The four hyperscalers guided to roughly $725 billion in 2026 capex, up 77 percent in a year. Here is the per-company breakdown and why free cash flow is collapsing.

How big is big tech AI capex in 2026?

Combined 2026 capital expenditure for the four largest US hyperscalers — Microsoft, Amazon, Alphabet, and Meta — is on track to reach roughly $725 billion, up about 77 percent from the record $410 billion they spent in 2025. That figure comes from each company’s first-quarter 2026 earnings guidance, and the vast majority of it is earmarked for AI infrastructure: GPUs, custom silicon, servers, networking gear, and the data centers and power to run them, per reporting from Tom’s Hardware.

To put $725 billion in perspective, it roughly approaches what the entire non-tech cohort of the S&P 500 spent on capex the prior year. This is no longer a line item — it is one of the largest sustained private investment cycles in modern corporate history, and it is being financed by a handful of companies in a single 12-month window.

A caveat up front, because it matters: every number in this article is reported guidance, not audited actuals. Companies revised these figures upward repeatedly through Q1 2026, and broader analyst tallies that fold in Oracle run higher still. Morgan Stanley, for instance, pegs the five-name group (adding Oracle) at roughly $805 billion for 2026. Treat the $725 billion as the four-company guidance midpoint, and treat everything below as a snapshot that will move.

What is the per-company big tech AI capex breakdown?

$725B

Combined 2026 capex (4 hyperscalers)

