I think AI agent consolidation is the most underappreciated near-term trend in software. The popular story says thousands of agent startups will bloom as models improve. My view is harsher: by 2028, most of today’s agent companies will either be acquired, merged, or reduced to niche products inside larger platforms. The reason is structural, not cyclical. Distribution is concentrating around model labs and incumbent software vendors, core model capabilities are becoming easier to buy from multiple providers, and venture-backed companies from the 2021–2022 cohorts will eventually need exits. Readers who want the market map should also see our roundup of $1B+ AI agent unicorns and our look at founder and funding data.

My contrarian take: the agent boom ends in roll-ups

2028

My timeline for broad consolidation

Opinion based on current platform, pricing, and funding dynamics

Base case: consolidation, not fragmentation

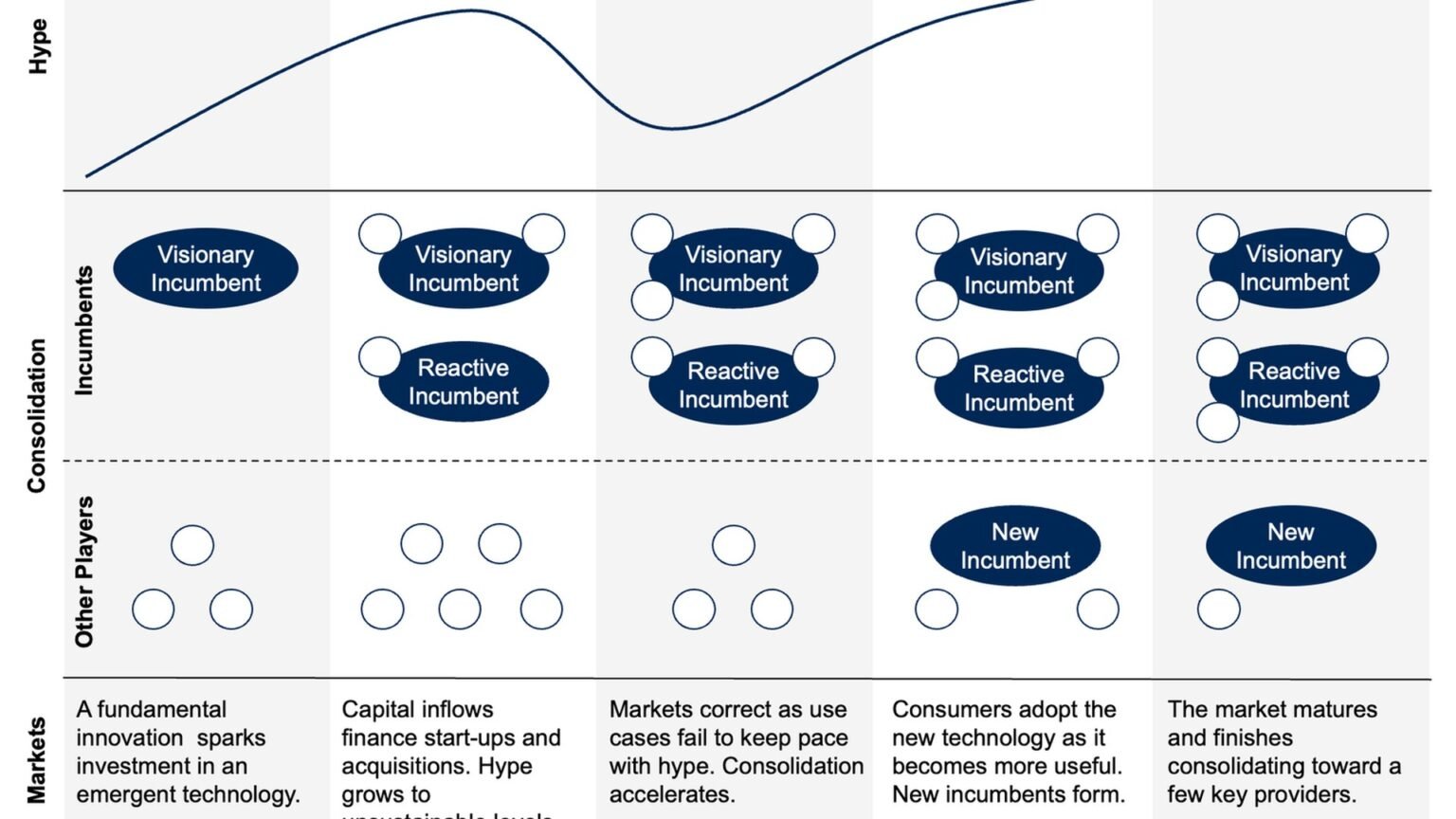

I think most AI agent startups will consolidate by 2028. Not because agents are overhyped, but because the category is becoming strategically important enough for larger platforms to own and economically difficult enough for smaller vendors to defend.

