The hard 2026 data on AI agent adoption: production rates, spend, ROI, abandonment, and the use cases that actually pay back, from McKinsey, Menlo, LangChain, Deloitte, a16z, MIT, and Gartner.

AI agent adoption in 2026: the headline numbers

By mid-2026, AI agent adoption has crossed from experiment to default in software, but real autonomous agents remain a small slice of what enterprises actually run. The most cited developer survey, LangChain’s State of AI Agents (1,340 respondents, fielded November 18 to December 2, 2025), found 57.3% of teams now have agents in production, up from 51% a year earlier, with another 30.4% actively building agents with concrete plans to deploy. On the buyer side, Andreessen Horowitz’s third annual CIO survey of 100 Global 2000 executives reported that 80% of enterprises have at least one production application that embeds an AI agent.

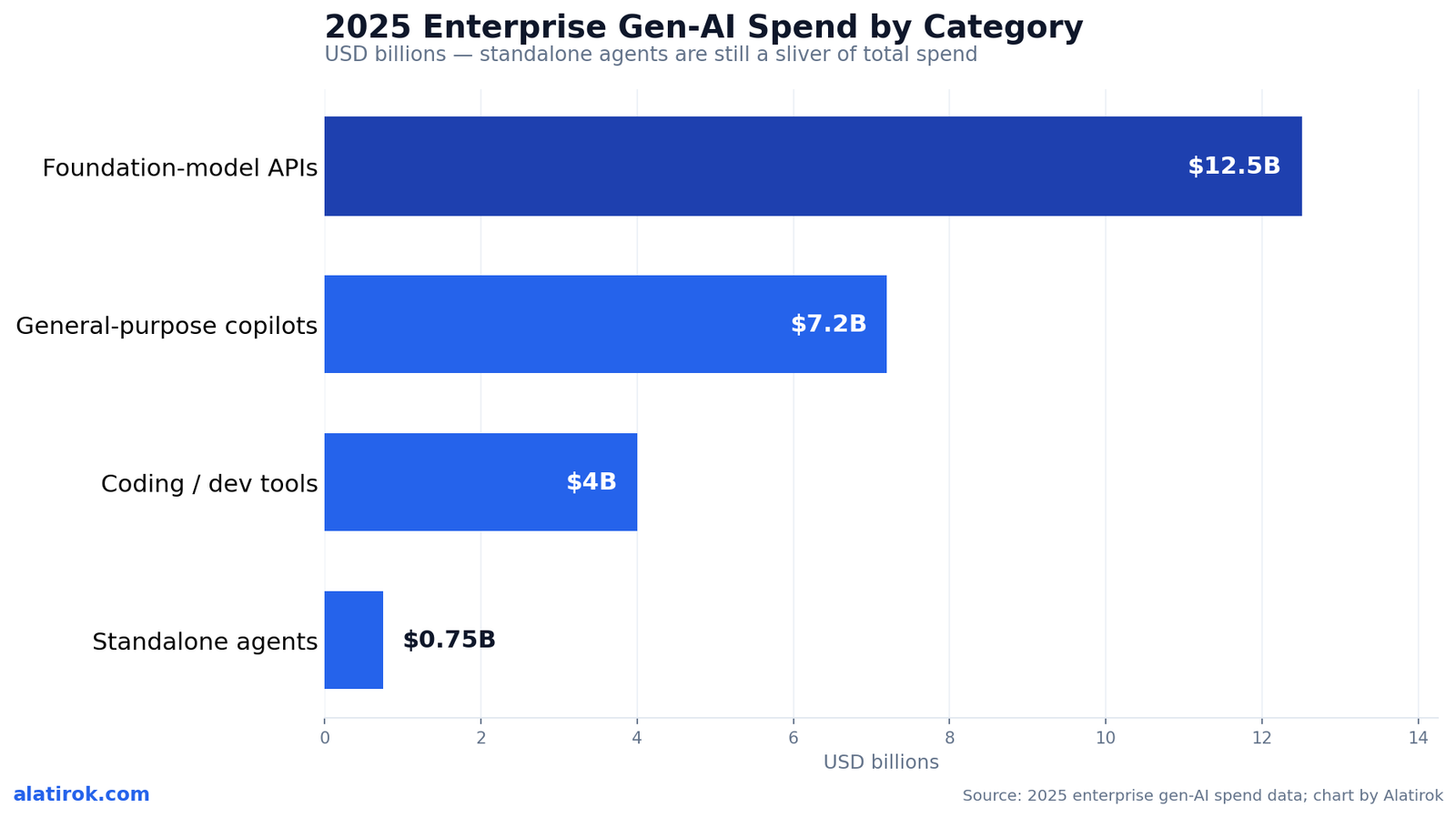

Those numbers look like a finished revolution. The capital flows say otherwise. Menlo Ventures’ 2025 State of Generative AI in the Enterprise — surveying roughly 500 U.S. decision-makers and released December 9, 2025 — found that of $37B in total enterprise generative-AI spend, the line item explicitly labeled ‘agents’ was just $750 million, about 10% of the horizontal applications layer. Most of what gets called an agent is still a copilot or a fixed-sequence workflow.

This is the central tension of AI agent adoption in 2026: near-universal experimentation, broad production presence, and a thin layer of genuinely autonomous systems. Every figure below comes from a named 2025-2026 survey, and the spread between them is the most useful thing in this report.

Production vs. pilot: the deployment gap

The single most important distinction in the 2026 data is what counts as an ‘agent’ and what counts as ‘production.’ Menlo Ventures draws the sharpest line: only 16% of enterprise deployments qualify as true agents — systems where an LLM plans, executes, and adapts — versus 27% among startups. The majority are fixed-sequence or routing workflows that vendors increasingly market as agentic. Gartner calls this ‘agent washing’ and estimates that of the thousands of self-described agentic vendors, only about 130 are real.

McKinsey’s State of AI (the agentic-era edition) reframes adoption around scale rather than presence: 23% of organizations report scaling an agentic system somewhere in the business, and 39% are experimenting — but in any single business function, no more than 10% say they are scaling agents. Deloitte’s State of AI in the Enterprise 2026 lands close: 23% are already using agentic AI to at least a moderate extent, and 74% expect to within two years.

Read together, the surveys describe a funnel. Roughly four in five enterprises have touched agents in some shipped app (a16z). Just under a quarter are scaling them (McKinsey, Deloitte). And only one in six deployments is autonomous enough to deserve the name (Menlo). The deployment gap is not about access to models — it is about the engineering and governance work between a demo and a durable system.

