Hyperscalers depreciate Nvidia GPUs over five to six years. Michael Burry says the real economic life is two to three. The gap, by his math, hides $176 billion in earnings.

What is the GPU depreciation 2026 debate, in one paragraph?

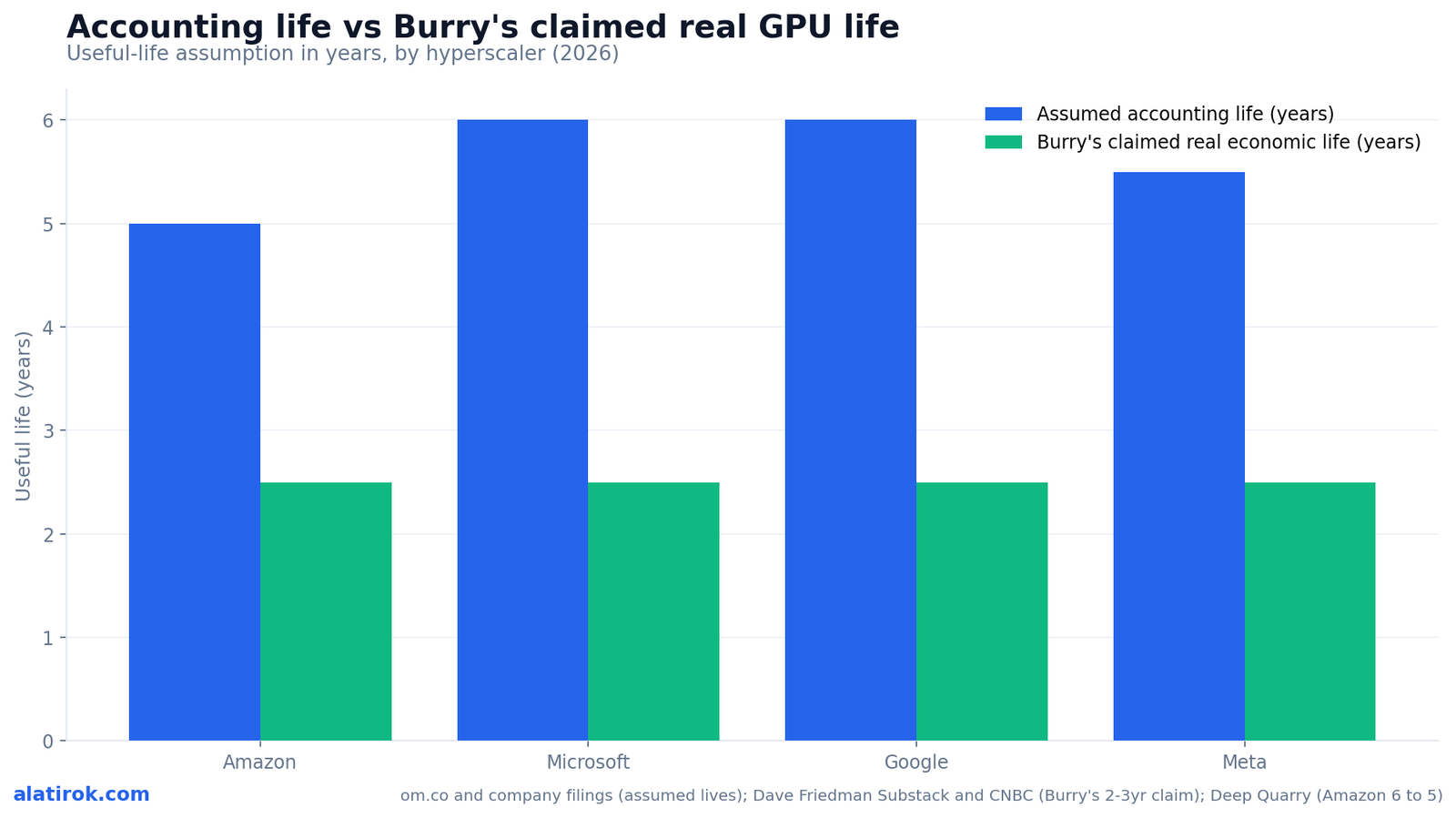

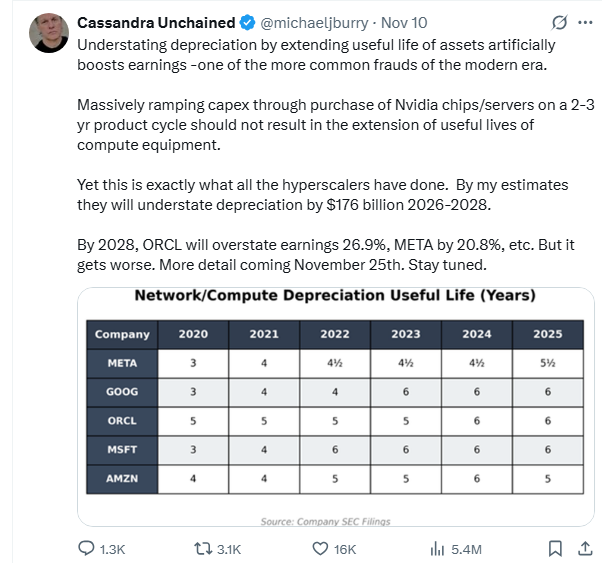

The GPU depreciation 2026 debate is a fight over one accounting estimate: how many years a hyperscaler should spread the cost of an Nvidia GPU across its income statement. Amazon, Microsoft, Alphabet and Meta book their AI servers on a five-to-six-year schedule. Investor Michael Burry argues the real economic life of a flagship GPU is closer to two or three years, because Nvidia now ships a new architecture roughly every year. If he is right, the industry is recording too little depreciation expense, which makes profit look bigger than it is. Burry’s headline number for the gap is about $176 billion of understated depreciation and overstated profit across 2026 through 2028.

Depreciation is not optional spin; it is how accrual accounting spreads a long-lived asset’s cost over the period it earns money. Buy a $30,000 H100 and assume it works for six years, and you charge roughly $5,000 a year against earnings. Assume it works for three years, and you charge roughly $10,000 a year. Same chip, same cash out the door, but the second assumption nearly halves the reported profit the asset generates in any single year. Multiply that across hundreds of billions of dollars of GPUs and the choice of denominator becomes one of the most consequential numbers in the market.

This is not a rounding error hiding in a footnote. It sits at the center of whether the hyperscalers’ record AI margins are real or borrowed from the future. Below we walk through what each company actually books, what Burry’s math implies, what the secondary market for used GPUs says about real economic life, and why the smartest version of the bull case is not ‘Burry is wrong’ but ‘it depends which chip you mean.’

