AI-native startups have collapsed the zero-to-$100M ARR timeline from years to months. Here is the data on who is fastest, and why the old SaaS records no longer hold.

What is the fastest company to $100M ARR?

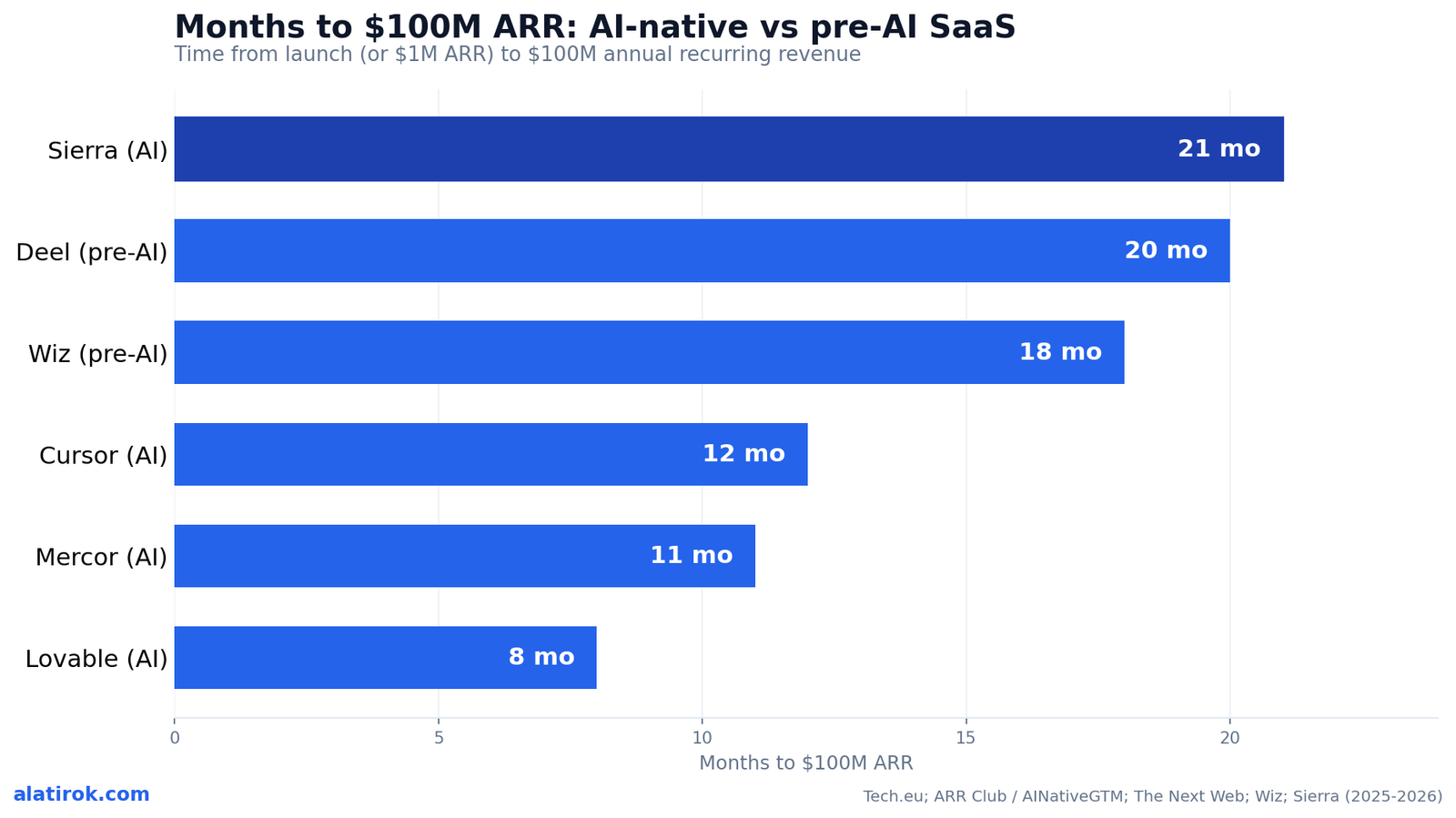

Lovable, a Swedish AI app-builder, is the fastest software company ever to reach $100M ARR, hitting the milestone in just 8 months and claiming the record ahead of OpenAI, Cursor, and Wiz. It crossed the line in July 2025 with roughly 2.3 million active users and only 45 full-time employees, then raised a $200M Series A from Accel at a $1.8B valuation, per Tech.eu and TechCrunch. This is the fastest to $100M ARR leaderboard, and AI-native startups now own the top of it.