The bullish case for agent startups is easy to understand. Models keep getting better. Tool use is improving. Enterprises want software that can draft, search, summarize, route, and act. New companies can ship quickly because they can build on APIs from OpenAI, Anthropic, Google, and open-weight ecosystems. That creates the impression of an enormous greenfield.

What I see instead is a market that looks open at the feature layer but increasingly closed at the power layer. The companies with the strongest position are the ones that already control user traffic, developer mindshare, model supply, cloud credits, or the system of record where work actually happens. In practice, that means model labs, hyperscalers, and incumbent SaaS vendors have a built-in advantage over standalone agent startups.

This is not a claim that every startup loses. Some will build durable businesses. But if you look category by category, broad horizontal agents are starting to resemble features, while the surviving companies are more likely to be those with deep workflow ownership, proprietary data, compliance barriers, or embedded distribution.

📌 Opinion thesis. My base case is not agent collapse. It is agent demand paired with ownership concentration.

“The question is no longer whether agents matter. It is who gets to own the margin when they do.”

alatirok opinion

Distribution moats favor model labs and incumbents

The first reason I expect consolidation is distribution. OpenAI, Anthropic, and Google are not just model providers. They are increasingly product companies with direct user relationships, developer ecosystems, and enterprise sales motions. OpenAI has ChatGPT Enterprise and its API platform. Anthropic has Claude for enterprise use and a growing ecosystem around the Anthropic API and developer docs. Google has Gemini integrated across Workspace and Google Cloud, with agent tooling surfaced through its enterprise stack at Google Cloud.

If a startup is building a general-purpose research agent, coding agent, writing agent, or support agent, it is competing against vendors that can bundle similar capabilities into products customers already use. That matters more than raw model quality. Distribution lowers customer acquisition cost, shortens trust cycles, and makes it easier to cross-sell agent features as an add-on rather than a net-new budget line.

The same pattern shows up in software incumbents. Microsoft can push copilots across Microsoft 365, GitHub, Azure, and Dynamics. Salesforce can embed agents into CRM workflows through Agentforce. ServiceNow can add AI agents inside service management. Atlassian, HubSpot, Zendesk, and Adobe all have installed bases that make agent adoption easier than buying another standalone tool.

Startups often answer that they can move faster. That is true in the short run. It is less true once the platform owner decides the category is strategic. Then the startup is forced into a race where the incumbent has the customer, the data exhaust, the procurement relationship, and often the balance sheet to price aggressively.

Pros

Cons

| Advantage | Why it matters in agents | Who usually has it |

|---|---|---|

| Installed user base | Cuts acquisition cost and speeds adoption | Incumbent SaaS vendors and model labs |

| Workflow ownership | Lets agents act inside existing systems of record | CRM, productivity, ERP, and support platforms |

| Model access | Improves economics and feature velocity | Model labs and hyperscalers |

| Enterprise trust | Shortens security and procurement cycles | Large platforms with existing contracts |

Margin compression is coming for horizontal agent startups

The second reason is economics. A large share of agent startups depend on third-party model APIs. That creates a business with variable costs tied to someone else’s roadmap and pricing. If model quality improves and prices fall, customers benefit, but differentiation at the application layer can also erode unless the startup owns something more durable than prompting, orchestration, or a thin workflow wrapper.

OpenAI, Anthropic, Google, and open-source model providers are all pushing the frontier. Better reasoning, larger context windows, tool use, and multimodal capabilities reduce the amount of bespoke application logic needed to deliver a useful agent. That is great for adoption. It is not automatically great for margins.

I have heard founders argue that lower inference costs solve this problem. They help, but they do not remove it. If the underlying model layer gets cheaper and more capable for everyone, then price competition intensifies at the application layer unless the product is anchored in proprietary data, deep integrations, regulated workflows, or measurable ROI that is hard to replicate.

