InfiniBand owned 80% of AI clusters two years ago. By the end of 2025, Ethernet had flipped the back-end network. Here is the data behind the regime change.

The short answer: Ethernet won the AI back-end in 2025

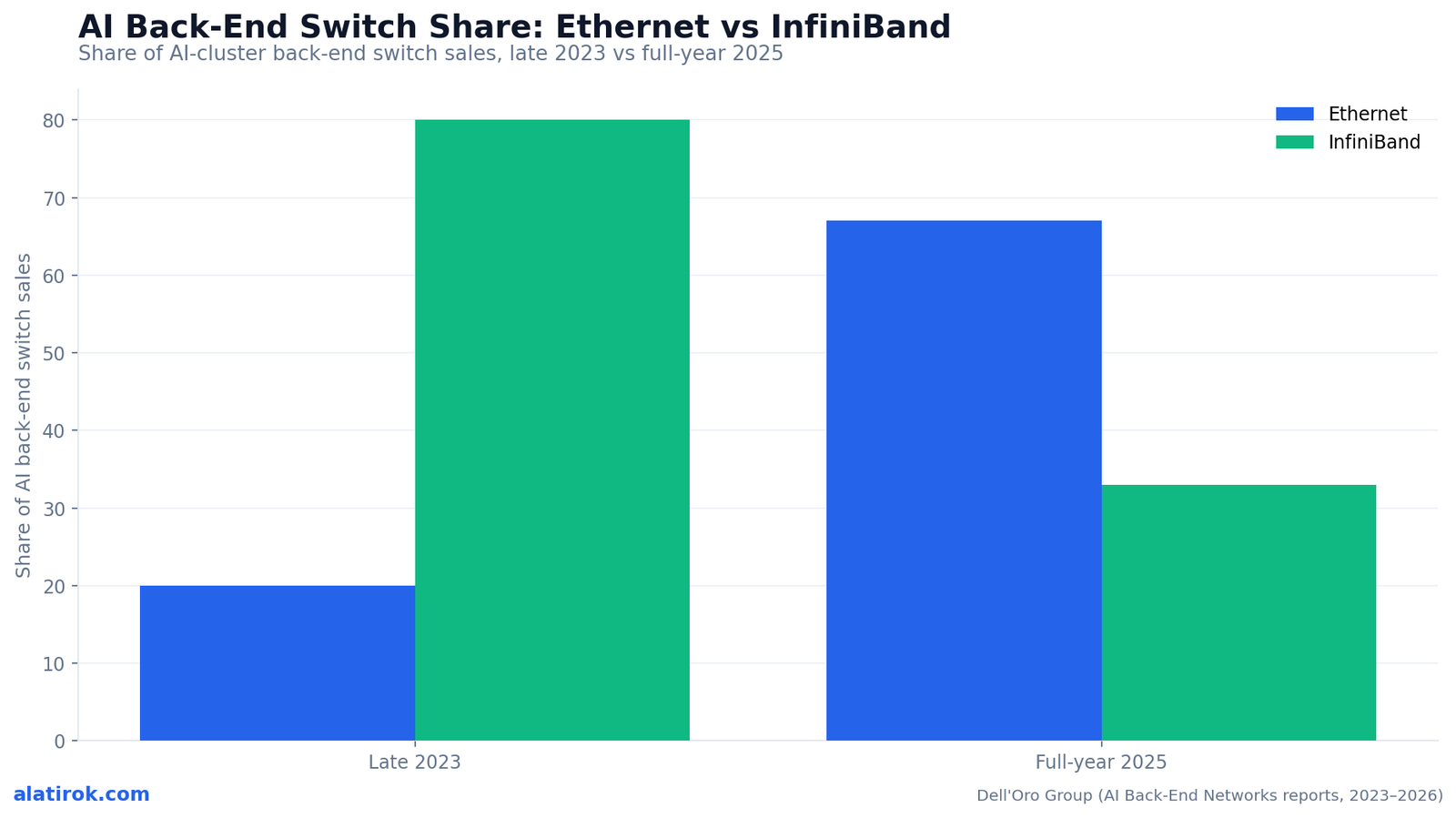

In AI data center networking 2026, Ethernet has decisively overtaken InfiniBand as the dominant fabric inside AI clusters — it accounted for more than two-thirds of AI back-end switch sales for full-year 2025, a near-mirror reversal of late 2023, when InfiniBand held over 80% of that segment. Dell’Oro Group, which began tracking AI back-end networks in late 2023, reports that Ethernet switch revenue in these clusters more than tripled in the fourth quarter of 2025 and now more than doubles the size of InfiniBand.

The “back-end network” is the fabric that stitches GPUs together so they can act like one machine — the east-west traffic that carries gradient updates during a training run or KV-cache shuffles during distributed inference. For years that job belonged almost exclusively to InfiniBand, the low-latency interconnect NVIDIA acquired with Mellanox in 2020. It was fast, it was lossless, and it was effectively single-vendor.

What flipped was not the physics. Ethernet did not suddenly get lower latency than InfiniBand. What changed is that the people buying the largest clusters on earth — Amazon, Microsoft, Meta, Oracle, and xAI among them — decided that a standards-based, multi-supplier fabric was worth more than InfiniBand’s incumbency, especially when clusters scaled past 100,000 accelerators and supply chains tightened. This is a capital-allocation story dressed up as a networking story, which is exactly why it matters.

Back-end vs front-end: the back-end network connects GPU to GPU (the high-bandwidth scale-out fabric). The front-end network connects servers to storage, the internet, and management planes. The Ethernet-vs-InfiniBand fight described here is almost entirely a back-end fight.

AI data center networking 2026: a near-complete reversal