Where the money actually went

$37B

Total 2025 enterprise gen-AI spend

Menlo Ventures; tripled from $11.5B in 2024

$750M

Spend on standalone agents

Menlo Ventures; ~10% of horizontal apps

40%

Anthropic enterprise LLM-API share

Menlo Ventures; OpenAI 27%, Google 21%

81%

Enterprises running 3+ model families

a16z CIO survey; up from 68%

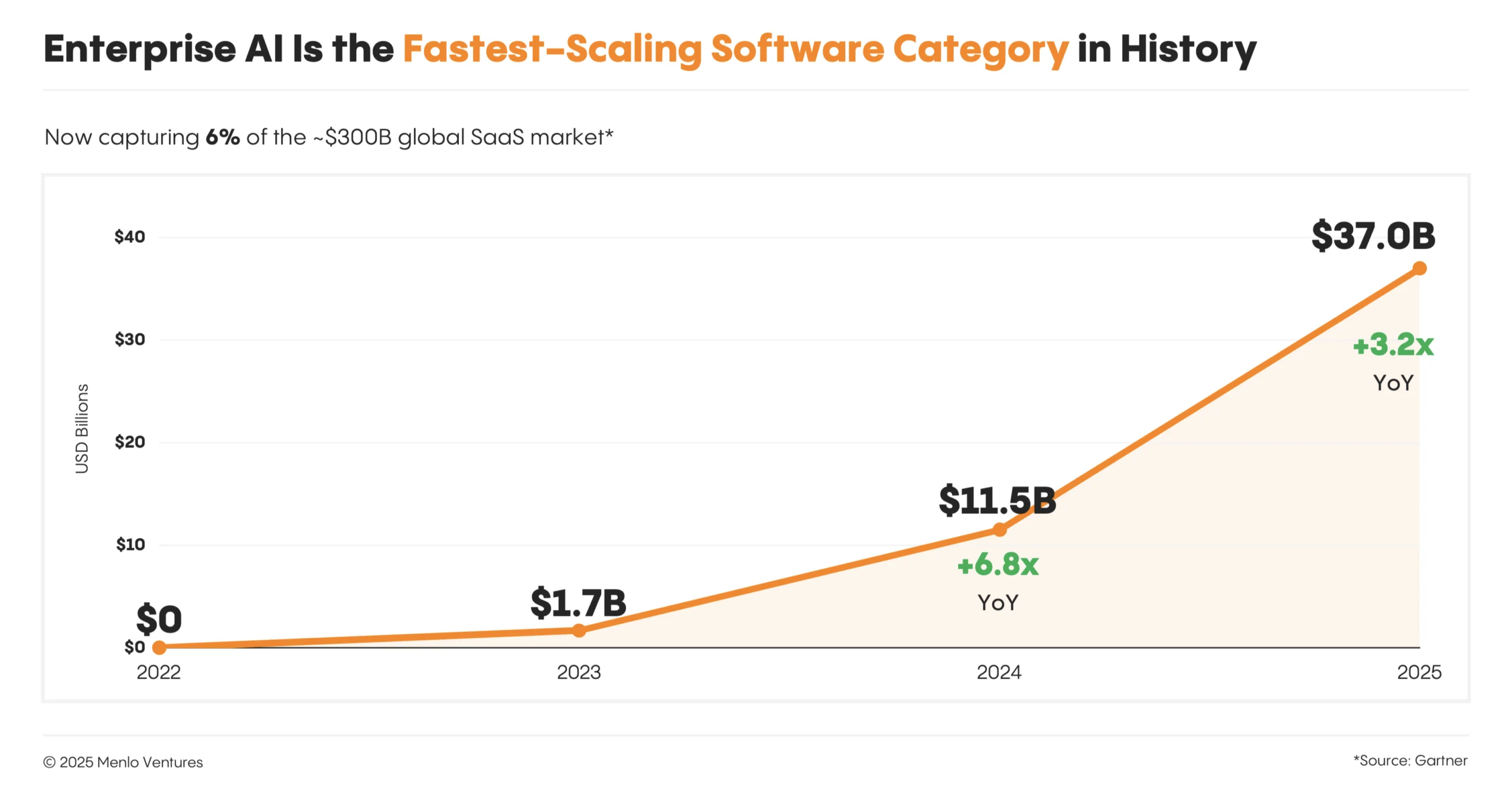

Enterprise AI spend tripled to $37 billion in 2025, the fastest scaling of any software category in history, but agents captured a sliver of it. Menlo Ventures splits the $37B almost evenly: $19B to the applications layer and $18B to infrastructure. Inside applications, coding tools alone took $4.0B, general-purpose copilots took $7.2B, and vertical AI (healthcare leading at $1.5B) took $3.5B. Standalone agents were $750M.

The infrastructure half is dominated by foundation-model APIs at $12.5B, and the vendor ranking inside that pool flipped the conventional wisdom: Menlo reports Anthropic at 40% enterprise LLM-API share, OpenAI at 27%, and Google at 21%. a16z’s CIO panel still shows broad OpenAI usage in production but confirms the multi-model reality — 81% of enterprises now run three or more model families, up from 68% a year earlier, and CIOs expect average LLM spend to climb from about $7M to $11.6M by the end of 2026.