What depreciation schedules do the hyperscalers actually use?

The major hyperscalers normalized on a six-year server life around 2023, and most still use five to six years for the bulk of their data-center hardware in 2026. The shift was deliberate and lucrative. When Alphabet extended its server life to six years for fiscal 2023, it told investors the change would reduce depreciation by roughly $3.4 billion for the year, money that flowed straight to operating income. Microsoft and the others moved in the same direction over the same window, and a six-year assumption became the de facto industry standard for cloud infrastructure.

But 2025 and 2026 introduced a split. Amazon went the other way for its AI fleet. Effective January 1, 2025, it shortened the useful life of a subset of its servers and networking equipment from six years to five. That single change increased depreciation and amortization expense by about $217 million in Q1 2025 alone and cut net income by roughly $162 million; by Q2 2025 the quarterly hit had grown to about $280 million of added D&A. Amazon had also taken roughly $920 million in accelerated depreciation in Q4 2024 as it retired some equipment early, and guided to about a $0.6 billion reduction in 2025 operating income from the move.

Meta, meanwhile, pushed in the opposite direction, extending the useful life of certain servers and network assets to about 5.5 years and booking an estimated $2.9 billion reduction in depreciation expense, equal to nearly 4% of its estimated annual pre-tax profit. So within the same 12 months, one giant shortened its assumption and took a charge while another lengthened its assumption and harvested a gain. That divergence is exactly what makes the depreciation question impossible to wave away as settled accounting.