That number would have been a rounding error of disbelief just three years earlier. For most of SaaS history, $100M ARR was a milestone you celebrated after the better part of a decade. Now a 45-person company reaches it before its first anniversary. This article puts the new records side by side with the old ones, and asks the more interesting question underneath the headlines: what actually changed to make this possible, and which of these run rates will still be standing in 2028.

The shorthand for this phenomenon is ARR velocity, the rate at which a company converts founding to recurring revenue. By that measure, a handful of AI-native companies have not just beaten the old records. They have made them look like they belong to a different sport.

The fastest to $100M ARR, ranked by months

Ranked by months from launch to $100M ARR, the fastest companies are Lovable (8 months), Mercor (11), and Cursor (about 12) — all of which beat the pre-AI records held by Wiz (18) and Deel (20). The cluster at the top of the table is almost entirely AI-native, and the gap between the new leaders and the old benchmark is not marginal: Lovable reached the milestone in under half the time it took Wiz, the company that held the crown just three years earlier. On the fastest to $100M ARR race, the gap between AI-native and classic SaaS is measured in years, not months.

Mercor, an AI-driven labor marketplace founded by three college dropouts, scaled from $1M to $100M ARR in 11 months while averaging 41% month-over-month growth through 2024 and posting 55% in January 2025 and roughly 88% in February, according to ARR Club and AINativeGTM. Cursor’s maker Anysphere hit $100M ARR around the 12-month mark. Sierra, Bret Taylor’s enterprise customer-agent company, took seven quarters — about 21 months — which by any pre-2024 standard would itself have been a world record, yet now sits near the bottom of this particular list.

The pre-AI reference points matter for calibration. Wiz’s 18 months and Deel’s 20 months were genuine outliers when they happened, celebrated as the fastest ever. The median SaaS company, by contrast, took five to ten years to reach $100M ARR, with Kimchi Hill’s analysis of 140 top SaaS businesses showing the bulk landing in that window. So the AI-native leaders are not beating the average by a few quarters. They are beating the previous record-holders by months, and beating the median by years.

Some figures are measured from company founding (Lovable, Sierra) and others from $1M ARR (Mercor, Wiz, Deel). The starting line is not perfectly standardized across sources, so treat sub-month differences as noise and the years-to-months collapse as the real signal.

Why AI-native startups got so much faster

8 months

Lovable to $100M ARR

Fastest software company ever; 45 employees, 2.3M users

88%

Mercor’s peak monthly growth

February 2025, per ARR Club

5-10 yrs

Median pre-AI SaaS to $100M

Kimchi Hill analysis of 140 top SaaS firms

AI-native startups reached $100M ARR faster because they fused viral self-serve distribution, usage-based pricing, and tiny high-leverage teams — collapsing the cost and time of acquiring and expanding revenue. Lovable’s 45 employees serving 2.3 million users is the clearest illustration: the product is the salesforce, the onboarding, and the expansion motion all at once.

Three structural shifts compound here. First, distribution went peer-to-peer. Vibe-coding and AI tools spread through social feeds and word of mouth, so customer acquisition cost approaches zero for the early millions of users — a luxury Wiz never had with its enterprise security sale. Second, pricing went consumption-based. When a customer’s bill scales with tokens consumed or tasks completed, revenue expands automatically with usage rather than waiting for an annual renewal negotiation. Third, the underlying capability arrived pre-built. Founders did not spend two years training models; they wrapped frontier APIs and shipped, turning what used to be R&D time into go-to-market time.

The result is a different revenue physics. In the old SaaS model, you hired ahead of revenue: sales reps, solutions engineers, customer success. In the AI-native model, the marginal cost of the next thousand customers is mostly inference, and the product onboards them itself. That is why a company can post $100M ARR with a team smaller than a single enterprise sales region.