The share swing is one of the fastest fabric transitions in data-center history: InfiniBand fell from over 80% of AI back-end switch sales in late 2023 to under one-third by full-year 2025, while Ethernet climbed from roughly 20% to over 66% in the same window. The crossover did not creep — it snapped, concentrated in the back half of 2025 as hyperscaler Ethernet deployments ramped in volume.

Dell’Oro’s quarterly cadence shows the momentum building through the year. By the third quarter of 2025, Ethernet already accounted for over two-thirds of switch sales in AI clusters; the full-year 2025 read confirmed Ethernet had more than doubled the dollar size of InfiniBand. Notably, InfiniBand itself did not collapse in absolute terms — its switch sales actually surged in 2Q 2025 — but it grew far slower than Ethernet, so its share eroded even as revenue rose. The market got bigger faster than InfiniBand could.

The chart below is the single clearest way to see the regime change: a 100%-stacked view of the AI back-end switch segment at the two endpoints of the transition.

Who is selling the Ethernet: NVIDIA leads its own disruption

The most counterintuitive fact in AI data center networking 2026 is that NVIDIA — the company that built and sold InfiniBand — is now the fastest-growing Ethernet vendor, with its Spectrum-X platform and partner Celestica together holding nearly half of the Ethernet AI back-end segment, per Dell’Oro. Accton, Arista, and Cisco rank next, with HPE/Juniper and Nokia scoring new accounts.

IDC’s broader datacenter-Ethernet tracker puts hard numbers on NVIDIA’s surge. In the second quarter of 2025, NVIDIA reached 25.9% of total datacenter Ethernet revenue (about $2.3B), up roughly 647% year over year — a 7.5x jump that vaulted it past both Arista (around 19%, ~$1.66B) and Cisco (around 14.5%, ~$1.26B) in that segment for the first time. NVIDIA’s own disclosures peg Spectrum-X at an annualized revenue run-rate exceeding $10B, inside a networking business that nearly doubled year over year to $7.3B in a single quarter.