The mechanics matter because depreciation is a non-cash expense that nonetheless drives reported profit, and the inputs are estimates set by management. Auditors check that the estimate is reasonable, not that it is correct. As Om Malik observed of recent hyperscaler filings, roughly two-thirds of some quarters’ capex now flows into short-lived assets like GPUs that depreciate over three to five years, with the remainder going to long-lived shell-and-power assets depreciating over fifteen years or more. Blend those and you get a headline number that can hide a lot.

| Company | Assumed useful life | Recent change | Stated earnings impact |

|---|---|---|---|

| Alphabet (Google) | ~6 years | Extended to 6 years for FY2023 | ~$3.4B less depreciation in 2023 |

| Amazon (AWS) | ~5 years (AI subset) | Cut 6 to 5 years, eff. Jan 1 2025 | +$217M D&A in Q1 2025; -$162M net income; ~$920M accelerated charge in Q4 2024 |

| Meta | ~5.5 years | Extended useful life in 2025 | ~$2.9B less depreciation (~4% of pre-tax profit) |

| Microsoft | ~5-6 years | Held longer schedule; vertical integration | Two-thirds of recent quarter capex in short-lived assets |

| Burry’s claimed real life | ~2-3 years | n/a (his estimate, not a filing) | Implies ~$50-60B/yr understated depreciation |

How does Burry get to $176 billion in overstated profit?

$176B

Burry’s claimed understated depreciation, 2026-2028

Cumulative across the hyperscalers

~27%

Claimed Oracle profit overstatement by 2028

Burry’s estimate, Nov 2025

~21%

Claimed Meta profit overstatement by 2028

Burry’s estimate, Nov 2025

$1.8B

Annual profit swing on a $10B GPU tranche

3-year vs 6-year schedule

Burry’s $176 billion figure comes from re-depreciating the hyperscalers’ projected GPU capex over a three-year life instead of the five-to-six years they use, then summing the difference for 2026 through 2028. The arithmetic is not exotic. Take a $10 billion tranche of GPUs. On a six-year schedule it generates about $1.67 billion of annual depreciation; on a three-year schedule it generates about $3.33 billion. The roughly $1.8 billion gap between those two numbers is profit that exists under the longer assumption and vanishes under the shorter one. Scale that to the hundreds of billions in AI capex the industry is committing, and the analysis lands at roughly $50-60 billion of understated depreciation per year, or about $176 billion cumulatively across the three-year window.

Burry went further and named names. In November 2025 he posted that Oracle’s profits could be overstated by roughly 27% and Meta’s by roughly 21% by 2028 if their GPU lives were marked to a two-to-three-year reality. He framed the practice bluntly, writing that understating depreciation by extending the useful life of assets ‘artificially boosts earnings’ and calling it ‘one of the more common frauds of the modern era.’ CNBC noted it could not independently confirm the companies were doing anything improper, and that the wide latitude management has in setting depreciation estimates makes the charge hard to prove either way.

The deeper claim underneath the percentages is about cash, not just optics. If a meaningful slice of GPU spending is really sustaining capex, the cost of standing still rather than growth capex that builds new capacity, then what looks like a temporary investment cycle is actually a permanent expense. In that reading, free cash flow is structurally lower than the bull case assumes, and the day of reckoning arrives either as a wave of impairments when stranded chips get written down, or as a quiet investor realization that margins were always going to compress once the depreciation caught up to the spending.

Burry’s central claim is that re-depreciating projected hyperscaler GPU capex over 3 years instead of 5-6 would erase roughly $176 billion of reported profit across 2026-2028 — about $50-60 billion every year. CNBC could not independently verify the practice, and the figure is Burry’s estimate, not a disclosure from any company.

What does the used-GPU market say the real economic life is?

The secondary market suggests GPUs lose value fast but not instantly: an Nvidia H100 holds roughly 75-85% of its acquisition value through 24 months, then slides to around 69% of contemporaneous new pricing by year three. That is steeper than a six-year straight-line assumption implies, but far gentler than the near-worthless-by-year-three picture Burry’s two-to-three-year framing can suggest. New H100s held a $25,000-$40,000 range from mid-2024 into early 2026, with SXM5 80GB units at the top of that band and PCIe parts near the bottom. Peak-scarcity secondary units briefly traded as high as the low $40,000s in mid-2024 before normalizing toward the mid-$20,000s by late 2025.

