CoreWeave, Nebius and Crusoe are scaling AI compute on borrowed money and contracted backlog. The unit economics hinge on one bet: that GPUs outlast their debt.

What neocloud economics 2026 actually mean

Neocloud economics 2026 comes down to a single timing bet: that a GPU can earn back its cost, service the debt that bought it, and still throw off profit before it has to be replaced. A neocloud is a specialized cloud operator that does one thing — rent out racks of NVIDIA accelerators for AI training and inference — without the diversified software empire of an Amazon or Microsoft. CoreWeave, Nebius and Crusoe are the three names that define the category, and all three are growing revenue at triple-digit rates while financing that growth with extraordinary amounts of borrowed money.

The business looks simple from the outside. You buy GPUs, you wrap them in power and cooling, and you sign multi-year contracts with AI labs and hyperscalers who cannot get enough compute. The complication is that the asset depreciates fast, the debt comes due on a fixed schedule, and the contracts — however enormous — only pay out if the counterparty survives and keeps consuming. The entire model is a race between cash generation and obsolescence.

This article treats the three operators as businesses rather than stock tickers. We walk through revenue, contracted backlog, debt structure, depreciation policy and the payback math, then ask the only question that matters: does the cash a GPU produces arrive before the bill for replacing it does? The numbers below are drawn from Q1 2026 filings and disclosures reported through May 2026.