Read that sequence carefully. NVIDIA did not lose the back-end network — it changed which product wins it. By leaning into Spectrum-X (Ethernet with NVIDIA’s congestion control and adaptive routing, paired with BlueField DPUs), the company kept its hooks in the fabric while conceding the protocol. The lesson for anyone studying lock-in: NVIDIA traded the InfiniBand moat for a wider Ethernet beachhead because the GPU is where the real defensibility lives.

IDC’s 25.9% is NVIDIA’s share of the broader datacenter Ethernet market, not the AI back-end-only segment. Dell’Oro’s ‘nearly 50% combined’ is NVIDIA plus Celestica specifically within AI back-end. The two datasets measure overlapping but different universes — do not add them together.

| Vendor | Q2 2025 datacenter Ethernet share | Approx. revenue | YoY growth | Position in AI back-end (Dell’Oro) |

|---|---|---|---|---|

| NVIDIA | 25.9% | ~$2.3B | ~+647% (7.5x) | Co-leads segment with Celestica (~50% combined) |

| Arista | ~19% | ~$1.66B | +34.2% | Ranks among top challengers |

| Cisco | ~14.5% | ~$1.26B | +9.1% | Accelerating with hyperscalers |

| Celestica | Not broken out by IDC | n/a | n/a | Co-leads AI back-end with NVIDIA |

| Accton | Not broken out by IDC | n/a | n/a | Next tier behind the leaders |

Why the buyers switched: it was never really about latency

Hyperscalers moved to Ethernet for supply diversity, scale economics, and roadmap control — not because Ethernet beat InfiniBand on raw latency. When a single cluster needs hundreds of thousands of ports and the same vendor also controls your GPU allocation, depending on that vendor for the network too becomes a procurement risk, not just an engineering choice.

Three forces did the work. First, scale: as clusters pushed past 100,000 accelerators, the buyers wanted a fabric with many interchangeable silicon suppliers (Broadcom, NVIDIA, Cisco, Marvell-based ODM gear) rather than one. Second, the Ultra Ethernet Consortium closed the technical gap, hardening Ethernet’s loss-handling and congestion control for AI traffic patterns so the latency penalty versus InfiniBand shrank to something hyperscalers could engineer around. Third, economics: Ethernet’s volume base — the entire internet runs on it — drives a cost and talent curve InfiniBand cannot match.

The named adopters tell the story plainly. Amazon, Microsoft, Meta, Oracle, and xAI are all building AI back-ends on Ethernet. When five of the largest infrastructure buyers on the planet make the same call inside eighteen months, the question stops being ‘will Ethernet win’ and becomes ‘how fast does the rest of the market follow.’

Pros

Cons

The optics squeeze: where the real 2026 bottleneck lives

$16.5B → $26B

AI optical transceiver market, 2025 to 2026

~57–60% YoY (TrendForce / LightCounting)

33.5M units

Goldman Sachs 2026 800G demand forecast

Raised 58% over prior estimate

~7M units

Goldman Sachs 2026 1.6T module forecast

1.6T enters volume in 2H 2026

1:8

Optical module-to-accelerator ratio (some ASIC designs)

Up from ~1:3 on H100-era gear

The harder constraint in AI data center networking 2026 is not the switch silicon — it is the optical transceiver, the part that is exploding in demand, prone to failure, and increasingly back-ordered. The AI optical transceiver market grew from about $16.5B in 2025 to roughly $26B in 2026, a ~57–60% year-over-year jump, per TrendForce and LightCounting.

Optics scale with port count, and port count scales faster than GPU count. The ratio of optical modules to accelerators has climbed from roughly 1:3 on H100-era designs toward 1:4.5 on newer parts and as high as 1:8 in some ASIC-based architectures. That is why Goldman Sachs raised its 2026 demand forecast for 800G transceivers to 33.5 million units (a 58% increase over its prior estimate) and pegged 1.6T modules at around 7 million units. TrendForce flagged component shortages — not switch capacity — as the primary bottleneck on capacity expansion.