This is why I am skeptical of broad horizontal wrappers that market themselves as universal agents for every team. Universal products can grow quickly, but they are also easiest for model labs and incumbents to absorb. The more generic the workflow, the more likely the category compresses into a feature set.

⚠️ Economic pressure. If your gross margin depends on reselling third-party intelligence with limited proprietary data, you are exposed to both vendor pricing and feature convergence.

“Cheaper models expand the market, but they also flatten weak differentiation.”

alatirok opinion

M&A is no longer hypothetical

Signal from the market: strategic buyers are active

The third reason is simple: consolidation has already started. In 2025, Cognition announced it had acquired Windsurf, bringing together one of the best-known AI coding agent companies with a fast-growing AI-native development environment. Cognition published the deal on its official site at cognition.ai/blog.

OpenAI has also shown a willingness to buy infrastructure and talent. In 2024, OpenAI announced it had acquired Rockset, a database and search analytics company, to strengthen its products and enterprise stack. OpenAI published the announcement at openai.com.

Those are not identical transactions, and I do not want to overstate them. But they point in the same direction: strategic buyers are not waiting for the market to settle before pulling important capabilities in-house. If you are a startup sitting between the model layer and the workflow layer, you are a natural acquisition target when your product proves demand but your moat remains incomplete.

I expect more of this in coding, customer support, sales automation, enterprise search, browser agents, and orchestration tooling. Some deals will be talent acquisitions. Some will be tuck-ins for distribution. Some will be defensive moves by incumbents that do not want a fast-moving startup to become the default interface for their own customers.

| Buyer | Target | What it signals |

|---|---|---|

| Cognition | Windsurf | Coding-agent leaders are combining product, IDE, and agent workflows |

| OpenAI | Rockset | Model labs are willing to buy infrastructure to deepen enterprise capabilities |

The VC clock matters more than founders admit

The fourth reason is capital. A lot of AI startups were funded into a market that rewarded speed, narrative, and category creation. That was rational at the time. But venture funds still operate on a return cycle, and the 2021–2022 vintages cannot wait forever for every company to become a durable public-scale winner.

When the market is hot, investors talk about category kings. When the hold periods stretch, they also start asking harder questions about burn, retention, gross margin, and whether a company can really defend itself against platform encroachment. If the answer is mixed, M&A becomes the cleanest path to liquidity.

This is one reason I think the next two years will feel different from the last two. The conversation will shift from ‘Can this demo wow people?’ to ‘Can this company own a workflow, keep margins healthy, and survive when the platform ships the same headline feature?’ Startups that cannot answer those questions will still have value. They just may not have standalone value.

That dynamic is especially relevant in crowded categories where many startups raised on similar stories: AI sales reps, AI SDRs, AI support agents, AI meeting agents, AI browser operators, and generalized enterprise copilots. There will be winners. There will also be a long tail of companies that are easier to buy than to outgrow.

📌 Capital markets lens. Consolidation is often less about product failure than about fund timelines, strategic fit, and the narrowing set of plausible IPO-scale outcomes.

Which categories I expect to consolidate first

If I had to rank the categories most likely to consolidate, I would start with horizontal coding agents and AI-native developer environments, then generalized enterprise copilots, then customer support agents, then sales automation agents, then browser and computer-use agents sold as broad platforms. These are all valuable categories. They are also categories where platform overlap is intense and where the buyer often already has a preferred system of record.

Coding is the clearest example. The market is large, but the strategic gravity is enormous. Microsoft owns GitHub and Visual Studio Code. OpenAI, Anthropic, Google, and others all care deeply about developer workflows because coding is both a showcase and a distribution wedge. That does not mean independent coding companies cannot win. It does mean the category is likely to end up with fewer, larger players than the current startup count suggests.

Generalized enterprise copilots are another likely consolidation zone. If your product promises to answer questions, search documents, summarize meetings, and trigger actions across SaaS tools, you are entering territory that Microsoft, Google, Salesforce, ServiceNow, and Atlassian all want to own. The integration burden is high, but the moat is often low unless you have unique data access or a workflow buyers cannot get elsewhere.

