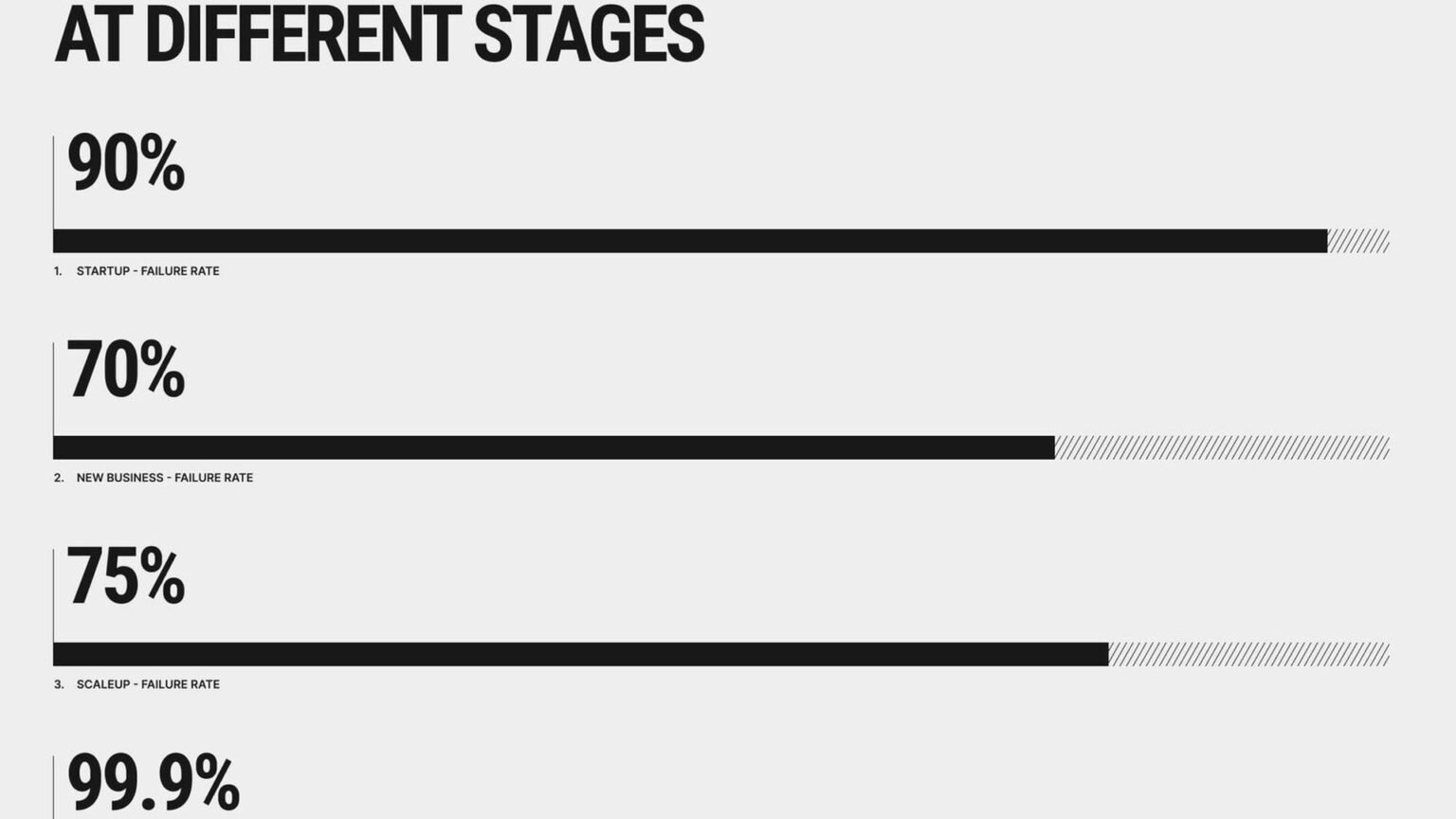

One number frames the debate: Y Combinator said 70% of its Winter 2026 batch was building AI agents. I think that is not a sign the market needs even more startups; it is evidence that the AI startup count has already overshot demand in several categories. In my view, too much venture money, too many lookalike products, and too little real distribution are producing a crowded field that will end in consolidation, acqui-hires, and shutdowns rather than a broad flowering of durable companies.

