lesson cuts both ways. Overinvestment can be real, and the platform shift can still be real. In fact, those two things often coexist. Investors can lose money in a market that changes everything. Builders can create enduring products while a lot of adjacent capital gets burned.

The AI version of the fiber risk is straightforward. If model training and inference costs do not keep falling fast enough, if enterprise usage stays bursty rather than persistent, or if open models push proprietary pricing down faster than expected, then a chunk of the current GPU and data center footprint will earn lower returns than the market expects. NVIDIA itself has acknowledged in its filings that demand can be volatile and that customers may adjust purchasing patterns; see the company’s SEC filings for risk factors tied to concentration and demand shifts.

Still, the analogy breaks when it is used to imply that all current AI revenue is merely future hope. It is not. The software layer is already monetizing. The better question is whether software gross margins and workflow depth will rise quickly enough to absorb the infrastructure bill.

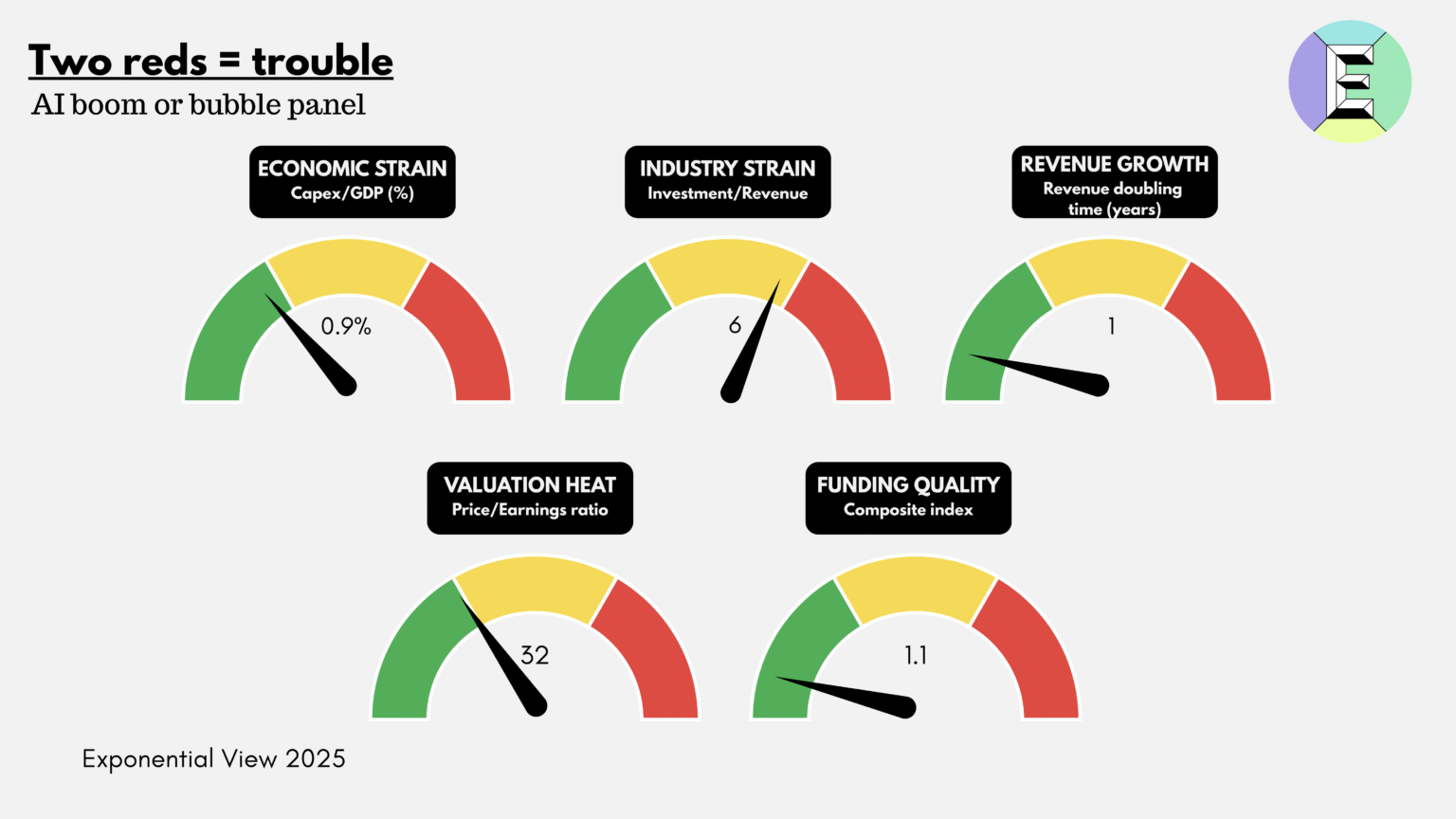

What I watch to separate a healthy boom from a dangerous bubble

I look at four things. First, revenue quality. Not just top-line growth, but whether revenue is recurring, contract-backed, and attached to workflows that are hard to rip out. A coding assistant used every day by a development team is different from a novelty image app. A customer support automation layer tied into CRM and ticketing is different from a one-off pilot.

Second, inference economics. Training gets the headlines, but inference is where many businesses live or die. If serving costs remain too high relative to what customers are willing to pay, then application margins get squeezed and model vendors face pricing pressure. This is one reason model optimization, smaller task-specific models, caching, routing, and retrieval matter so much. The future of AI economics is not just bigger models; it is cheaper useful work.