Customer support and sales agents will also compress. The reason is not lack of demand. It is that the incumbent platforms already sit on the customer records, ticket histories, and workflow permissions that make automation useful. Standalone vendors can still build better experiences, but over time many of those capabilities are likely to be bundled, copied, or acquired.

| Category | My consolidation risk view | Why |

|---|---|---|

| Horizontal coding agents | Very high | Strategic to model labs and developer platforms; crowded field |

| General enterprise copilots | Very high | Incumbents already own productivity and workflow surfaces |

| Customer support agents | High | CRM and support platforms control the data and action layer |

| Sales automation agents | High | Strong overlap with CRM incumbents and crowded startup supply |

| Browser/computer-use platforms | High | Powerful demos, but broad use cases are easy for larger platforms to absorb |

Which categories can still stay independent

Best chance to stay independent: vertical workflow leaders

The strongest counterargument to my thesis is that some agent companies are building real vertical moats. I agree. In fact, the companies I am most willing to exempt from the consolidation wave are the ones that solve expensive, regulated, domain-specific problems with proprietary data and workflow depth.

Harvey is the kind of company people cite for a reason: legal work is specialized, high value, and embedded in professional workflows where trust and domain adaptation matter. Abridge is another important example because clinical documentation sits inside healthcare environments where compliance, integration, and workflow fit are not trivial. These are not generic wrappers around a model. They are products tied to domain expertise, data structures, and buyer pain that are harder to replace with a broad platform feature.

I would extend that logic to a few other areas: revenue cycle automation in healthcare, insurance claims workflows, regulated financial operations, and industrial or field-service environments where the agent needs to interact with messy real-world systems and domain-specific records. In those markets, the startup can build a moat around implementation depth, customer trust, and measurable ROI.

The dividing line, in my view, is whether the startup owns a mission-critical workflow that a horizontal platform cannot easily replicate. If yes, independence is plausible. If no, consolidation pressure rises sharply.

📌 Where I think startups can survive. Vertical agents with proprietary data, compliance depth, and workflow ownership have the best chance of remaining independent.

“Vertical depth is still the best defense against horizontal consolidation.”

alatirok opinion

| Category type | Survival odds | What creates the moat |

|---|---|---|

| Legal AI | Better than average | Domain expertise, workflow specificity, high-value use cases |

| Clinical documentation | Better than average | Compliance, integrations, provider workflow fit |

| Regulated financial operations | Moderate to strong | Auditability, controls, domain data |

| Generic productivity agents | Weak | Low switching costs and heavy platform overlap |

What would prove me wrong

Failure conditions for this thesis

I could be wrong if model labs remain disciplined and choose not to move aggressively into application ownership. I could be wrong if open-source models and inference competition reduce dependence on a few API providers enough that application-layer margins improve materially. I could be wrong if enterprise buyers decide they prefer neutral agent vendors over bundled platform offerings, even when the platform is cheaper.

I could also be wrong if the best startups build stronger moats than I expect through proprietary interaction data, superior evaluation systems, and workflow execution that is much harder to copy than today’s demos suggest. If agent reliability improves in a way that rewards specialized execution more than distribution, the independent winners could be more numerous than I think.

Still, my base case remains the same. The market is rewarding agent adoption, but the structure of the market points toward concentration. By 2028, I expect the headline to be less about how many agent startups were created and more about which ones managed to avoid being folded into someone else’s stack.

I could be wrong.

Frequently asked questions

In this article, AI agent consolidation means a market where many standalone agent startups are acquired, merged, or functionally displaced by larger platforms that bundle similar capabilities. You can see the platform direction in official product pages from OpenAI, Anthropic, and Google Cloud.

Many agent products rely on external models for reasoning, tool use, and multimodal capabilities. That means the application vendor is exposed to upstream pricing, capability changes, and feature overlap. Official developer documentation from OpenAI and Anthropic shows how central those APIs are to the current ecosystem.

Yes. OpenAI announced its acquisition of Rockset on its official site at openai.com. Cognition also announced its acquisition of Windsurf on its official blog at cognition.ai/blog.

The best candidates are vertical companies with domain-specific workflows, proprietary data, and compliance-heavy environments. Examples often discussed in the market include legal and healthcare-focused vendors such as Harvey and Abridge, where the product is tied to specialized workflows rather than generic productivity.

Primary sources

- OpenAI API — OpenAI

- OpenAI acquires Rockset — OpenAI

- Anthropic developer documentation — Anthropic

- Google Cloud — Google Cloud

- Salesforce Agentforce — Salesforce

- Cognition blog — Cognition

- Harvey — Harvey

- Abridge — Abridge

Last updated: May 20, 2026. Related: Agent Infrastructure.