Up ~77% from 2025

$410B

2025 combined capex baseline

Prior record

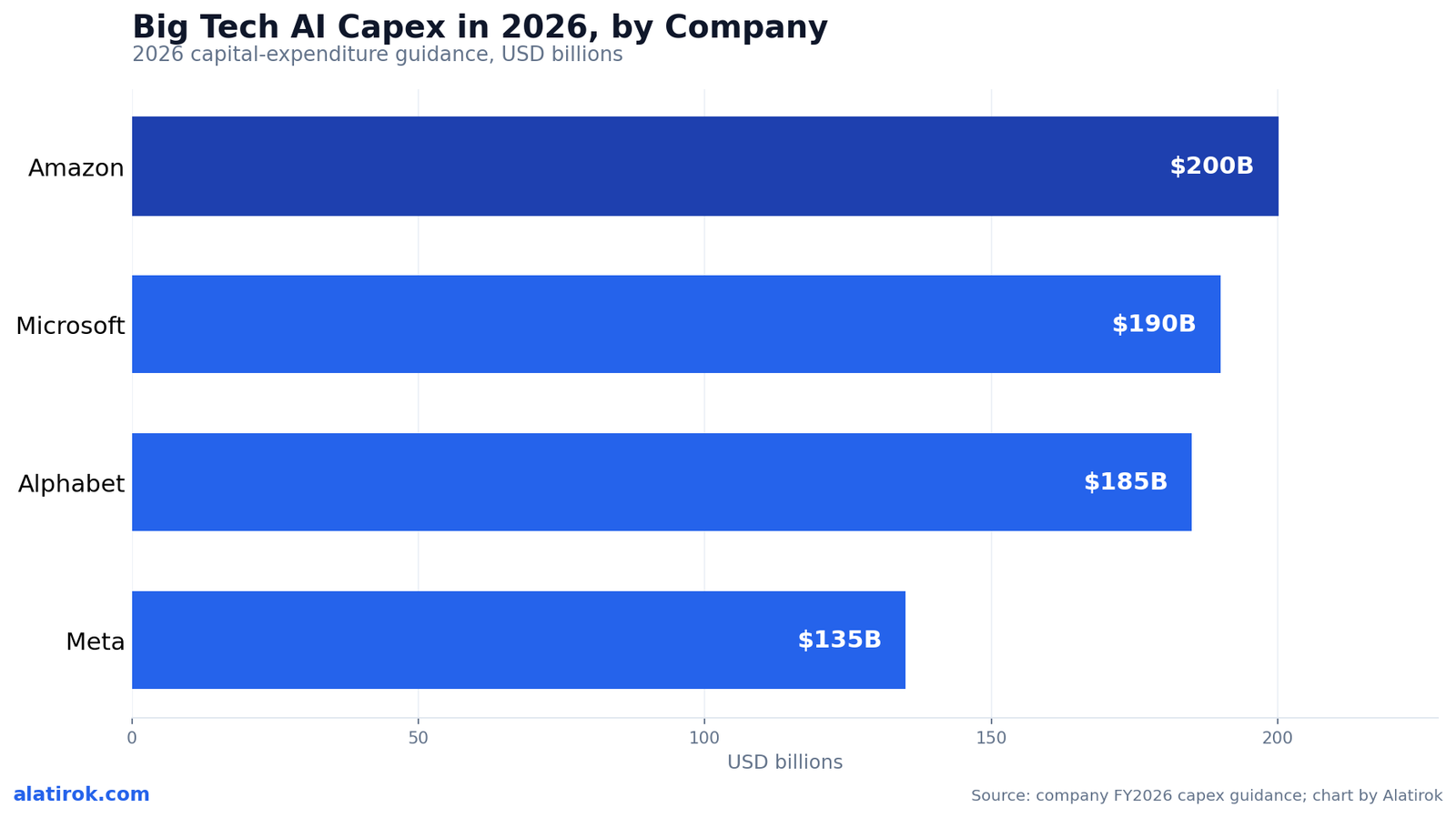

$200B

Amazon 2026 guidance

Largest single commitment

$25B

Microsoft capex from cost inflation

Per CFO Amy Hood

Amazon leads at roughly $200 billion, followed by Microsoft at about $190 billion, Alphabet at $180–190 billion, and Meta at $125–145 billion for full-year 2026. Those four guidance figures, when taken near their midpoints, sum to roughly $725 billion. Each company crossed the $100 billion annual capex threshold individually — a line none of them had approached two years earlier.

The dispersion in investor reaction tells you as much as the numbers. When companies reported in late April, Alphabet’s stock rose around 7 percent while Meta’s fell more than 6 percent, even though both raised guidance, according to Fortune. The difference was demonstrable return: Alphabet showed Google Cloud revenue of about $20 billion, up 63 percent year-over-year, with a $462 billion backlog. Meta offered what investors heard as vaguer assurances about “leading models and leading products.”

The lesson for anyone tracking big tech AI capex is that the market is no longer rewarding spend for its own sake. It is pricing the gap between dollars going out and revenue coming back — and that gap looks very different at a cloud business with external customers than at a company funding the buildout largely off its core ad engine.

| Company | 2026 capex guidance | Notable detail |

|---|---|---|

| Amazon | ~$200 billion | Largest single commitment; bulk tied to AWS AI capacity |

| Microsoft | ~$190 billion | $25B attributed to memory and component cost inflation |

| Alphabet | $180–190 billion | Raised from $175–185B; Cloud backlog ~$462B |

| Meta | $125–145 billion | Raised $10B at both ends; issued ~$55B in debt |

| Combined (4) | ~$725 billion | Up ~77% from 2025’s ~$410 billion |

Why did memory and component costs add $25 billion?

Microsoft CFO Amy Hood told investors that roughly $25 billion of the company’s record 2026 capex is attributable not to buying more hardware, but to paying more for the same hardware — driven by surging memory and component prices. In other words, a meaningful slice of the headline number is inflation, not expansion, per Tom’s Hardware.

The pressure is concentrated in memory. DRAM contract prices reportedly jumped around 95 percent quarter-over-quarter in early 2026, with further increases of 58 to 63 percent projected for the following quarter, as server DRAM and high-density DDR5 modules consumed most available production capacity. AI servers are memory-hungry in a way traditional cloud servers never were, so the hyperscalers are competing for the same constrained supply.

This reframes the whole capex narrative. A 77 percent year-over-year jump sounds like 77 percent more compute. It is not. Some of that growth is the same buildout costing dramatically more, which means the productive capacity added per dollar is lower than the raw spending implies — a subtlety that gets lost when only the topline circulates.