My contrarian view: the market needs fewer AI startups

70%

of YC Winter 2026 startups building AI agents

Per Y Combinator’s batch announcement

I think the AI startup count is already too high. Not because entrepreneurship is bad, and not because AI is overhyped in the abstract, but because too many new companies are being formed around the same narrow set of primitives: model access, prompt orchestration, browser automation, support agents, SDR agents, meeting agents, and coding agents with only marginal differentiation.

That is not what a healthy software market looks like. A healthy market can support many experiments, but it still imposes discipline through distribution, switching costs, integration depth, and customer willingness to pay. In AI, especially in agent infrastructure and application layers, venture capital has often arrived faster than those constraints. The result is a startup formation boom that looks vibrant from the outside and increasingly redundant from the inside.

I am not arguing for less innovation. I am arguing that the current startup supply is out of proportion to the number of categories that can realistically support independent winners. If ten teams are building a durable new market, that is healthy. If a hundred teams are building slightly different wrappers on the same APIs while hoping distribution will sort itself out later, that is mostly waste.

That is why I read the current moment less as a golden age of company creation and more as a sorting event that has not happened yet. Readers who follow our coverage of category concentration will recognize the pattern from our look at every $1B+ AI agent unicorn in 2026: value is already clustering around a relatively small set of companies with strong distribution, product velocity, or capital access.

More AI startups does not automatically mean more innovation. In several agent categories, it may mean more duplication, weaker talent density, and a longer path to real customer value.

“The problem in AI is no longer a shortage of people willing to start companies. It is a shortage of categories that can support all of them.”

alatirok analysis

YC’s Winter 2026 batch is a signal, not just a curiosity

The cleanest public signal of startup oversupply came from Y Combinator itself. In its Winter 2026 batch announcement, YC said 70% of the batch was building AI agents. That is a remarkable statistic, and I do not read it as proof that the market can absorb endless new entrants. I read it as proof that the startup formation machine has become highly concentrated around one fashionable thesis.

YC is not the whole market, but it is one of the best windows into what ambitious founders think investors and customers want right now. When a supermajority of a major accelerator batch converges on the same broad category, the likely outcomes are not all positive. Some of those teams will be excellent. Many will be competing for the same buyers, the same integrations, the same model providers, and the same wedge into enterprise workflows.

This matters because startup ecosystems often confuse ease of formation with quality of opportunity. It has never been easier to stand up a demo, connect to frontier models, and claim agentic automation. That lowers the cost of experimentation, which is good. It also lowers the barrier to launching products that look differentiated in a demo but collapse into sameness under procurement scrutiny.

We have seen versions of this before in cloud, crypto, and no-code. The difference with AI agents is that the underlying capability stack is moving so fast that many product claims decay quickly. A feature that looks novel in January can be table stakes by June. In that environment, a surge in startup count can be a sign of weak moats rather than strong demand.

Y Combinator wrote that 70% of its Winter 2026 batch was building AI agents. That is a useful market signal because YC sits near the top of the founder funnel.

Capital is outrunning revenue in too many cases

The strongest argument for fewer startups is not aesthetic. It is financial. In too many AI categories, capital raised has become detached from demonstrated revenue durability. That does not mean every well-funded company is weak. It means the market has normalized a capital-to-traction ratio that would look aggressive in most other software cycles.

Take the public reporting around some of the best-known AI coding and agent companies. These are among the category leaders, not fringe examples. Yet even there, the numbers suggest a market willing to price future dominance long before current economics would justify it by traditional software standards. That is a sign of investor belief in winner-take-most outcomes. It is also a sign that many subscale competitors are unlikely to survive independently if those winner-take-most dynamics are real.