Third, distribution. I pay close attention to whether AI products are winning because they are genuinely embedded in enterprise systems or because they are being sampled by innovation budgets. Microsoft, Google, and Amazon have an advantage here because they can bundle AI into environments where identity, security, billing, and data access already exist. That can create real pull-through for the model layer and for downstream agent products.

Fourth, retention of human trust. This sounds soft, but it is not. Agentic systems only become durable budget lines when users trust them with consequential work. That means reliability, observability, auditability, and governance. It is one reason the most interesting parts of the stack are not just frontier models but also evaluation, tracing, policy, and orchestration infrastructure. If you want a sense of where capital has been flowing in that layer, our AI agent unicorn roundup is a useful companion read.

📌 My practical test. If an AI product is tied to recurring workflow value, improving unit economics, and incumbent distribution, I treat it as a business. If not, I treat it as a financing story.

{

"ai_boom_health_check": {

"revenue_quality": "recurring and workflow-embedded",

"unit_economics": "inference costs falling",

"distribution": "incumbent channels or strong direct pull",

"trust": "observable, auditable, reliable"

}

}| Metric I watch | Healthy signal | Bubble signal |

|---|---|---|

| Revenue quality | Recurring, workflow-embedded, contract-backed | Pilot-heavy, discretionary, easy to cut |

| Inference economics | Costs falling faster than price compression | Margins squeezed by compute and competition |

| Distribution | Adoption through existing enterprise systems | Usage depends on temporary experimentation budgets |

| Trust and governance | Observable, auditable, reliable systems | High error rates and weak controls block expansion |

My bottom line on the AI bubble

Best summary: real market, overheated capital cycle

Here is my honest take. I think the AI bubble argument is right that too much money can chase a real technological shift. It is wrong when it implies that current AI demand is mostly fictional. We already have enough evidence of real software revenue, enterprise adoption, and productivity use cases to reject the idea that this is all narrative and no business.

What I expect instead is a sorting event. Some infrastructure bets will prove early or overpriced. Some model vendors will discover that revenue scale does not automatically translate into attractive margins. Some application companies will be crushed by distribution they do not control. At the same time, a smaller set of companies will become foundational because they own workflow, distribution, or data advantages that compound over time. Data network effects may not look like consumer social graphs, but they still matter when products improve through usage, feedback, and integration depth.

If you want a concrete example of how this sorting is already happening, compare the strategic positions of the leading model vendors. We broke that out in our Anthropic vs. OpenAI piece. The point is not that one company wins everything. The point is that this market is already stratifying by buyer, channel, and product architecture.

So yes, there is bubble behavior in AI. There is also real business formation in AI. Those statements are not contradictory. They are probably the most accurate way to describe the market right now.

I could be wrong. This take fails if enterprise AI budgets prove mostly experimental and get cut sharply, if model pricing collapses faster than costs, if inference demand never becomes dense enough to support the current infrastructure base, or if the largest reported revenue numbers turn out to be less durable than they appear. It also fails if productivity gains remain too narrow to justify broad seat expansion. If those conditions show up together, the bears will have been early, not wrong.

⚠️ Conditions that would invalidate my view. A sharp pullback in enterprise renewals, sustained margin compression, and underutilized infrastructure would turn a healthy boom into a more classic bubble unwind.

“Bubble behavior and genuine platform change can happen in the same market at the same time.”

alatirok analysis

Frequently asked questions

No. The strongest version of the argument is that infrastructure spending may be running ahead of proven long-term returns. Microsoft, Alphabet, and Meta have all disclosed large AI-related capital spending in earnings materials, which is why overbuild risk is a serious question. See Microsoft FY25 Q1 earnings, Alphabet Q3 2024 earnings, and Meta Q1 2025 results.

Reported revenue is the clearest evidence. OpenAI said it surpassed $10 billion in annual recurring revenue run rate, and Anthropic said its annualized revenue reached $3 billion. Those figures do not settle valuation debates, but they do show that AI revenue is not purely hypothetical.

One major difference is that AI is already being sold into existing enterprise software budgets through large distribution channels. Microsoft, Google, and Amazon are embedding AI into products enterprises already buy, which shortens the path from experimentation to procurement. You can see that in product and platform materials from Microsoft Copilot, Google Workspace with Gemini, and Amazon Bedrock.

I would worry more if enterprise renewals weaken, if inference costs stay stubbornly high, and if data center capacity is built faster than durable usage arrives. Those are the conditions under which a real technology shift can still produce poor returns for investors. NVIDIA’s public filings discuss demand concentration and purchasing-pattern risks in more detail at its SEC filings page.

Primary sources

- OpenAI company update — OpenAI

- Anthropic annualized revenue reached $3 billion — Anthropic

- Microsoft FY25 Q1 earnings release and webcast — Microsoft

- Alphabet Q3 2024 earnings release — Alphabet

- Meta Q1 2025 results — Meta

- Amazon Q1 2025 earnings results — Amazon

- Oracle fiscal 2025 third-quarter financial results — Oracle

- NVIDIA SEC filings — NVIDIA

- Microsoft Copilot — Microsoft

- Google Workspace with Gemini — Google

- Amazon Bedrock — Amazon Web Services

Last updated: May 20, 2026. Related: Agent Infrastructure.