One structural finding cuts across both reports: enterprises buy far more than they build. Menlo found 76% of AI use cases are purchased rather than built internally. That preference is not laziness — as the ROI data shows next, it is the rational response to abandonment rates.

| Category | 2025 spend | Share / note |

|---|---|---|

| Total enterprise gen-AI spend | $37B | Up from $11.5B in 2024 |

| Applications layer | $19B | 51% of total |

| Infrastructure layer | $18B | 49% of total |

| Foundation-model APIs | $12.5B | Largest single line item |

| General-purpose copilots | $7.2B | 86% of horizontal apps |

| Coding / developer tools | $4.0B | Largest departmental category |

| Vertical AI (healthcare $1.5B) | $3.5B | Healthcare = 43% of vertical |

| Standalone agents | $750M | ~10% of horizontal apps |

ROI and the abandonment rate

The defining failure statistic of the era is MIT’s: 95% of enterprise generative-AI pilots delivered no measurable P&L impact. The MIT NANDA ‘State of AI in Business 2025’ study — built from 52 executive interviews, 153 leader surveys, and 300 public deployments — argued the cause is organizational, not technical. MIT named it the ‘learning gap’: companies cannot fold models into their workflows, structures, and culture. Crucially, the report found vendor partnerships succeed about 67% of the time, while internal builds succeed roughly one-third as often — direct empirical support for the buy-over-build pattern.

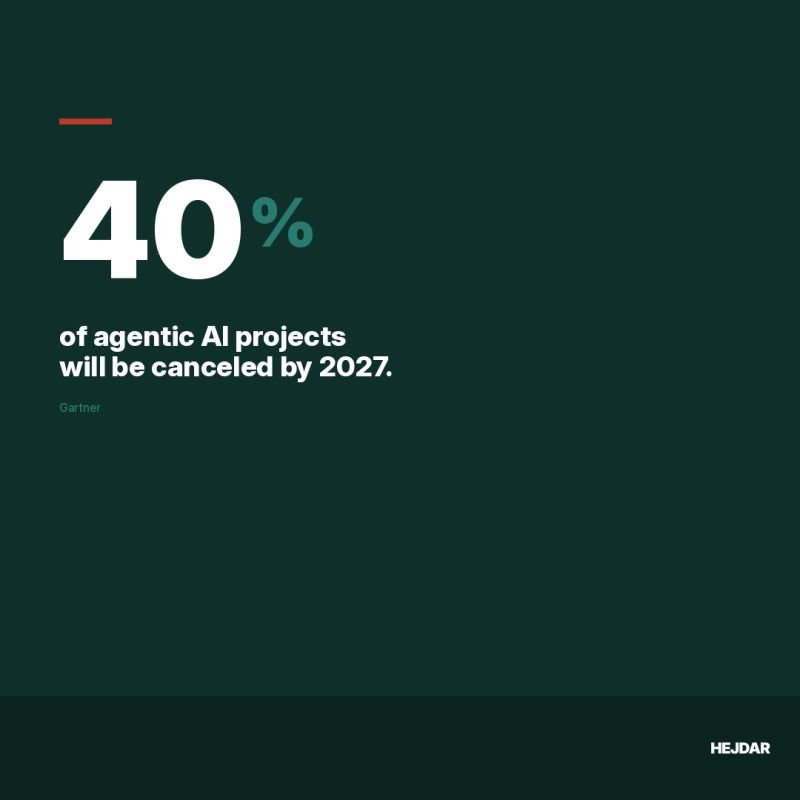

Looking forward, Gartner predicts over 40% of agentic AI projects will be canceled by the end of 2027, citing escalating costs, unclear business value, and inadequate risk controls. That is not a contradiction of the adoption numbers — it is the expected attrition of a hype cycle where, per Gartner, most current projects are early-stage proofs of concept.

The positive ROI signal is real but narrow. MIT found the biggest returns in back-office automation — eliminating outsourcing, cutting agency costs, streamlining operations — even though more than half of gen-AI budgets still flow to sales and marketing. The lesson repeated across reports: payback comes from unglamorous, measurable workflows with a clean success metric, not from open-ended autonomy.