When investors fund dozens of adjacent companies on the assumption that one or two will become category kings, the ecosystem gets more startups on paper but not necessarily more enduring businesses. Founders hire ahead of revenue, customers get inundated with similar pitches, and the eventual correction comes through down rounds, acqui-hires, or strategic sales.

I do not think this is a moral failure. It is a market structure problem. If distribution and trust end up concentrating in a handful of brands, then financing a very large number of near-identical challengers is not ecosystem building. It is overproduction.

Pros

Cons

| Company | Publicly reported signal | Why it matters for startup count |

|---|---|---|

| Cursor / Anysphere | Bloomberg reported Anysphere was in talks to raise at about a $9 billion valuation in 2025 | Suggests investors expect outsized category concentration around a few coding winners |

| Windsurf / Codeium | CNBC reported OpenAI agreed to acquire Windsurf for about $3 billion in 2025 | Shows strategic buyers may prefer buying scaled contenders rather than letting the field stay fragmented |

| Cognition | Cognition announced it signed a definitive agreement to acquire Windsurf in 2026 | Points to consolidation pressure inside AI coding and agent markets |

Distribution still beats demos

One reason I am skeptical of a high AI startup count is simple: distribution remains brutally concentrated. The best demo rarely wins. The company that already sits inside the workflow, owns the developer surface, controls the customer relationship, or can bundle AI into a broader platform usually has the advantage.

That is especially true in enterprise software. Buyers do not want twenty agent vendors for adjacent tasks. They want fewer vendors, stronger security reviews, clearer accountability, and products that fit existing systems. In practice, that favors incumbents and a small number of breakout startups with unusually strong product velocity or brand pull.

This is why so many AI startups end up sounding more differentiated to investors than to customers. A founder can explain nuanced architectural differences between orchestration layers, memory systems, or evaluation loops. A buyer often hears a simpler question: why should I add another vendor when my existing platform is shipping similar capabilities?

The distribution problem is even sharper in coding, support, and productivity tools, where users already live inside entrenched environments. We have covered that dynamic in our analysis of why most AI agent startups may consolidate by 2028. The short version is that a crowded field does not produce a broad middle class of winners when channels are narrow and switching costs are low.

“In software, distribution is a moat. In AI, it is often the moat.”

alatirok analysis

Talent dilution is a real cost, not a side effect

The most underrated downside of too many AI startups is talent dilution. When hundreds of companies are funded around similar theses, the ecosystem does not magically get hundreds of elite teams. It gets the same finite pool of strong researchers, product builders, infrastructure engineers, and go-to-market operators spread across too many organizations.

That matters because AI products are unusually cross-functional. The best companies need people who understand models, systems, evaluation, UX, enterprise deployment, and pricing. Those teams are hard to assemble even in a concentrated market. In an oversupplied one, many startups end up with one or two excellent people and a long tail of gaps they cannot fill.

The category-level effect is lower quality. Products ship with weak reliability, shallow integrations, poor eval discipline, and vague positioning. Customers then conclude that ‘AI agents’ as a whole are immature, when the deeper issue is that too many underpowered teams are trying to occupy the same market at once.

I would rather see fewer startups with denser talent and more staying power than a larger number of companies that each have just enough capability to raise a seed round and launch a polished landing page. The former builds trust in the category. The latter burns it.

A smaller number of stronger teams can be better for customers, hiring markets, and long-term category credibility than a larger number of thinly staffed startups.

Agent startups are converging on the same product shapes

Another reason the AI startup count looks too high to me is product convergence. Browse enough launch posts and you start seeing the same templates repeated: an AI teammate for sales, an AI employee for support, an AI engineer for code, an AI analyst for operations, an AI browser worker for repetitive tasks. The labels change. The underlying promise often does not.

That convergence is not accidental. Frontier models are broadly accessible through major providers. Open-source models continue to improve. Tooling for retrieval, orchestration, evals, and browser or desktop automation is more available than ever. Those are good developments for builders. They also compress the space for true product differentiation at the application layer.