Revenue and backlog: the headline numbers

$2.08B

CoreWeave Q1 2026 revenue

Up 112% year over year

$99.4B

CoreWeave revenue backlog

36% expected to convert within 24 months

684%

Nebius Q1 2026 revenue growth

To $399M, off a small base

$7-9B

Nebius 2026 ARR guidance

Raised on Meta + Microsoft deals

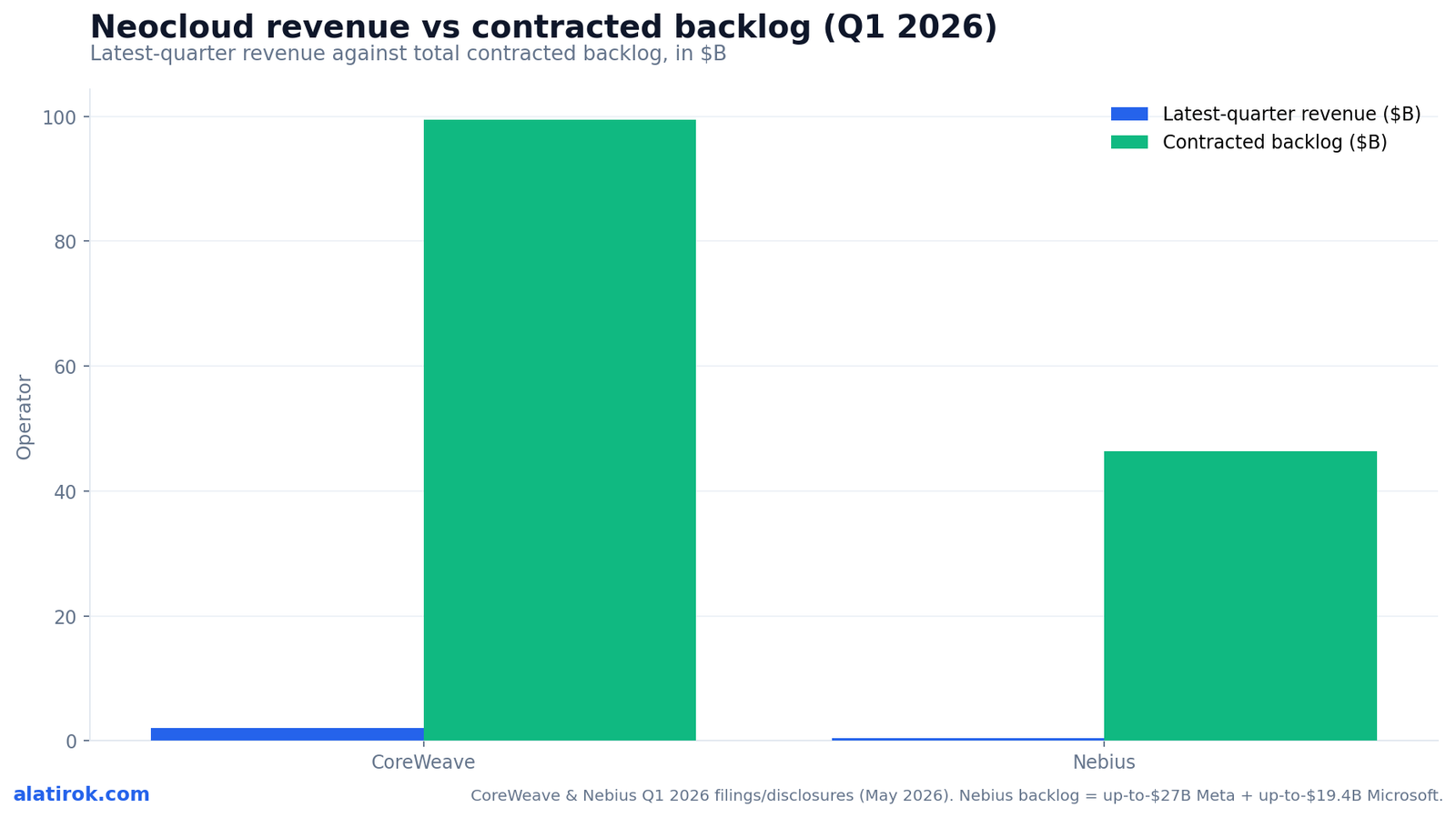

CoreWeave is roughly ten times Nebius’s size by revenue, but Nebius is growing faster and has assembled a backlog that, deal-for-deal, rivals CoreWeave’s. In Q1 2026, CoreWeave reported $2.078 billion of revenue, up 112% year over year, and ended the quarter with a $99.4 billion revenue backlog against about 3.5 gigawatts of contracted power. Nebius reported $399 million of Q1 2026 revenue — a startling 684% year-over-year jump — and raised its 2026 guidance to $3.0-3.4 billion in revenue and $7-9 billion in annualized recurring revenue (ARR).

The backlog is the seductive number, and it deserves scrutiny. CoreWeave’s $99.4 billion is near-term weighted: management says 36% is expected to convert within 24 months and 75% within four years. Nebius’s backlog is concentrated in two megadeals — a Meta contract worth up to $27 billion ($12 billion of fixed dedicated compute plus a $15 billion option at Nebius’s discretion) and a Microsoft commitment of up to roughly $19.4 billion over five years. For a company that did $529.8 million of revenue in all of 2025, those are transformational contracts.

Backlog is not cash, and it is not even guaranteed revenue. It is the sum of contracted future payments, sensitive to counterparty health and to whatever termination and option clauses the contracts carry. A $15 billion option that one side can decline is worth less than $15 billion of firm commitment. The right way to read these figures is as a measure of demand and bargaining position, then to discount heavily for concentration: a handful of AI labs and hyperscalers sit behind almost all of it.

The debt engine: how neocloud growth is financed

Neocloud growth is financed primarily with debt collateralized by the GPUs themselves, and CoreWeave is the clearest case: it carries roughly $24.9 billion of total debt plus about $10.1 billion of operating-lease obligations, for total financial commitments near $35 billion. The signature instrument is the GPU-backed loan — a facility secured against the chips and the contracts they serve. CoreWeave pioneered the structure, and on March 31, 2026 it closed an $8.5 billion GPU-backed financing facility, on top of earlier delayed-draw term loans that ran into double-digit interest rates.

That leverage is now expensive. CoreWeave’s net interest expense in Q1 2026 was $536 million, up from $264 million a year earlier — and full-year 2026 interest expense is guided to $2.6-2.9 billion against operating income of just $900 million to $1.1 billion. Read that again: interest expense is guided to roughly three times operating income. The company is profitable at the EBITDA line and deeply unprofitable once the cost of its own balance sheet is counted.