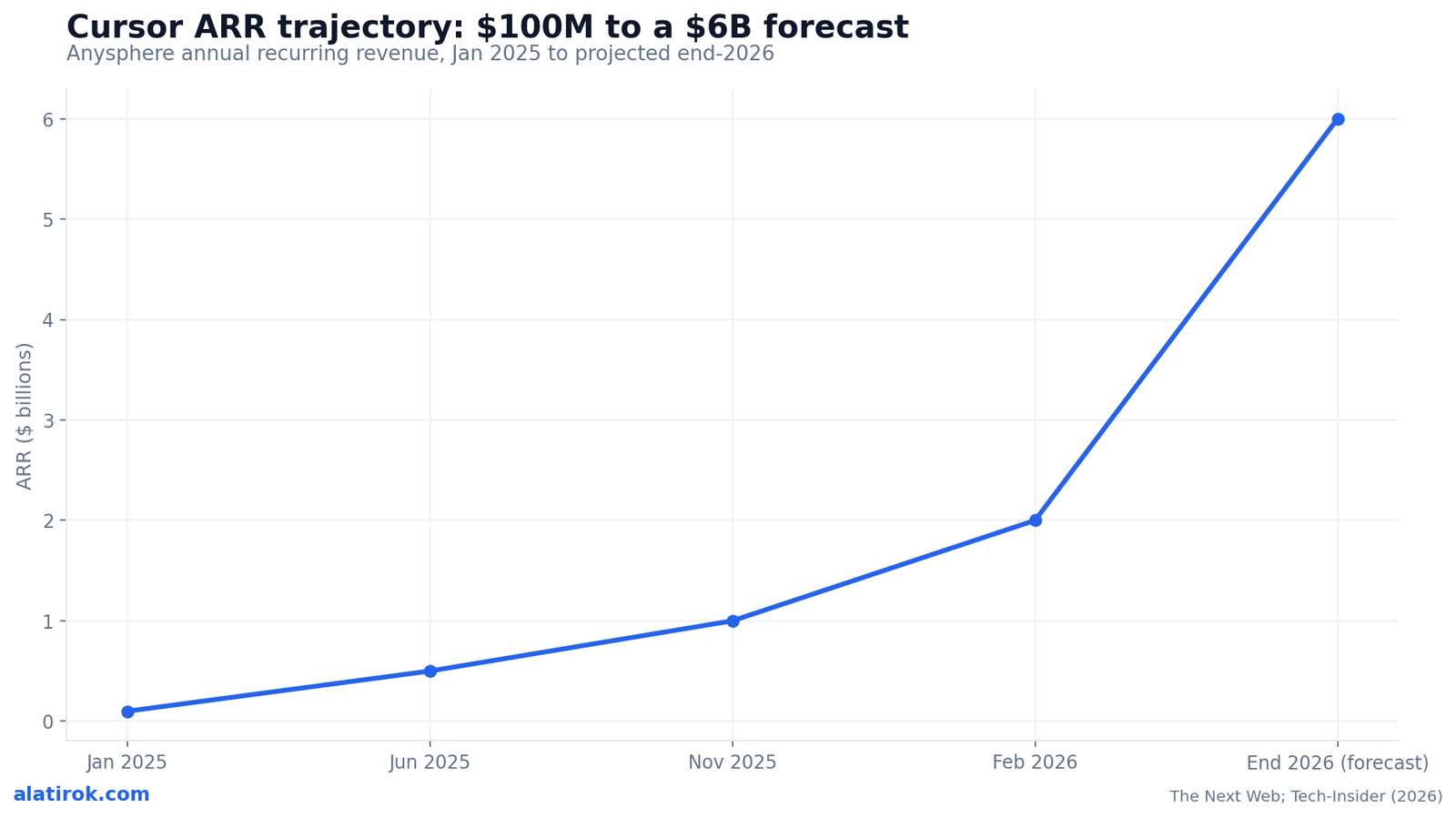

Cursor’s trajectory shows velocity compounds past $100M

Cursor proves that AI revenue velocity does not stop at $100M ARR: Anysphere hit $100M in January 2025, $500M by June, $1B by November, and $2B by February 2026 — the fastest B2B software company from zero to $2B on record. The company is now forecasting more than $6B ARR by the end of 2026, per The Next Web, and is reportedly raising around $2B at a roughly $50B valuation.

The shape of this curve is the point. Traditional SaaS growth decelerates as the law of large numbers kicks in — doubling $50M is hard, doubling $1B is brutal. Cursor doubled from $1B to $2B in about three months. That trajectory, if the $6B forecast holds, implies the company roughly triples again in the ten months after February 2026. Anysphere reportedly serves over a million paying customers and counts roughly 70% of the Fortune 1,000, which means the expansion is coming from both new logos and seat-and-usage growth inside accounts that already pay.