Age is the dominant variable in the resale data. Units under a year old fetch roughly $18,000-$25,000, one-to-two-year-old units land around $12,000-$18,000, and chips past two years trade at roughly $7,000-$12,000. Warranty status moves the needle too: a unit with 12-plus months of transferable third-party coverage can command 8-12% more than an identical chip with expired support, because Nvidia’s manufacturer warranty does not transfer to secondary buyers. Read together, the curve shows a chip that is clearly depreciating on a roughly three-to-four-year arc as a frontier asset, not a six-year arc, but one that retains real salvage value rather than going to zero.

Two facts complicate the bear case. First, resale price and economic life are not the same thing: a chip can lose half its market value and still earn its keep if the owner keeps it running profitably. Second, demand stayed deep enough that H100s coming off expired contracts have reportedly been rebooked at around 95% of their original rental pricing, and 2020-era A100s remain fully booked for inference. The market is telling us these chips age, but they age into a job, not into a landfill.

Why the bull case says six years is defensible: the value cascade

The strongest counterargument is the ‘value cascade’: a GPU’s job changes as it ages, so it keeps earning long after it stops being the fastest chip in the rack. In this model, a GPU spends years one and two on frontier training where peak performance is everything, moves in years three and four to high-value real-time inference where it is still plenty fast, and settles into years five and six handling cost-sensitive batch inference and analytics where latency barely matters and economics rule. The newest Blackwell parts take over training, displaced H100s slide into premium inference, and aging A100s cascade down to standard inference and ordinary compute. Each step keeps the asset generating revenue, which is the literal test for whether a longer useful life is justified.

theCUBE Research, which coined much of the cascade framing, notes that hyperscalers collectively saved roughly $18 billion in annual depreciation by extending server lives from three-to-four years up to six, and argues the extension was grounded in observed utilization rather than accounting opportunism. The supporting evidence is concrete: A100 chips announced in 2020 remain fully booked for inference, and Azure has run some GPU generations for seven-plus years before retirement. One widely cited analyst flipped from worrying about earnings quality to a more relaxed stance after concluding that a heavily batched A100 can deliver lower total cost of ownership for the right workload than a brand-new, far more expensive B200.

The cascade does not make Burry wrong; it makes the question conditional. If you mean the chip’s life as a frontier training accelerator, two to three years is fair. If you mean its life as a revenue-generating asset across all workloads, five to six years is defensible. The accounting standard asks for the second number, the economic-life-of-the-asset number, which is why auditors have largely signed off. The honest critique is not that the schedules are fraudulent but that blending genuinely short-lived training silicon with genuinely long-lived inference silicon into a single estimate can flatter the average.

Pros

Cons

“The accounting asks one number for the life of the asset. Operators run two clocks: when a newer chip makes this one uneconomic, and how long you can keep it busy at all.”

The core tension in GPU depreciation 2026

What would actually prove Burry right or wrong?

A real distortion, smaller than the bears say and larger than the bulls admit

The decisive evidence will be impairments and schedule changes, not Twitter debates: watch for accelerated-depreciation charges, useful-life cuts, and write-downs of stranded GPUs in the 2026 and 2027 filings. Amazon’s move from six years to five for its AI subset is the canonical tell, because a company only takes a $920 million accelerated charge when its own engineers conclude the old assumption no longer fits the newest workloads. If Microsoft, Alphabet or Oracle follow with similar cuts, Burry’s thesis gains hard corroboration straight from audited disclosures. If instead the schedules hold and utilization data keeps showing old chips fully booked, the cascade view wins on the merits.

A second signal is the capex reclassification question. Hyperscalers frame most GPU spending as growth investment that will taper. If 2026-2027 free cash flow stays compressed even as revenue growth slows, that pattern would suggest a large share of the spend was sustaining capex all along, exactly the structural-margin problem Burry warns about. Conversely, if free cash flow re-expands as the build-out matures, the spending really was a cycle rather than a permanent tax on the business.

For now the verifiable facts cut both ways. The schedules are real and have been audited; the secondary-market depreciation curve is steeper than six-year straight-line but gentler than three-year; one giant is shortening lives while another is lengthening them. That is not the signature of open fraud, but it is also not the all-clear the bulls sometimes claim. The most defensible reading in mid-2026 is that reported AI margins are somewhat overstated relative to a true blended economic life, by an amount real enough to matter and uncertain enough to argue about, which is precisely why this is the AI boom’s most important accounting fight.