When the underlying ingredients are widely available, many startups end up competing on packaging, speed, and storytelling. Some will still build real moats through workflow depth, proprietary data loops, or exceptional UX. But many others are effectively racing to become the best-known version of a product that several rivals can reproduce.

This is one reason I keep returning to concentration. If the market is converging on a handful of product shapes, then it is unlikely to support a huge number of independent winners in each shape. We are already seeing this in coding, where our broader coverage of model competition for agents and agent frameworks suggests the underlying stack is maturing faster than many application moats.

Pros

Cons

Consolidation is no longer hypothetical

My verdict: startup formation is ahead of market capacity

The case for fewer startups gets stronger once consolidation begins in earnest. We are now past the stage where consolidation was just a theoretical endgame. Public reporting and company announcements show that strategic combinations are already part of the market structure.

One of the clearest examples is Windsurf. CNBC reported in 2025 that OpenAI agreed to acquire Windsurf for about $3 billion. In 2026, Cognition announced it had signed a definitive agreement to acquire Windsurf. Whatever the final long-term ownership map looks like, the broader point stands: scaled players and strategic buyers are moving to compress the field, not preserve maximum fragmentation.

That pattern is rational. If a category is crowded, the fastest way to gain customers, talent, and product assets is often to buy rather than outbuild. For founders, that can be a good outcome. For the ecosystem, it is evidence that startup count was not the right north star. The market is selecting for concentration.

I expect more of this, especially in coding, customer support, workflow automation, and vertical agents where distribution overlap is high. If that happens, the current startup glut will look less like a broad renaissance and more like a temporary inventory build before roll-ups and shutdowns clear the market.

The strongest counterargument: experimentation needs abundance

There is a serious counterargument, and I want to take it seriously. Many important technology waves looked crowded before they clarified. Search, social, cloud, mobile, and SaaS all produced lots of startups, many of which failed. That was not necessarily waste. It was the cost of discovering what users actually wanted.

The same may be true in AI. We do not yet know the final product boundaries for agents, copilots, autonomous workflows, or model-native software. A market with many startups can generate more experiments, more founder learning, and more unexpected category creation than a tightly filtered one.

I agree with that up to a point. The issue is not whether experimentation is good. It is whether the current level of company formation is still increasing useful experimentation or merely increasing duplication. Once too many teams are pursuing nearly identical wedges, the marginal startup adds less discovery and more noise.

This is where I part ways with the ‘let a thousand flowers bloom’ view. In 2026, I think we are well past the stage where every additional AI agent startup meaningfully expands the frontier. Many are now competing over known use cases with known buyer objections and known distribution bottlenecks.

“Experimentation is valuable. Duplication financed at scale is something else.”

alatirok analysis

What a healthier market would look like

If I am right, the answer is not to discourage founders from building in AI. It is to raise the bar for what deserves to be a standalone company. A healthier market would have fewer startups chasing horizontal sameness and more teams going after hard, workflow-deep, data-rich problems where incumbents are genuinely weak.

That means more skepticism toward products whose main advantage is wrapping a frontier model with a cleaner interface. It means more attention to retention, integration depth, security posture, and measurable labor substitution or revenue lift. It means fewer seed rounds for generic agent claims and more support for companies that can show why their wedge compounds over time.

It also means founders should think harder about whether they are building a company, a feature, or an acquisition target. There is nothing wrong with building for acquisition if everyone is honest about it. But the ecosystem should stop pretending that every polished AI launch is on a path to becoming an enduring independent business.

We have made related arguments in our coverage of AI agent pricing models and enterprise AI agent security requirements. The throughline is that durable companies are usually built where deployment friction is high, customer trust matters, and product depth compounds. Those conditions naturally support fewer winners.

The best candidates for new AI startups are categories with proprietary data loops, difficult integrations, regulatory complexity, or workflow depth that incumbents cannot easily copy.