Nebius has chosen a different starting point. It inherited a debt-light position and a 500-person engineering team out of the former Yandex Cloud, and it intends to fund its new Microsoft and Meta capacity largely through asset-backed financing tied to those specific contracts — borrowing against signed revenue rather than against speculative buildout. Crusoe, still private, raised $1.375 billion of equity in its October 2025 Series E rather than leaning first on debt, which gives it more room before any refinancing pressure begins.

Industry-wide, there are now more than $20 billion in outstanding loans collateralized by NVIDIA GPUs. The collateral is an asset that loses value every quarter — a structure short-seller Jim Chanos has flagged as a candidate for ‘debt defaults’ if utilization or chip resale values weaken.

| Metric | CoreWeave | Nebius | Crusoe |

|---|---|---|---|

| Status | Public (CRWV) | Public (NBIS) | Private |

| Q1 2026 revenue | $2.08B (+112%) | $399M (+684%) | Not disclosed |

| FY2025 revenue | $5.13B | $529.8M | Not disclosed |

| Contracted backlog | $99.4B | Up to ~$46B (Meta + MSFT) | Not disclosed |

| Total debt | ~$24.9B | Debt-light, ABF-led | Equity-led (Series E) |

| GPU depreciation | 6 years | 4 years | Not disclosed |

| Headline deal | Multiple labs + Meta | Meta up to $27B; MSFT up to $19.4B | $1.375B Series E at $10B+ |