When a CFO attributes $25 billion of a $190 billion budget to component cost increases, roughly 13 percent of that company’s capex bought no additional capacity at all. Memory inflation is silently lowering the compute-per-dollar of the entire 2026 cycle.

What is the free-cash-flow squeeze, and how bad is it?

The free-cash-flow squeeze is the gap between the cash these companies generate from operations and the far larger cash they are now spending on capex — a gap that is pushing several hyperscalers toward negative free cash flow in 2026. Combined free cash flow for the four is reportedly set to hit its lowest level since 2014, when their revenues were roughly a seventh of today’s, according to BeInCrypto.

The individual figures are stark. Amazon is projected to burn roughly $10 billion of cash in 2026; Meta is expected to burn cash in the second half; Alphabet should stay positive but at its weakest level in more than a decade. Combined quarterly free cash flow could dip to around $4 billion in the third quarter, against a post-pandemic norm closer to $45 billion per quarter. Different analysts model it differently — Amazon’s 2026 free-cash-flow deficit has been estimated anywhere from negative $10 billion to negative $28 billion depending on lease and financing assumptions — so read these as scenarios, not certainties.

It is worth stressing that free cash flow turning negative is not the same as the businesses losing money. Operating profits remain large. What is happening is that capex is consuming, and in some cases exceeding, operating cash flow — so the cushion that funded buybacks and dividends is gone, and the marginal dollar of the buildout has to come from somewhere else.

“A 77 percent capex jump does not mean 77 percent more compute. Some of it is the same buildout costing far more, and some of it is being funded by debt rather than cash.”

On reading the 2026 hyperscaler numbers

How do depreciation and debt financing fit in?

Depreciation is the delayed bill for today’s capex, and debt is increasingly how the bill gets paid — together they are why the AI buildout pressures margins for years and ties the hyperscalers to the wider ‘circular financing‘ web. When a company spends on GPUs and servers, the cash leaves immediately but the expense is spread across the asset’s useful life, so the earnings hit shows up later and lingers.

Useful-life assumptions are doing heavy lifting here. Microsoft extended server useful life to six years; Meta has stretched its estimate to around five and a half. Longer lives lower annual depreciation and flatter near-term earnings — Microsoft’s earlier extension added billions to operating income. But critics, including analysts who scrutinize hyperscaler cash flow, argue AI accelerators may really last two to three years given Nvidia’s compressed upgrade cadence. If Meta trimmed its server life by a single year, 2026 depreciation could rise by more than $5 billion, with operating profit falling by a similar amount.

With internal cash no longer covering the spend, the hyperscalers have turned to debt — Meta issued roughly $55 billion in bonds over six months and paused buybacks; the broader group raised over $100 billion in 2025 with projections of well over a trillion in issuance ahead. That leverage feeds the ‘circular’ deal structures binding chipmakers, model labs, and cloud providers, where the same dollars cycle between Nvidia, OpenAI, Oracle, and the hyperscalers. None of these companies is fragile, but the model has shifted from self-funded to leveraged in under two years.

Why depreciation lags the capex headline

Capex is a cash outflow recorded when the asset is bought. Depreciation is the accounting expense that spreads that cost over the asset’s estimated useful life — typically five to six years for hyperscaler servers. So a 2026 spending spike does not fully hit the income statement until 2027 through 2031, which is why margin pressure ramps up well after the capex announcement.What ‘circular financing’ means here

It describes deal webs where capital loops between a small set of players: a chipmaker invests in a model lab, the lab commits to a cloud provider, the cloud provider buys the chipmaker’s hardware, and debt or equity stakes tie them together. Critics warn it can inflate apparent demand; defenders note the underlying revenue and compute consumption are real. The risk is concentration, not fraud.Will big tech AI capex really hit $1 trillion in 2027?

A record buildout, financed on borrowed time

Quite possibly — Morgan Stanley now projects roughly $1.1 trillion in 2027 capex across the five-name hyperscaler group that includes Oracle, up from a prior $951 billion estimate, after lifting its 2026 figure to about $805 billion. The trajectory the bank describes is no longer linear but accelerating, per FXStreet.