What this means for founders and investors

For founders, my advice is blunt: assume your category is more crowded than it looks from inside your own bubble. If your pitch can be paraphrased as ‘an AI agent for X,’ you probably do not yet have enough differentiation. You need a stronger answer on why customers will switch, why incumbents cannot absorb the feature, and why your product gets better with usage in a way rivals cannot easily match.

For investors, the implication is equally uncomfortable. Counting startups is not the same as building an ecosystem. If capital keeps flowing into lookalike teams because AI remains the dominant narrative, the likely outcome is not a richer market but a noisier one. More companies will be funded than can plausibly survive, and the eventual correction will be framed as an AI disappointment when it is really a market selection event.

I also think seed and Series A investors should be more explicit about category capacity. How many independent winners can this market support? What distribution channels are actually open? What evidence suggests this team is not just one of many competent wrappers around the same model capabilities? Those questions matter more in AI than in many prior software cycles because the underlying technology layer is so rapidly shared across competitors.

None of this means founders should stop building. It means they should be more selective about where they build, and investors should be more selective about what kind of startup formation they reward.

Pros

Cons

{

"bad_thesis": "AI agent for a common workflow with no proprietary advantage",

"better_thesis": "AI product with workflow lock-in, differentiated data, and measurable ROI",

"investor_question": "How many durable independent winners can this category realistically support?"

}Where my argument breaks

Bottom line: fewer, stronger startups would be better

I could be wrong. The cleanest way my argument fails is if AI opens far more durable software categories than I expect. If agents become foundational across every major workflow and each workflow supports multiple independent platforms with real moats, then today’s high AI startup count may look not excessive but necessary.

I could also be wrong if distribution becomes less concentrated than prior software waves. If open ecosystems, model marketplaces, and agent interoperability make it easier for smaller companies to reach users without being crushed by incumbents, then a larger long tail of viable startups could emerge.

Another failure case is technical. If the next wave of model and tool improvements dramatically expands what specialized products can do, then what looks like duplication today may turn into segmentation tomorrow. In that world, many apparently similar startups could diverge into distinct, defensible businesses.

Still, from where I sit in 2026, the evidence points the other way: too much capital, too many lookalike agent companies, too little distribution, and the early signs of consolidation already underway. That is why I think the market would be healthier with fewer AI startups, not more. I could be wrong.

This argument fails if AI creates many more durable categories than expected, if distribution opens up materially for smaller vendors, or if technical progress sharply increases differentiation at the application layer.

Frequently asked questions

Because Y Combinator is one of the clearest public windows into founder formation trends. In its Winter 2026 batch announcement, YC said 70% of the batch was building AI agents, which makes it a useful signal of how concentrated startup creation has become.

Yes. Public reporting and company announcements point in that direction. CNBC reported that OpenAI agreed to buy Windsurf for about $3 billion, and Cognition later announced it had signed a definitive agreement to acquire Windsurf on its official blog at cognition.ai/blog.

No. It means being skeptical that every AI product idea deserves to become a standalone venture-backed company. You can be bullish on AI adoption while still believing that distribution, integration depth, and customer trust will concentrate value in a smaller set of winners. For a related market map, see our internal analysis at every $1B+ AI agent unicorn in 2026.

This take would weaken if AI creates many more durable categories than expected, if smaller vendors gain easier access to users through open ecosystems, or if application-layer differentiation becomes much stronger. Those are all plausible scenarios, which is why the conclusion should be read as an argument about current market structure, not a permanent law.

Primary sources

- Y Combinator Winter 2026 batch announcement — Y Combinator

- Y Combinator companies directory — Y Combinator

- CNBC report on OpenAI and Windsurf — CNBC

- Bloomberg report on Anysphere valuation talks — Bloomberg

- Cognition blog — Cognition

- Cursor homepage — Cursor

- Windsurf homepage — Windsurf

Last updated: May 21, 2026. Related: Agent Infrastructure.