For builders, this reframes the whole project plan. You can order the switches and the GPUs and still be stalled by a transceiver lead time. The optical module is now the critical path item in standing up a cluster, and it is the line on the bill of materials most likely to slip a deployment by a quarter.

“You can order the switches and the GPUs and still be stalled by a transceiver lead time. The optical module is now the critical path.”

On the real 2026 bottleneck

The roadmap: 800G now, 1.6T in late 2026, $100B by 2030

800Gbps switches made up the vast majority of Ethernet AI back-end shipments through Q4 2025; 1.6Tbps gear begins volume shipping in the second half of 2026, and cumulative AI back-end switch spending is set to surpass $100B by 2030, per Dell’Oro. The port-speed cadence is roughly a doubling every two years: 800G today, 1600G by 2027, and 3200G targeted for 2030.

Dell’Oro frames the $100B-plus opportunity across three expanding domains. Scale-up tightly couples GPUs and memory within a system (where NVLink and the emerging UALink compete). Scale-out connects GPUs across racks (the classic back-end fabric). And scale-across — the newest frontier — links geographically distributed data centers into a single logical cluster, a response to the reality that no single site can supply enough power. Ethernet is positioned as the long-term winner across scale-up and scale-out, even against proprietary alternatives.

One demand-side surprise: Dell’Oro identifies Neo Clouds — specialized GPU-rental providers like CoreWeave and its peers — as the fastest-growing customer segment across the forecast. That matters for anyone renting capacity, because it means a growing slice of the world’s AI fabric is being built by companies whose entire business is selling that fabric’s output by the hour.

What is ‘scale-across’ and why does it suddenly matter?

Scale-across interconnects multiple physical data centers into one logical training cluster, using long-reach coherent optics (800G/1.6T ZR/ZR+) between sites. It exists because individual sites are hitting power and land limits — if you cannot put 1GW in one building, you split the cluster across buildings and stitch them with the fabric. It is the newest of Dell’Oro’s three domains and a key driver of the post-2027 spending curve.Does this mean InfiniBand is dead?

No. InfiniBand switch revenue was still growing in absolute terms through 2025 — it even surged in Q2 2025. What it lost was share, because Ethernet grew far faster. InfiniBand remains a strong choice for tightly integrated turnkey NVIDIA clusters and latency-critical HPC. It is being out-grown, not replaced overnight.What this means if you build or rent AI infrastructure

Verdict: the AI back-end network is now an Ethernet market — but the bottleneck moved to the optics

The practical takeaway for 2026: bet on Ethernet for new back-end builds, treat optical transceivers as your critical-path procurement item, and watch port-speed timing so you do not buy a cluster that is a generation behind by the time it ships. The fabric question is now largely settled in Ethernet’s favor; the open questions are supply, speed grade, and which vendor’s Ethernet extensions you are willing to depend on.

For teams renting capacity — most AI startups, Cyntr included — the upside of the Ethernet flip is structural: multi-vendor fabric means the per-GPU-hour price is less likely to be dictated by a single supplier’s allocation desk, and the rapid 800G-to-1.6T cadence keeps pushing effective bandwidth up. The risk to watch is the optics shortage flowing through to availability and pricing of the newest, fastest instances.

For teams building their own clusters, the discipline is sequencing. Lock transceiver supply before you finalize switch and GPU orders, stage purchases around the 1.6T ramp in the second half of 2026, and decide deliberately how much vendor-specific Ethernet tuning (Spectrum-X-style) you want in your stack versus how much standards-only portability you want to preserve. That single decision is the new lock-in frontier now that the protocol war is over.

Builder’s take

I build Cyntr’s orchestration on rented GPU capacity, so the network fabric under those GPUs is not an abstraction to me — it shows up in latency tails and in the bill. The Ethernet flip is the most underrated infrastructure story of the year, and here is why it matters if you ship anything on top of a cluster.