Cursor’s run is the strongest evidence that this is not purely a consumer-virality story. Lovable’s speed could be dismissed as a low-ACV land grab, but Cursor is selling into the enterprise and still compounding faster than Slack, Zoom, or Snowflake ever did on the way to their first billion. The same forces — usage-based billing, bottoms-up adoption, near-zero marginal distribution cost — appear to work at $2B just as they did at $20M.

“Cursor doubled from $1B to $2B ARR in about three months. Traditional SaaS spends years on that step.”

Based on The Next Web reporting, February 2026

The fastest to $100M ARR: full comparison table

Across the cohort, AI-native companies reached $100M ARR in 8 to 21 months, while the pre-AI record-holders needed 18 to 20 — and the median SaaS company needed five to ten years. The table below lays out each company’s milestone alongside the business model that powered it, because the timeline only makes sense in light of how the revenue was actually generated.

Replit is the clearest example of velocity continuing after the milestone: it went from $10M to $100M ARR in about six months, then raised a $400M Series D at a $9B valuation in March 2026 — tripling its valuation in six months, per TechCrunch — and is targeting $1B run-rate revenue by year-end. Sierra, meanwhile, hit $100M ARR in seven quarters and crossed $150M in January 2026 on the back of outcome-based contracts where customers pay per resolved conversation, then raised roughly $950M at a $15B valuation in May 2026.

| Company | Time to $100M ARR | Model | Latest valuation |

|---|---|---|---|

| Lovable | 8 months | Self-serve AI app builder | $1.8B (Series A) |

| Mercor | 11 months | AI labor marketplace | $10B (Series C) |

| Cursor (Anysphere) | ~12 months | AI coding, bottoms-up B2B | ~$50B (reported) |

| Sierra | ~21 months (7 quarters) | Enterprise AI agents, outcome-based | $15B (May 2026) |

| Wiz (pre-AI) | 18 months | Cloud security, enterprise sales | Acquired (Google) |

| Deel (pre-AI) | 20 months | Global payroll/HR | Private |

| Median SaaS (pre-AI) | 5-10 years | Conventional B2B sales + PLG | Varies |

Why the new $100M ARR records deserve an asterisk

The headline records are real, but ARR velocity measures how fast money came in, not how durably it stays — and AI-native revenue is uniquely exposed to churn, model commoditization, and usage that evaporates as fast as it spiked. A run rate is an instantaneous snapshot annualized; it says nothing about net revenue retention, gross margin after inference costs, or whether the customer renews when the novelty fades.

Three risks sit under these numbers. Usage-based revenue is reflexive: it inflates during a hype cycle and can deflate just as quickly when a customer’s experiment ends or budgets tighten. Model commoditization is constant: a cheaper or better frontier model can erode a wrapper’s pricing power overnight, and much of this revenue is built on third-party APIs. And consumer-led virality has a retention tax — acquiring 2.3 million users cheaply means little if a meaningful share lapse within a year. None of this makes the records fake. It means a 8-month sprint to $100M ARR and a durable $100M business are not yet the same thing, and only time-on-the-clock will tell them apart.

There is also a measurement caveat. Some figures count from founding and others from $1M ARR; some are audited and others are founder tweets. The years-to-months collapse is unambiguous in the aggregate, but the exact ranking within a few months should be read with appropriate skepticism.

Pros

Cons

$100M ARR means a company earned roughly $8.3M in its best recent month, annualized. It is not $100M booked or collected. Always pair an ARR headline with net revenue retention before treating it as a durable business.

What ARR velocity means for founders and investors

The records are real; the durability is still being priced

For founders and investors, the lesson is that distribution and pricing model now determine velocity more than headcount or capital — but durability still has to be earned the old-fashioned way. The AI-native playbook (self-serve onboarding, usage-based pricing, frontier APIs, viral distribution) has demonstrably compressed time-to-$100M from years to months. That is a tailwind any builder should try to ride.

But the cohort splits into two stories. Lovable and Replit show how fast bottoms-up, consumer-adjacent products can scale. Sierra and Cursor show that the same velocity can reach the enterprise when paired with outcome-based or seat-and-usage contracts that expand inside accounts. The investors writing $50B and $15B checks are betting that velocity at this scale predicts durability. The skeptics are betting that some of these run rates are the high-water mark of a hype cycle. Both will be proven partly right, and the dividing line will be retention.