Depreciation policy: where the profits are really made

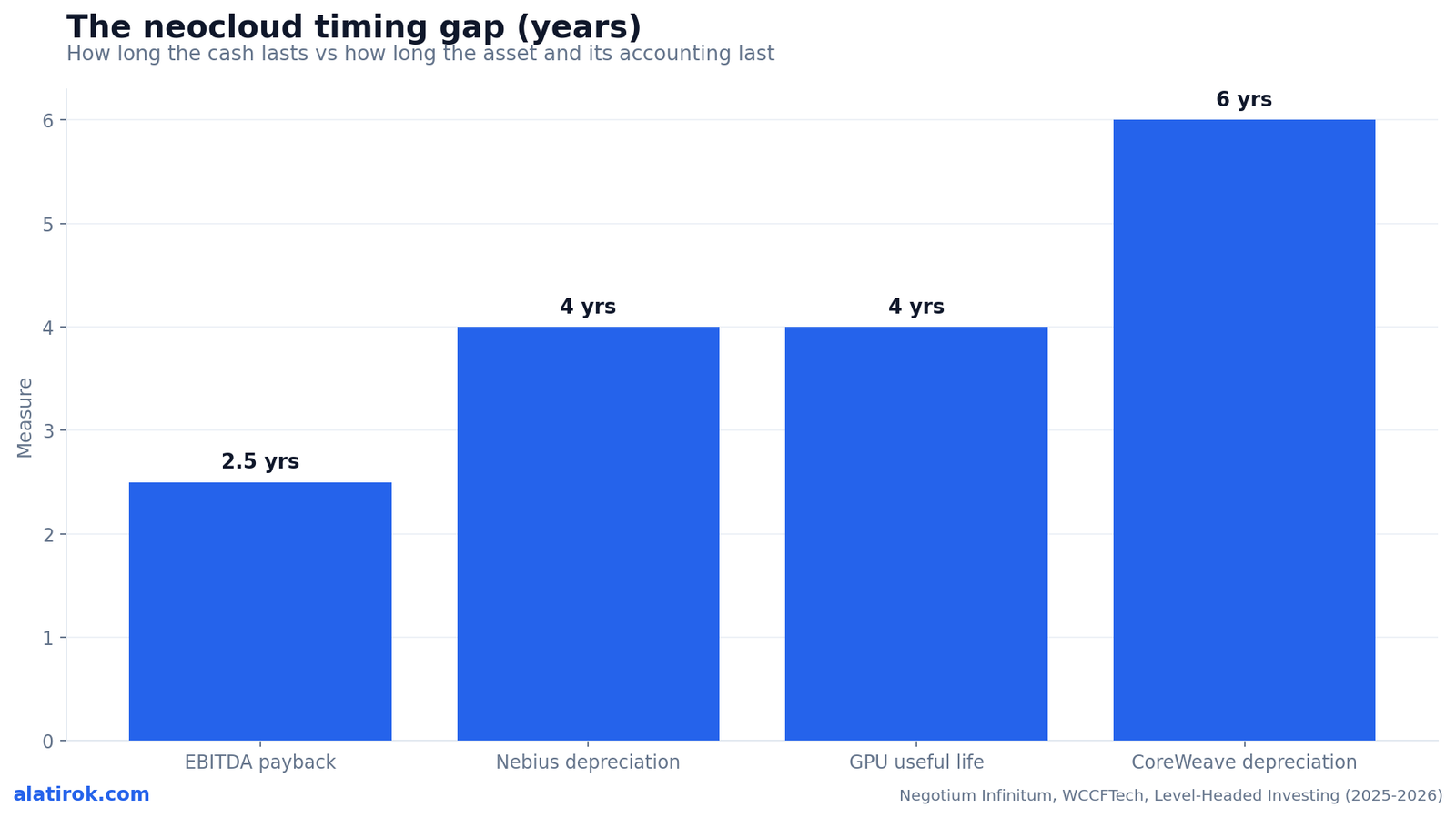

The single most important accounting choice a neocloud makes is how many years it spreads a GPU’s cost over — and CoreWeave’s 6-year schedule versus Nebius’s 4-year schedule materially flatters CoreWeave’s reported margins on identical hardware. CoreWeave depreciates its technology equipment, including NVIDIA GPUs, straight-line over six years, a figure it extended from four years back in January 2023. Nebius depreciates the same class of chips over four years. Neither company is wrong; they are simply making different bets about how long an H100 or H200 stays economically useful.

The mechanical effect is large. Spread a $30,000 GPU over six years and you book roughly $5,000 of annual depreciation; spread it over three or four years and you book $7,500 to $10,000. The longer schedule lowers reported expense, which lifts operating margin and net income today. It is the accounting equivalent of assuming your car will run for nine years instead of five — your monthly costs look lower until the engine fails on the original timeline anyway.

The risk lands later. If a GPU is genuinely obsolete after three to four years — which Michael Burry, among others, argues is closer to the truth as each NVIDIA generation leaps ahead — then a six-year schedule leaves unrecovered book value on the balance sheet that must eventually be written off as an impairment. Nebius’s faster schedule pulls that pain forward, depressing today’s margins in exchange for a cleaner balance sheet tomorrow. When you compare two neoclouds’ profitability, you are partly comparing their honesty about obsolescence.

“Longer depreciation improves profitability optics today but risks painful impairments tomorrow. The schedule is a forecast of obsolescence dressed up as an accounting policy.”

Synthesis of WCCFTech and Bizety analyses, 2025-2026

The payback gap: 2.5 years of earning, 3-4 years of life

The structural tension in neocloud economics is that a GPU pays back its cost in roughly 2.5 years on an EBITDA basis but effectively needs replacing in three to four years — leaving a window of only about a year of true surplus before the next capex wave hits. Operators love to quote the 2.5-year payback because it sounds fast. But EBITDA payback is not profit payback: it deliberately ignores depreciation, interest and the cost of the inevitable replacement. It measures how quickly the chip returns its purchase price in gross cash, not how much you actually keep.

Layer the timelines and the squeeze becomes visible. The 2.5-year EBITDA payback runs against a 3-4 year useful life, and against debt that often must be refinanced on a faster cadence than either. CoreWeave had about $986 million due in 2025 and roughly $4.2 billion needing refinancing in 2026, and on some measures close to 47% of its debt principal — around $11.7 billion — matures by the end of 2027. The cash a GPU earns in its productive window has to cover the interest, repay or roll the principal, and fund the next generation of chips, all at once.