“95% of enterprise generative-AI pilots delivered no measurable impact on the P&L — and vendor partnerships succeeded roughly three times as often as internal builds.”

MIT NANDA, State of AI in Business 2025

Top use cases that pay back

The agent use cases winning in 2026 are concentrated, not scattered: customer service, research and data analysis, internal workflow automation, and software engineering lead every survey. LangChain’s data puts customer service at 26.5% as the most common production use case, with research and data analysis at 24.4% and internal workflow automation at 18%. Inside the largest organizations (10,000+ employees), internal productivity overtakes everything at 26.8%.

McKinsey’s scaled-use data tracks the same pattern by industry: technology leads, with software engineering and IT reporting the highest levels of agents at scale; insurance leads in marketing and sales; healthcare shows strong uptake in knowledge management. The common thread is tasks with abundant text, clear correctness criteria, and a human reviewer in the loop.

This is also where the spend follows function. Coding’s $4.0B (Menlo) is the clearest signal — it is the one category where adoption, daily usage, and willingness to pay all line up, because the output is testable and the productivity gain is immediate. Use cases that disappoint, by contrast, tend to be open-ended ‘do my job’ agents with no objective scoring function.

Pros

Cons

The barriers blocking production

33%

Cite quality as top agent blocker

LangChain; latency second at 20%

~66%

Cite security/risk as top scaling barrier

McKinsey State of AI

89% vs 52%

Observability vs. evals adoption

LangChain; teams watch but cannot grade

21%

Have mature agent governance

Deloitte; vs 74% planning to use agents

Quality, security, and governance — not raw model capability — are the barriers stalling AI agent adoption in 2026. LangChain found quality is the top blocker at 33% (accuracy, consistency, tone, and policy adherence), with latency second at 20%. Among enterprises with 2,000+ employees, security rises to a 24.9% concern. McKinsey is blunter: security and risk are the top barrier to scaling agentic AI, cited by nearly two-thirds of respondents, ahead of regulatory uncertainty or technical limits.

Tooling maturity is uneven in a telling way. LangChain reports 89% of teams have implemented observability, but only 52.4% run offline evals and just 37.3% run online evals. Teams can watch their agents but cannot reliably grade them — which is precisely why quality remains the number-one complaint. Observability tells you something broke; evals tell you whether it works before it ships.

Governance is the widest gap of all. Deloitte found only 21% of companies have a mature governance model for autonomous agents, even as 74% plan to use agents within two years. McKinsey notes only about 30% of organizations reach a meaningful maturity level on agentic controls. The risk surface — tool access, data exposure, autonomous action — is expanding faster than the controls around it.

If your team has observability but no evals, you are in the LangChain majority — and the most likely to see quality complaints in production. Stand up an offline eval suite with a labeled dataset before you widen an agent’s autonomy or tool access, not after.

Scoring the major 2026 surveys

No single survey captures AI agent adoption alone — each measures a different slice, so the honest read triangulates across all of them. Developer surveys (LangChain) over-index on production presence; VC surveys (Menlo, a16z) capture spend and vendor share; consultancies (McKinsey, Deloitte) measure organizational scaling; and the contrarian studies (MIT, Gartner) supply the failure data the optimistic reports gloss over.

Below is how each source ranks as a primary reference for an operator trying to make a deployment decision in 2026 — weighted by sample transparency, recency, and whether the methodology measures real production rather than intent.