The honest takeaway for anyone building in 2026: treat these records as evidence of what is now possible, not as a target to anchor on. They represent the extreme tail of an AI gold rush. The companies that still matter in 2028 will be the ones whose revenue survived the next model release — and that is a different, slower, harder game than the sprint to the first $100M.

Builder’s take

I build revenue-generating software for a living, so when I see an 8-month sprint to $100M ARR I do not read it as a victory lap. I read it as a warning about how compressed the whole game has become. As the founder of Cyntr and Loomfeed, here is what these numbers actually mean from the builder’s seat:

- The denominator changed, not just the numerator. Wiz needed an enterprise sales motion to hit $100M ARR in 18 months. Lovable did it in 8 with 45 people and a self-serve credit card flow. The new records are as much about distribution physics as product quality.

- ARR velocity and ARR durability are different sports. A net-revenue-retention number you can trust matters more than a press-release run rate. Usage-based AI revenue can deflate as fast as it inflated when a cheaper model ships or a customer’s experiment ends.

- Speed-to-$100M is now a recruiting and fundraising weapon more than a moat. The moat still gets built the boring way: retention, switching costs, and a wedge competitors can’t copy in a weekend. I would rather have Sierra’s outcome-based contracts than a viral spike.

- If you are pre-seed in 2026, do not anchor on these numbers. They are the top 0.01% of an AI gold rush, not a target. Optimize for a real wedge and revenue that survives the next model release, and let velocity be a side effect.

Frequently asked questions

Lovable, a Swedish AI app-building platform, is the fastest software company ever to reach $100M ARR, hitting the milestone in just 8 months in July 2025. It surpassed previous record-holders including OpenAI, Cursor, and Wiz, doing so with roughly 2.3 million active users and only 45 full-time employees.

Before the AI wave, the fastest software companies took around 18 to 20 months — Wiz reached $100M ARR in 18 months and Deel in 20, both celebrated as record-breaking at the time. The median SaaS company took far longer, typically five to ten years from founding to $100M ARR.

Cursor’s maker Anysphere hit $100M ARR around January 2025, $500M by June 2025, $1B by November 2025, and $2B by February 2026 — described as the fastest B2B software company from zero to $2B on record. The company is forecasting more than $6B ARR by the end of 2026.

Three forces compound: viral self-serve distribution that drives customer acquisition cost toward zero, usage-based pricing that expands revenue automatically with consumption, and frontier model APIs that let founders ship products without spending years on R&D. Together they let tiny teams scale revenue with very little headcount.

ARR (annual recurring revenue) is a snapshot of recurring revenue annualized from a recent period. ARR velocity is the speed at which a company grows that figure — for example, months from founding to $100M ARR. Velocity measures how fast money arrives but says nothing about whether it stays, which is why net revenue retention matters alongside it.

The years-to-months collapse is well documented, but exact rankings deserve caution. Some figures are measured from company founding and others from $1M ARR, and some are audited while others are self-reported by founders. The records are real signals of AI-native demand, but a fast run rate does not guarantee a durable business until retention is proven.

Primary sources

- Lovable becomes fastest software company ever to reach $100M ARR — Tech.eu

- Eight months in, Swedish unicorn Lovable crosses the $100M ARR milestone — TechCrunch

- Mercor AI ARR hit $100M, from $1M to $100M in just 11 months — ARR Club

- From Zero to $100M ARR in 11 Months: The Mercor Story — AINativeGTM

- Cursor in talks to raise $2B at $50B valuation after hitting $2B ARR in three years — The Next Web

- Cursor AI Valuation Hits $60B: Anysphere’s $2B Revenue Surge — Tech-Insider

- $100M ARR in 18 months: Wiz becomes the fastest-growing software company ever — Wiz

- Cloud security startup Wiz reaches $100M ARR in 18 months — TechCrunch

- Sierra hits $100M ARR milestone in 7 quarters — Sierra

- Sierra raises $950M as the race to own enterprise AI gets serious — TechCrunch

- Replit snags $9B valuation 6 months after hitting $3B — TechCrunch

- Path to $100m of Top 140 SaaS Unicorn Businesses — Kimchi Hill

- OpenAI ads pilot tops $100 million in annualized revenue in under 2 months — CNBC

Last updated: June 1, 2026. Related: Capital.