- The thing that changed is not the wire — it is who controls the roadmap. InfiniBand was a single-vendor lane; Ethernet is a standards body plus a dozen silicon suppliers. When you are renting capacity, that diversity is what keeps your per-GPU-hour price from being set by one company’s allocation desk.

- Watch the optics, not the switch. The transceiver market roughly grew from $16.5B to $26B in a single year. Optical modules are now the part that fails, the part that is back-ordered, and the part that throttles how fast a Neo Cloud can actually light up the racks it already paid for.

- NVIDIA winning the Ethernet share race with Spectrum-X is the tell. The company that built InfiniBand is now the fastest-growing Ethernet vendor. That is not a contradiction — it is NVIDIA conceding the protocol war to keep the GPU war. Read it as a signal about where lock-in is actually defensible.

- If you are sizing a 2026 build, do not over-index on 800G being the floor forever. 1.6T volume shipping in the second half of 2026 means the gear you buy in Q1 may be a generation behind by Q4. Lease, stage, and leave headroom.

Frequently asked questions

Yes, in the back-end (GPU-to-GPU) network. Dell’Oro Group reports Ethernet accounted for more than two-thirds of AI back-end switch sales for full-year 2025 and more than doubled the dollar size of InfiniBand, a reversal from late 2023 when InfiniBand held over 80% of that segment.

Mainly for supply diversity, scale economics, and roadmap control rather than latency. As clusters grew past 100,000 accelerators, buyers like Amazon, Microsoft, Meta, Oracle, and xAI wanted a standards-based fabric with many silicon suppliers. The Ultra Ethernet Consortium also narrowed Ethernet’s AI-traffic performance gap with InfiniBand.

NVIDIA, surprisingly, given it also built InfiniBand. Per Dell’Oro, NVIDIA (via Spectrum-X) and Celestica together hold nearly 50% of the Ethernet AI back-end segment. IDC’s broader datacenter Ethernet tracker put NVIDIA at 25.9% share (~$2.3B) in Q2 2025, up about 647% year over year, ahead of Arista and Cisco.

About $26 billion in 2026, up from roughly $16.5 billion in 2025 — a ~57–60% jump, per TrendForce and LightCounting. Goldman Sachs raised its 2026 800G demand forecast to 33.5 million units and estimates around 7 million 1.6T modules. Component shortages, not switch capacity, are the main bottleneck.

The second half of 2026, per Dell’Oro Group. 800Gbps gear made up the vast majority of Ethernet AI back-end shipments through Q4 2025. The port-speed roadmap roughly doubles every two years: 800G today, 1600G by 2027, and 3200G targeted for 2030.

Cumulative spending on AI back-end data-center switches is forecast to surpass $100 billion by 2030, according to Dell’Oro Group’s February 2026 report. Growth is driven by scale-up, scale-out, and the newer scale-across architectures, with Neo Clouds the fastest-growing customer segment.

Primary sources

- Ethernet More Than Doubles Size of InfiniBand as Leading AI Scale-Out Fabric in 2025 — Dell’Oro Group

- AI Back-End Networks Now Over Two-Thirds of 3Q 2025 Switch Sales in AI Clusters — Dell’Oro Group

- Ethernet is Winning the War Against InfiniBand in AI Back-End Networks — Dell’Oro Group

- AI Back-End Switch Market Will Push Past $100 Billion by 2030 — Dell’Oro Group

- Nvidia Takes The Commanding Lead In Datacenter Ethernet Switching — The Next Platform

- Global AI Optical Transceiver Market to Reach US$26 Billion in 2026 — TrendForce

- AI Optical Transceiver Market to Grow 57% to US$26bn in 2026 — Semiconductor Today

- Goldman Sachs Optical Module Demand Forecast — Optical Communications in the AI Supernode Era — HTF

Last updated: June 1, 2026. Related: Capital.