Menlo Ventures — State of Generative AI 2025

Best for: Budget benchmarking and vendor selection

What works

Watch out for

LangChain — State of AI Agents 2026

Best for: Engineering and platform teams

What works

Watch out for

McKinsey — State of AI (agentic era)

Best for: Executives planning scale-up

What works

Watch out for

MIT NANDA — State of AI in Business 2025

Best for: Anyone justifying agent budget

What works

Watch out for

What the 2026 data means for operators

The verdict for 2026 is that AI agent adoption is real, profitable in narrow lanes, and dangerously overstated in headlines that conflate presence with autonomy. Four in five enterprises ship something with an agent in it (a16z), but only one in six deployments is genuinely autonomous (Menlo), and 95% of pilots historically returned no measurable P&L (MIT). The winners are not the teams chasing the most ambitious autonomy — they are the teams that bought a proven tool, pointed it at a back-office workflow with a clean metric, and instrumented it with real evals.

The forward indicators are still steep. Gartner projects that 33% of enterprise applications will embed agentic AI by 2028, up from under 1% in 2024, and Deloitte’s 74%-in-two-years intent number suggests the funnel keeps filling. But Gartner’s same forecast — over 40% of agentic projects canceled by end of 2027 — is the reminder that intent is not deployment, and deployment is not ROI.

For anyone allocating budget in 2026, the data converges on one discipline: name the dollar before you staff the agent, buy before you build, and grade before you scale.

Builder’s take

I build Cyntr, an agent orchestration runtime, so I read every one of these surveys the day they drop and then watch what teams actually ship. The gap between the headline adoption numbers and what survives contact with production is the whole story of 2026.

- Trust the production number, not the experimentation number. McKinsey’s 39% experimenting is noise; the 16% of deployments that are true agents (Menlo) is signal.

- Buy before you build. MIT found vendor partnerships succeed ~67% of the time versus internal builds at roughly a third of that — the math is not close.

- Budget for evals, not just observability. LangChain shows 89% have observability but only ~52% run evals; the missing evals are why pilots stall.

- Pick a use case with a clean success metric. Gartner’s cancellations cluster on ‘unclear business value’ — if you cannot name the dollar it saves, do not staff it.

Frequently asked questions

It depends on the definition. LangChain’s 2026 survey found 57.3% of teams have agents in production, and a16z found 80% of enterprises have at least one production app embedding an agent. But Menlo Ventures found only 16% of enterprise deployments are true autonomous agents — the rest are copilots or fixed workflows.

Menlo Ventures put total enterprise generative-AI spend at $37B in 2025, but the line item specifically for standalone agents was just $750M — about 10% of the horizontal applications layer. Copilots ($7.2B) and coding tools ($4.0B) dwarf pure agent spend.

MIT NANDA’s 2025 study found 95% of enterprise generative-AI pilots delivered no measurable P&L impact. Gartner separately predicts over 40% of agentic AI projects will be canceled by the end of 2027, citing escalating costs, unclear value, and weak risk controls.

The data favors buying. MIT found vendor partnerships succeed about 67% of the time while internal builds succeed roughly one-third as often, and Menlo found 76% of enterprise AI use cases are purchased rather than built. Buy a proven tool unless you have a genuine differentiation reason to build.

Quality is the top blocker at 33% and latency is second at 20% (LangChain), while McKinsey found security and risk are the top scaling barrier, cited by nearly two-thirds of respondents. Governance is a major gap: Deloitte found only 21% of companies have mature governance for autonomous agents.

Customer service (26.5% of use cases) and research/data analysis (24.4%) lead by volume, while coding tools attract the most spend ($4.0B). MIT found the highest ROI in back-office automation — cutting outsourcing and agency costs — even though most budgets still go to sales and marketing.

Primary sources

- 2025: The State of Generative AI in the Enterprise — Menlo Ventures

- State of AI Agents 2026 — LangChain

- State of AI trust in 2026: Shifting to the agentic era — McKinsey

- The State of AI in the Enterprise 2026 — Deloitte

- Leaders, gainers and unexpected winners in the Enterprise AI arms race — Andreessen Horowitz

- MIT report: 95% of generative AI pilots at companies are failing — Fortune / MIT NANDA

- Gartner Predicts Over 40% of Agentic AI Projects Will Be Canceled by End of 2027 — Gartner

Last updated: May 31, 2026. Related: Capital.