Treat the trillion-dollar headline with the same caution as everything else here. It is an analyst forecast built on company guidance that has been revised upward repeatedly, not a committed budget. The same forces that pushed 2026 higher — memory inflation, capacity constraints, competitive escalation — could push 2027 well past $1 trillion or, if demand or financing tightens, leave it short. Forecasts of exponential curves tend to be the first casualties of a cycle turn.

What is not in doubt is the direction. Even the conservative reading has these companies spending more in 2026 than they ever have, with depreciation and debt obligations that will shape their margins and balance sheets through the end of the decade. Whether that buildout earns its return is the trillion-dollar question — and the market has already started grading on it company by company.

Builder’s take

I run Cyntr, an agent orchestration runtime, so every dollar of this $725 billion eventually shows up in my inference bill. When you build on top of the hyperscalers, their capital cycle is not abstract macro news — it is your future COGS. Here is how I read the 2026 numbers as an operator who has to plan around them.

- The memory shock is the real story. Microsoft’s CFO pinning $25 billion of guidance on component costs tells you the bottleneck moved from GPUs to DRAM and HBM. If you buy inference, expect price floors to firm up before they fall.

- Depreciation, not capex, is the number to watch. These assets get expensed over five to six years, so the margin hit lands quarters after the spending headline. That delayed pain is what eventually gets passed to API customers.

- Free cash flow turning negative changes vendor behavior. When Amazon and Meta are burning cash, they get more disciplined about discounts and credits. I am locking in committed-use pricing now rather than betting on a price war.

- Diversify your compute the way they diversify their balance sheets. I keep Cyntr portable across providers precisely because the circular-financing risk concentrated in one ecosystem is not risk I want my runtime to inherit.

Frequently asked questions

The four largest US hyperscalers — Microsoft, Amazon, Alphabet, and Meta — guided to a combined ~$725 billion in 2026 capex, up roughly 77 percent from 2025’s ~$410 billion. Broader analyst tallies that include Oracle run higher, around $805 billion. All figures are reported guidance and subject to revision.

Amazon, at roughly $200 billion, has the largest single 2026 capex commitment, followed by Microsoft at about $190 billion, Alphabet at $180–190 billion, and Meta at $125–145 billion. Each crossed the $100 billion annual threshold individually for the first time.

CFO Amy Hood told investors that surging memory and component prices — DRAM contract prices reportedly rose around 95 percent quarter-over-quarter in early 2026 — meant roughly $25 billion of Microsoft’s $190 billion budget paid for cost inflation rather than additional capacity. It signals the bottleneck shifted from GPUs to memory.

It is the widening gap between the cash hyperscalers generate and the larger amount they spend on capex. Combined free cash flow is set to hit its lowest since 2014. Amazon may burn ~$10 billion in 2026, Meta is expected to burn cash in the second half, and Alphabet’s, while positive, is at a decade-plus low.

Capex leaves as cash immediately but is expensed over the asset’s useful life — typically five to six years for these companies. Longer assumed lives lower near-term depreciation and flatter earnings, but if AI chips truly last only two to three years, the gap understates the real cost. A one-year cut to Meta’s server life could add over $5 billion in 2026 depreciation.

Morgan Stanley projects roughly $1.1 trillion in 2027 across the five-name group including Oracle, after raising its 2026 estimate to about $805 billion. It is an analyst forecast built on repeatedly upgraded guidance, not a committed budget, so treat the trillion-dollar figure as a plausible trajectory rather than a certainty.

Primary sources

- Big Tech AI spending plans reach $725 billion, up 77% — Tom’s Hardware

- Microsoft attributes $25 billion of AI budget to memory and chip costs — Tom’s Hardware

- Only Google convinced investors its AI spending is paying off — Fortune

- Big Tech’s cash pile shrinks to decade low as AI spending soars — BeInCrypto

- Morgan Stanley: $1.1 trillion AI capex by 2027 — FXStreet

- AI hyperscalers: capital expenditure and free cash flow — The Footnotes Analyst

Last updated: May 31, 2026. Related: Capital.