Builder’s take

I run Cyntr and Loomfeed on borrowed and owned compute, so depreciation is not an abstraction to me; it is the difference between a margin and a loss. Here is how I read the Burry fight from the operator’s chair:

- The honest answer is that both sides are right about different chips. A frontier training cluster genuinely does fall off a cliff in 24-36 months; a fleet of inference H100s genuinely earns for five-plus years. Lumping them into one ‘useful life’ number is where the accounting gets fuzzy.

- What actually scares me is not the depreciation rate, it is the reclassification it implies. If a chunk of ‘growth capex’ is really sustaining capex, then free cash flow is structurally lower forever, not just this quarter. That is the part the bulls keep dodging.

- When I size compute for Cyntr, I model two clocks: a performance clock (how long until a newer chip makes this one uneconomic for my hottest workload) and a utilization clock (how long I can keep it busy at all). The accountants only book one number. I plan around both.

- Amazon cutting from six years back to five was the tell. You do not take a $920M accelerated-depreciation charge unless your own engineers are telling you the old assumption no longer holds for the AI subset.

- For a small builder the lesson is brutal and simple: rent the frontier, own the trailing edge. Let the hyperscalers absorb the depreciation cliff on the newest silicon while you run last-gen GPUs at 90%+ utilization for batch work.

Frequently asked questions

GPU depreciation is how a company spreads the cost of an expensive AI accelerator across the years it expects the chip to earn money, rather than expensing it all at once. It matters in 2026 because hyperscalers are spending hundreds of billions on Nvidia GPUs, so the assumed useful life directly determines how large their reported AI profits look. A longer assumed life means less annual expense and higher reported earnings; a shorter life means the opposite.

The industry normalized on roughly a six-year server life around 2023. As of 2026, Microsoft and Alphabet sit near five to six years, Meta extended certain servers to about 5.5 years, and Amazon cut a subset of its AI servers from six years to five effective January 1, 2025. Michael Burry argues the real economic life of a flagship GPU is closer to two or three years.

Burry re-depreciated the hyperscalers’ projected GPU capex over a three-year life instead of their five-to-six-year schedules and summed the difference for 2026 through 2028. That works out to roughly $50-60 billion of understated depreciation per year, or about $176 billion cumulatively. He also estimated Oracle’s profits could be overstated by about 27% and Meta’s by about 21% by 2028. CNBC noted it could not independently verify the practice.

Partly. H100s hold roughly 75-85% of their value through 24 months and around 69% of contemporaneous new pricing by year three, with two-year-old units fetching about $7,000-$12,000 versus $25,000-$40,000 new. That curve is steeper than a six-year straight line but far from worthless by year three, which is why the resale data supports neither extreme cleanly.

The value cascade is the idea that a GPU changes jobs as it ages: frontier training in years one to two, high-value real-time inference in years three to four, and cost-sensitive batch inference in years five to six. Because the chip keeps generating revenue at each step, owners argue a five-to-six-year economic life is justified even though the chip is no longer the fastest available. A100s from 2020 remaining fully booked for inference is the headline evidence.

Watch the 2026 and 2027 filings for accelerated-depreciation charges, useful-life cuts, and write-downs of stranded GPUs. Amazon’s six-to-five cut and ~$920 million accelerated charge already lean Burry’s way; if Microsoft, Alphabet or Oracle follow, his thesis gains audited support. If schedules hold and old chips stay fully utilized, the value-cascade view wins instead.

Primary sources

- Big Short investor Michael Burry accuses AI hyperscalers of artificially boosting earnings — CNBC

- The $176 Billion Accounting Question at the Heart of the AI Boom — Dave Friedman (Substack)

- Deep Quarry: Useful Lives of GPUs and Key Considerations — National Law Review

- Mike Burry says Oracle will overstate earnings by 27% and Meta by 21% — Cryptopolitan

- Amazon revises server lifespan amid AI shift, impacting 2025 earnings — Deep Quarry (Substack)

- 298 | Resetting GPU Depreciation — Why AI Factories Bend But Don’t Break Useful Life Assumptions — theCUBE Research

- Used GPU Market: A100 & H100 Pricing, Depreciation — Hashrate Index

- What I Learned about Hyperscalers’ AI Spend — Om Malik

- Why I don’t worry (as much) about big tech’s depreciation schedule — MBI Deep Dives

Last updated: June 1, 2026. Related: Capital.