This is why critics describe the model as a ‘perpetual replacement loop.’ Each cohort of GPUs throws off cash for a couple of good years, then the collateral value erodes just as replacement spending looms and debt comes due. The inflows look less like durable profit and more like a temporary return of capital that immediately has to be redeployed. The model works beautifully as long as demand keeps rising, financing stays cheap, and resale values hold — and all three of those conditions are outside the operators’ control.

Why EBITDA payback overstates the real picture

EBITDA strips out depreciation and interest — the two largest real costs of a debt-funded, fast-depreciating asset. A 2.5-year EBITDA payback can coexist with negative net income and even negative operating cash flow. In H1 2025, for example, CoreWeave reported negative operating cash flow even as adjusted EBITDA looked healthy, because depreciation ran near half of revenue and debt service consumed billions.What could break the loop

Three triggers: a demand pause that drops utilization below the level needed to service debt; a credit-market tightening that makes refinancing the 2026-2027 maturity wall expensive or impossible; or a collapse in GPU resale values that guts the collateral behind $20B+ of loans. Any one of them turns a manageable refinancing into a distressed one.Three operators, three strategies

CoreWeave is the leveraged scale play, Nebius is the contract-anchored fast follower, and Crusoe is the equity-cushioned vertically integrated bet — and the differences are as much about financing philosophy as about technology. CoreWeave is by far the largest: $5.13 billion of 2025 revenue (up from $1.92 billion in 2024), 43 data centers, and a plan to roughly double active power from about 850 megawatts toward more than 1.7 gigawatts in 2026. It became the fastest cloud provider in history to reach $5 billion in annual revenue, and it got there by borrowing aggressively against its chips.

Nebius is the fast follower with a cleaner balance sheet and a Yandex-derived engineering pedigree. Its 684% growth flatters a small base, but the Meta and Microsoft deals give it contracted demand on a scale that lets it fund expansion through asset-backed financing tied to named, creditworthy counterparties rather than speculative buildout. Its 4-year depreciation schedule signals a more conservative posture on obsolescence, at the cost of thinner reported margins today.

Crusoe is the wildcard. Still private, it closed a $1.375 billion oversubscribed Series E in October 2025 at a valuation above $10 billion, co-led by Valor Equity Partners and Mubadala Capital with NVIDIA participating. It does not disclose 2026 revenue or backlog, but reported that Crusoe Cloud bookings grew fivefold across the first three quarters of 2025, and it has brought a 1.2-gigawatt campus in Abilene, Texas online with a 1.8-gigawatt Wyoming facility under development. Equity funding buys it time and privacy buys it quiet — both real advantages, and both ways to defer the scrutiny the public players face every quarter.

Pros

Cons

How to read a neocloud’s numbers without getting fooled

Neocloud economics in 2026 are a race between cash and obsolescence

To judge a neocloud honestly, ignore the backlog headline and the EBITDA payback, and instead line up four things: net income after interest, the depreciation schedule, the debt maturity wall, and customer concentration. Each of those is harder to dress up than the growth metrics operators lead with, and together they tell you whether the business is compounding value or just compounding obligations.

Start with the depreciation schedule, because it silently sets the margin. If two operators report similar margins but one depreciates over six years and the other over four, the four-year company is the more profitable business — its reported numbers already absorb a cost the six-year company has merely deferred. Then check the maturity wall: a company refinancing billions every single year is hostage to credit conditions, and as a customer you inherit that risk through your pricing.

Finally, weigh the contracts. A $99 billion backlog concentrated in a handful of counterparties is a different risk profile from the same backlog spread across hundreds. The neocloud thesis is fundamentally a bet that AI compute demand keeps outrunning supply long enough for these companies to repay debt taken on against assets that are wearing out. It may well prove right. But it is a leveraged, time-sensitive bet, and the operators who survive will be the ones whose cash arrived before their bills did.

Builder’s take

I run compute-hungry products (Cyntr’s orchestration engine, Loomfeed’s feed pipeline), so I read neocloud filings the way a tenant reads a landlord’s mortgage. Here is what actually matters under the growth headlines.

- The backlog number is a sales funnel, not a bank balance. A $99B backlog only converts if customers stay solvent and the contracts are take-or-pay. Discount it by counterparty concentration before you celebrate.

- Depreciation policy is the whole argument. CoreWeave’s 6-year schedule and Nebius’s 4-year schedule describe the same H100s; the difference is purely which company is reporting profits it may have to give back later as impairments.

- EBITDA payback in ~2.5 years against a 3-4 year replacement cycle is a razor-thin window. There is roughly one year of true surplus before the next capex wave, and that surplus is what has to service the debt.

- If you buy GPU capacity, ask for the maturity wall, not the valuation. A vendor refinancing billions every year is one credit-market hiccup away from renegotiating your price.

- Private players like Crusoe get to skip the quarterly autopsy. That is an advantage in narrative and a blind spot for buyers — you cannot price risk you cannot see.

Frequently asked questions

A neocloud is a specialized cloud provider that rents out racks of AI accelerators — primarily NVIDIA GPUs — for training and inference, without the broad software and services portfolio of hyperscalers like AWS or Azure. CoreWeave, Nebius and Crusoe are the leading examples. Their economics revolve almost entirely around buying GPUs with borrowed money and renting them out under multi-year contracts.

CoreWeave reported a $99.4 billion revenue backlog in Q1 2026 — the total of contracted future payments. Management expects 36% to convert within 24 months and 75% within four years. Backlog signals demand and bargaining power, but it is not guaranteed revenue: it depends on customers staying solvent and on the contracts’ termination and option terms, and it is concentrated in a small number of counterparties.

CoreWeave depreciates GPUs straight-line over six years (extended from four in January 2023), while Nebius uses a four-year schedule. The longer schedule books less depreciation each year, which raises reported margins and net income today. The risk is that if GPUs are obsolete in three to four years, CoreWeave carries unrecovered book value that must later be written off as an impairment. Nebius’s faster schedule pulls that cost forward.

Typical neocloud EBITDA payback is about 2.5 years — the chip returns its purchase price in gross cash that fast. It is misleading because EBITDA excludes depreciation, interest and the cost of replacing the chip. Since GPUs effectively need replacing in three to four years, there is only about a year of true surplus before the next capex wave, and that surplus must also service the debt.

CoreWeave alone carries roughly $24.9 billion of total debt plus about $10.1 billion of operating-lease obligations. Industry-wide there are more than $20 billion in loans collateralized by NVIDIA GPUs — collateral that depreciates every quarter. CoreWeave had about $4.2 billion needing refinancing in 2026 and roughly $11.7 billion (about 47% of principal) maturing by end-2027, leaving it exposed to credit-market conditions.

Crusoe is still a private company. It closed a $1.375 billion Series E at a valuation above $10 billion in October 2025 and reported that Crusoe Cloud bookings grew fivefold over the first three quarters of 2025, but it has not disclosed 2026 revenue or backlog. As a private firm funded largely by equity, it faces less quarterly scrutiny and less near-term refinancing pressure than its public peers.

Primary sources

- CoreWeave Reports Strong First Quarter 2026 Results — CoreWeave Investor Relations

- CoreWeave Q1 revenue doubles as AI backlog nears $100B — StockTitan

- Nebius (NBIS) Q1 2026 Earnings Transcript — The Motley Fool

- Crusoe Announces Series E Funding — Crusoe

- CoreWeave Depreciates Its GPUs Over 6 Years, While Nebius Uses 4 Years — WCCFTech

- When Growth Runs on Debt: The CoreWeave Case Study — Level-Headed Investing

- CoreWeave Q1 2026 slides: revenue surges 112% as margins compress — Investing.com

- Neoclouds Hold More Than $20 Billion in GPU-Backed Debt — Dave Friedman / Negotium Infinitum

- CoreWeave Research Profile — MLQ.ai

- CoreWeave Reports 2025 Revenue of $5.13B with Backlog — Yahoo Finance

Last updated: June 1, 2026. Related: Capital.